- Crypto Pragmatist by M6 Labs

- Posts

- Brutal Flush, Flickers of Life Return

Brutal Flush, Flickers of Life Return

BTC Rejects Sub-80K, ETF Flows Turn Green, Liquidity Still Thin

The Coiners

November 22, 2025

GM Anon!

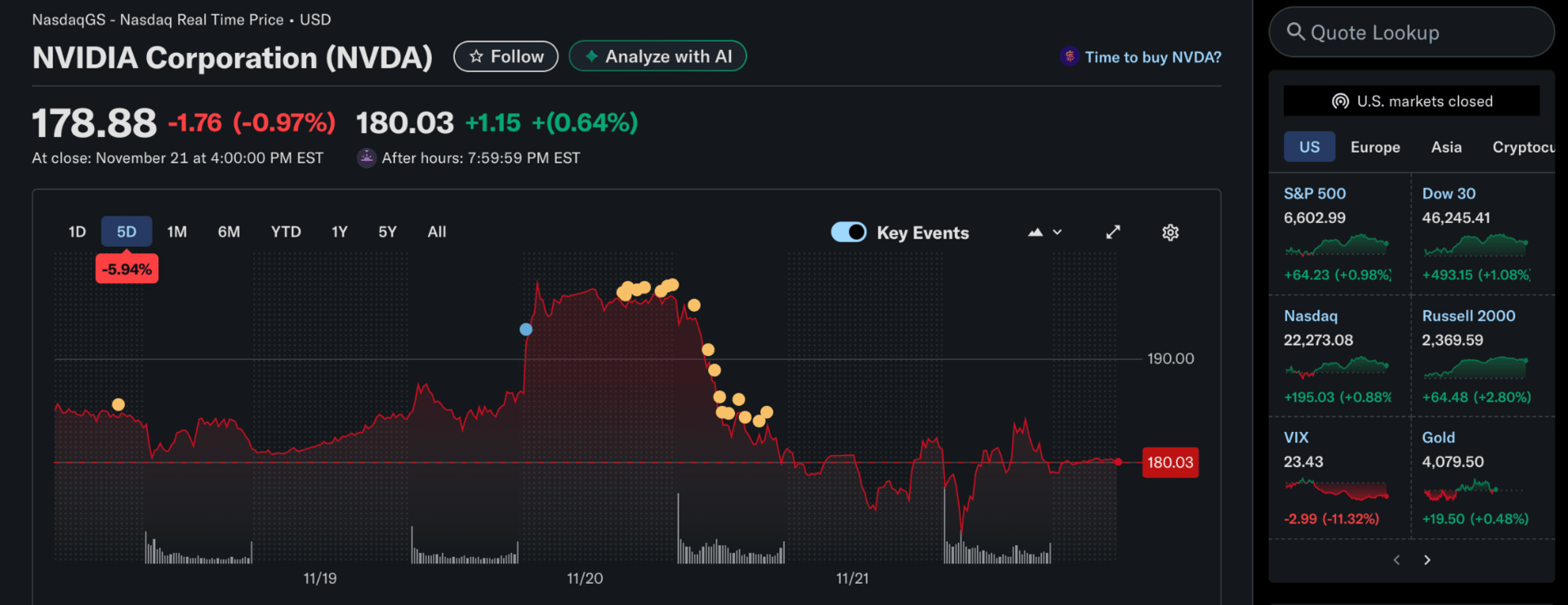

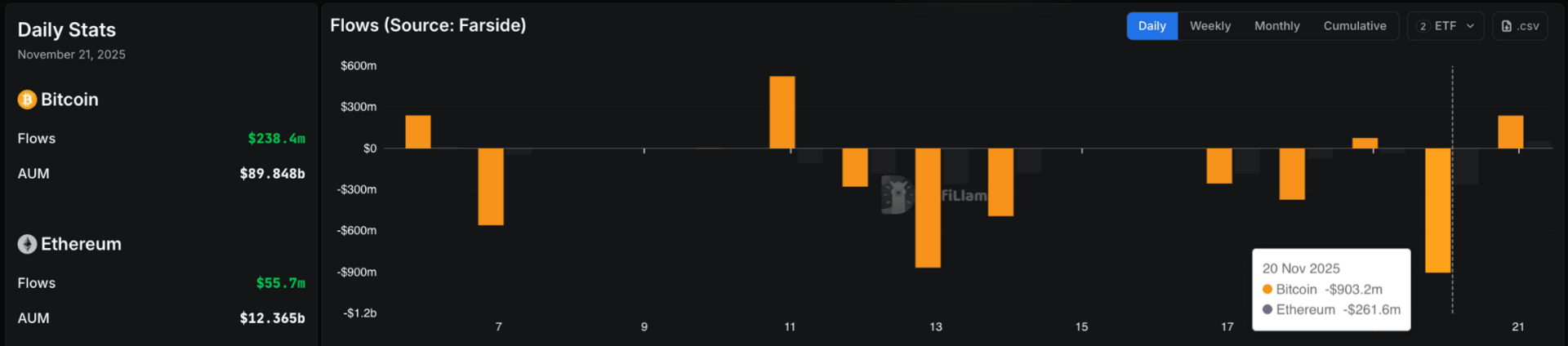

BTC briefly dipped into the high-70s before snapping back above $85K, helped by the first meaningful green ETF print since November 11 — roughly $238M in inflows. ETH even managed a positive flow. Nvidia essentially saved the market from a deeper unwind, beating expectations and stabilizing equities at a critical moment.

The crypto washout was positioning-driven rather than macro-driven, with no real shift in fundamentals behind the collapse. Liquidity is still tight and high-beta names remain heavy, but the tape looks less chaotic than it did just a few days ago. It isn’t strength yet, but the selling pressure finally shows signs of fatigue.

Let’s break down what unfolded this week.

TLDR

Macro stayed volatile as strong jobs data and Fed hesitation clashed with markets suddenly repricing cuts.

Nvidia’s rally faded, equities softened, and thin liquidity kept risk assets jumpy.

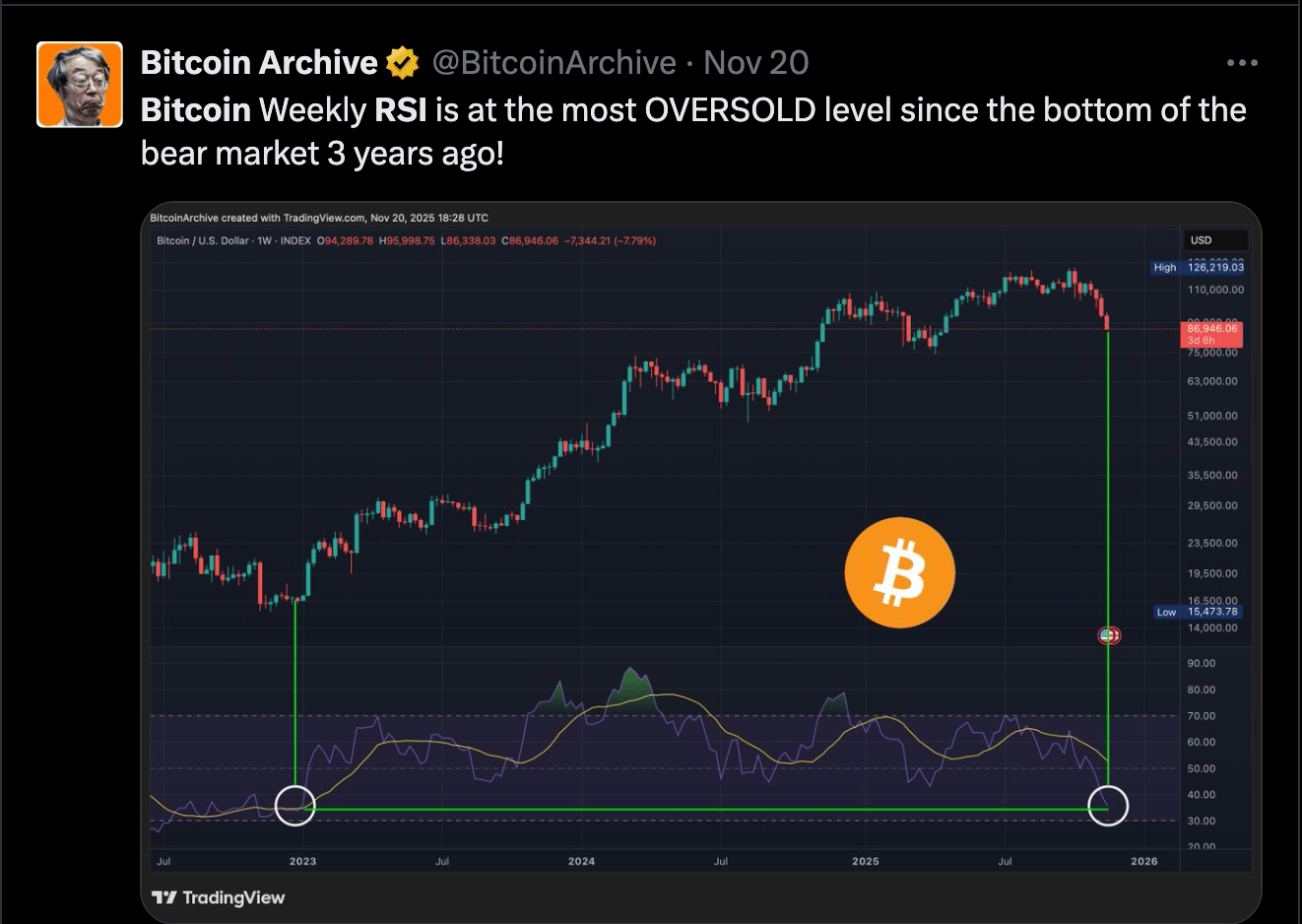

BTC dipped below $80K, triggering the second-largest ETF outflow and a three-year RSI low.Forced flows hit hard: $1.4B BTC sold by Gunden, 10K ETH from FG Nexus, and nearly $1B moved by Mt Gox.

Sentiment steadied as ETF flows turned positive, whales bought, and desks framed the sell-off as positioning.

Institutions stayed active with the SOL and XRP ETFs, Coinbase expansions, and new RWA moves across Plume, NH, and Saudi real estate.

Infra build continued: Kraken’s $800M raise + IPO filing, Aztec Ignition, OpenLedger AI, and Vitalik’s privacy/quantum updates.

Regulators stayed noisy: US bills advanced, Korea pushed a 20–25% tax, Brazil eyed cross-border crypto taxes, and OCC cleared banks for gas-fee crypto.

Cultural assets felt stress (Punks near 90K) while pockets like HYPE, ASTER, and TNSR bounced on momentum and fee spikes.

Positioning remains cautious, stablecoin supply slipped, but forced sellers look done — the market ends the week far more stable than it began (hopefully).

Join The Coiners + Get in on the $50K Grid Bot Challenge 🚀

Don’t wait, Anon — it’s free and will level up your trading game. As a member, you’ll unlock:

High-calibre crypto trading alerts

Weekly live streams with expert trader Michael Whitman (Wed Q&A + Fri Market Recap)

Real-time strategies straight from the pros

🔥 Plus, get front-row access to our $50K Grid Bot Challenge — we’re putting $50K into Pionex Grid Bots and you can follow along every step:

✅ Learn the exact ranges + settings we use

✅ Copy the bots into your own account with 1 click

✅ Track live results in real time

✅ Vote on the “Coin of the Week” for a short-term bot

The mission: turn $50K into 6 figures while showing you how to run profitable bots yourself.

Want more? Qualify for VIP access by meeting one of these:

Deposit $100K+ through a partner exchange

Trade $1M+ in monthly volume

Refer 3 friends who sign up

Stay sharp, stay active, and keep stacking edge with The Coiners.

Market Update

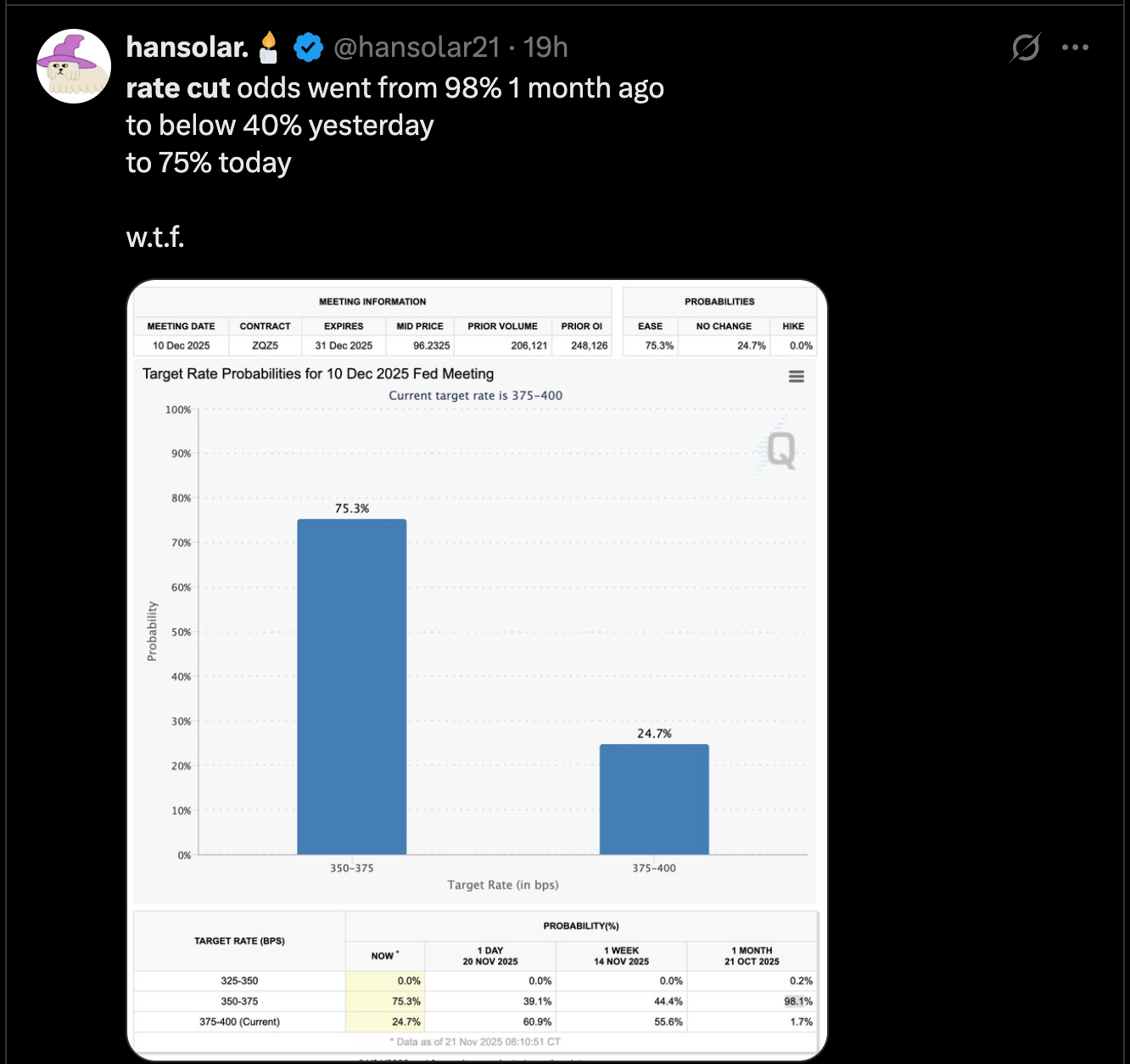

Macro conditions remained chaotic this week as markets absorbed stronger US jobs data, mixed signals from the Fed, and the unwinding of Nvidia’s earnings bounce. Early expectations for a December cut faded after payrolls beat forecasts and Vice Chair Barr reiterated lingering inflation concerns, yet prediction markets abruptly swung toward pricing in more aggressive easing.

Equities lost momentum as Nvidia’s gains reversed, gold softened, and liquidity remained tight enough to keep high-beta assets under pressure. The tone was less about macro deterioration and more about uncertainty and thin positioning — the kind of environment where volatility is amplified and forced flows dominate price action.

Crypto felt that stress directly. The drop that dragged BTC just below 80K triggered the second-largest ETF outflow on record, pushed RSI to a three-year low, and coincided with a wave of mechanical selling: Gunden exited a $1.4B position after 14 years, FG Nexus sold 10K ETH, Mt Gox moved nearly $1B BTC to an unmarked address, and institutional desks grappled with $1B in ETH DAT orders from Asia being shelved.

Noise increased as Tom Lee argued that parts of the sell-off were exacerbated by a software glitch, while Bitmine’s $3.5B unrealised loss added to sentiment drag. Yet the market stabilized meaningfully into the weekend. ETF flows flipped back to green, whales resumed accumulation, and StanChart and Bernstein framed the 25% slide as a positioning flush rather than a regime shift.

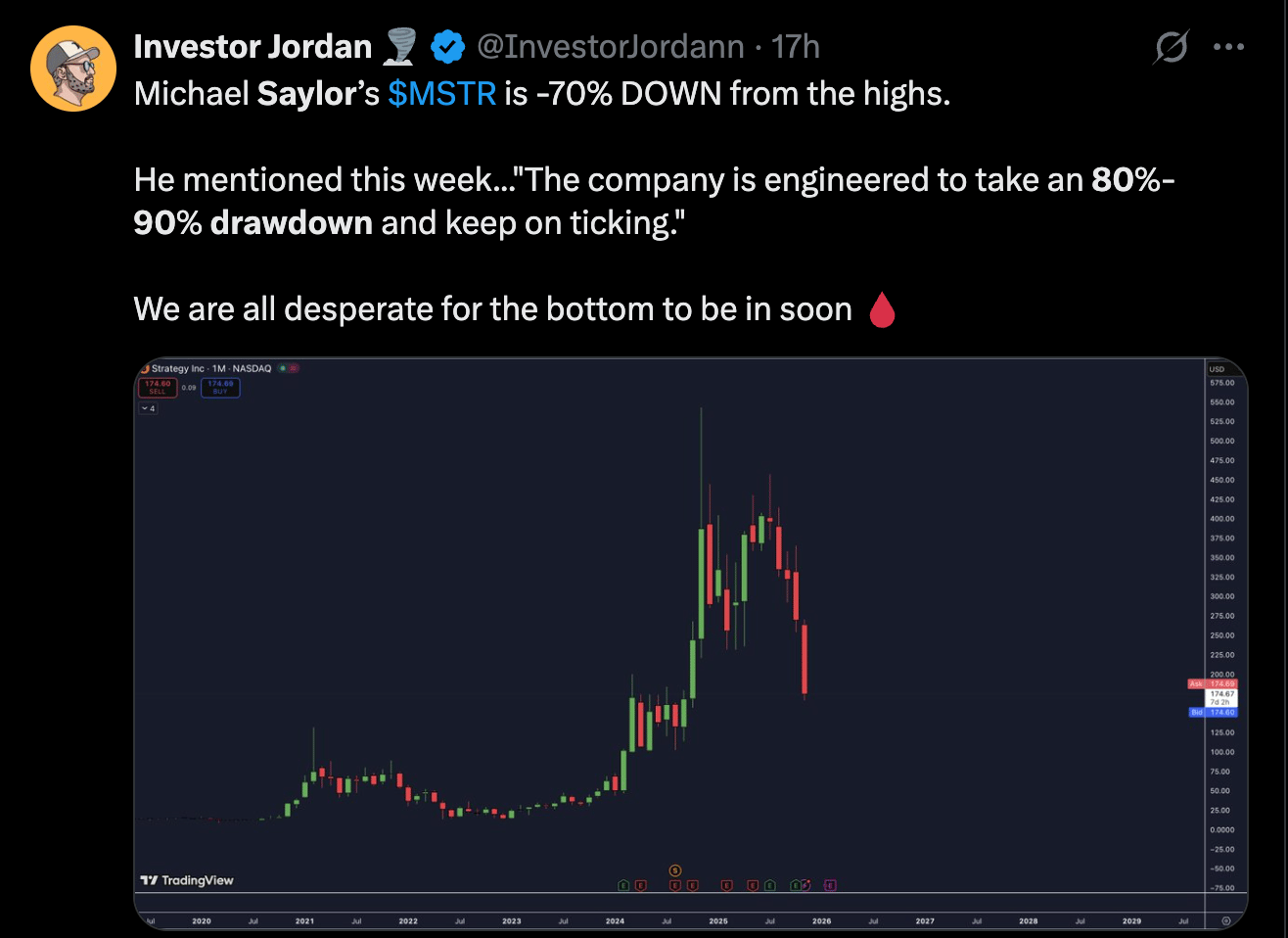

Strategy added $836M BTC despite the turbulence, Saylor reiterated that the firm could withstand an 80–90% drawdown, and El Salvador and Metaplanet disclosed a combined ~$195M of BTC buys. ETH saw modest inflows and fresh attention through new privacy work from Vitalik, alongside his call for quantum-resilience planning.

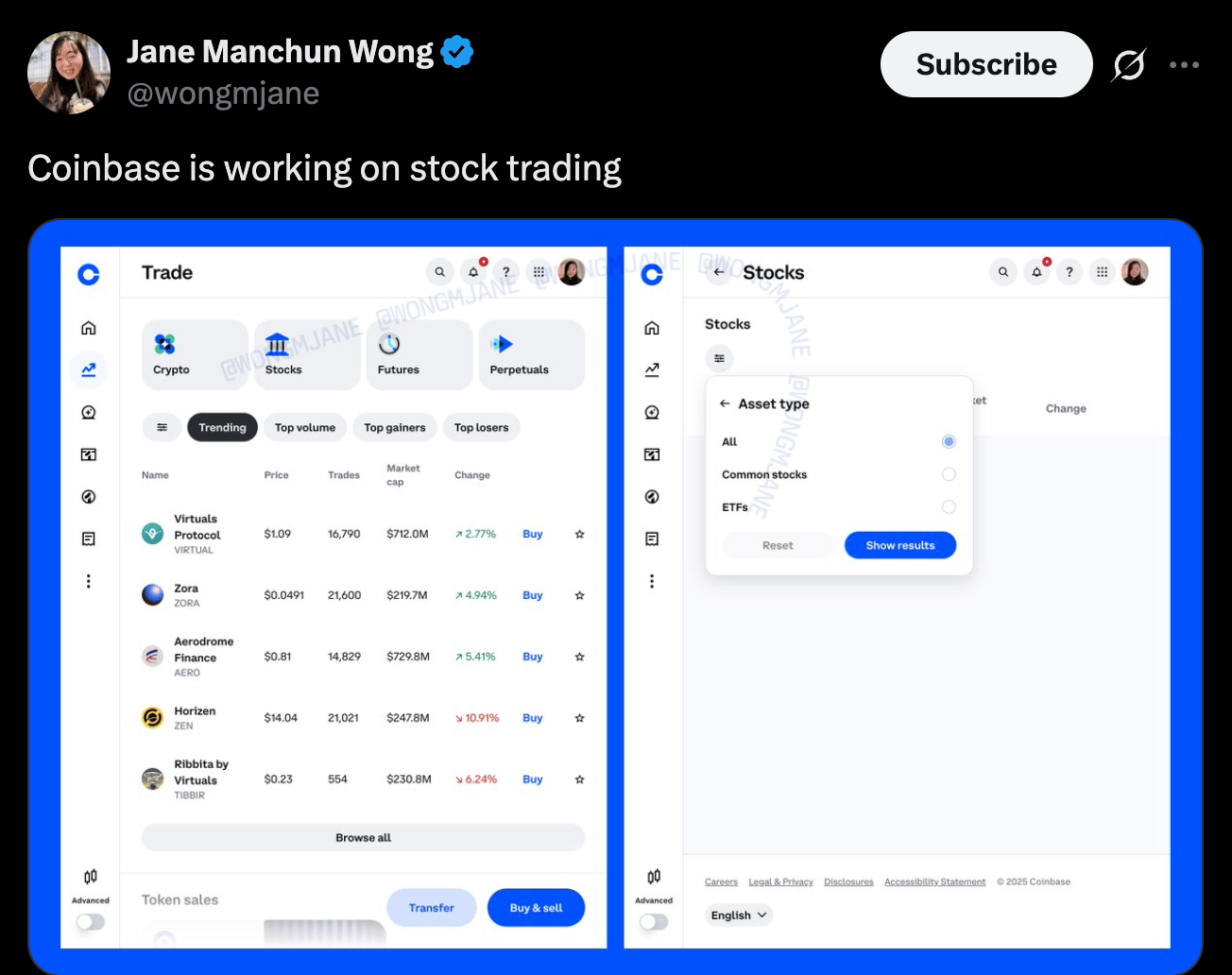

Institutional and infrastructure activity stayed surprisingly active in spite of the volatility. Fidelity pushed ahead with its SOL ETF, Bitwise launched its spot XRP ETF, and CBOE moved toward perp-style BTC and ETH futures. Coinbase continued expanding with ETH-backed loans via Morpho, a developing prediction-market and equities-trading stack, and its Aster spot listing, even as its Monad token sale lost early momentum.

RWA initiatives accelerated: Securitize partnered with Plume, New Hampshire advanced a BTC-backed muni bond, a Saudi real-estate group moved to tokenise a Trump hotel, and Tether invested in Ledn. Kraken confidentially filed for a US IPO and raised $800M at a $20B valuation, while OpenLedger launched the OPEN AI mainnet and Aztec rolled out its privacy-focused Ignition L2.

Regulators remained active across multiple jurisdictions. Tim Scott pushed for a December vote on a major crypto bill, Rep. Davidson introduced the Bitcoin for America Act, and Korea advanced both a 20–25% tax framework and new digital-asset definitions. Brazil examined taxing crypto used for cross-border payments, the IRS signaled it may soon gain visibility into foreign holdings, and the OCC opened the door for banks to hold crypto for gas-fee payments.

MSCI’s potential removal of DAT companies added another layer of index-related uncertainty, while the CFTC and Congress faced renewed scrutiny on oversight boundaries. The cultural end of the market wasn’t spared either: Punks’ floor dropped toward 90K with liquidations looming, even as communities rallied behind figures like Congressman Tim Timons publicly backing Pudgy Penguins.

Despite the heavy backdrop, selective risk pockets still found traction. HYPE and ASTER led a sharp bounce as fees surged, TNSR’s run carried it toward a $240M mark, and Base’s ecosystem saw renewed attention with the upcoming JESSE token. The broader picture remains one of consolidation after one of the most mechanically driven sell-offs of the year. Liquidity is thin, uncertainty persists, and positioning remains light — but with forced sellers largely exhausted and institutions quietly scaling back in, the market enters the weekend looking far more stable than it did at the start of the week.

Market Data Points

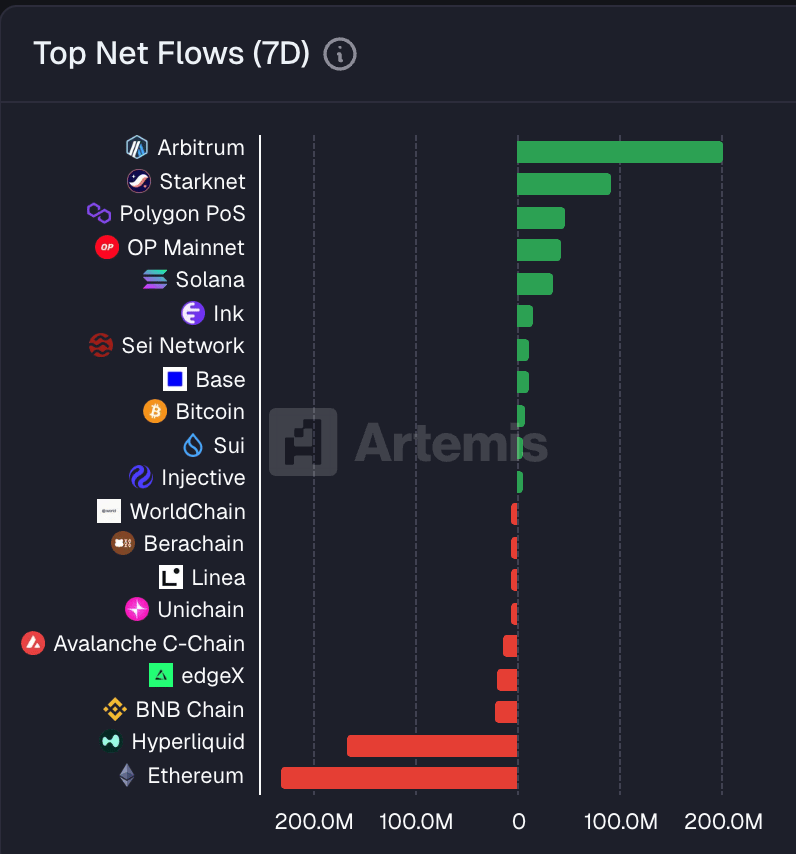

Over the last 7 days, flows rotated toward L2s. Arbitrum led net inflows (≈$200M), with Starknet, Polygon PoS, OP Mainnet, and Solana also positive. On the outflow side, Ethereum posted the largest net withdrawals, followed by Hyperliquid, BNB Chain, edgeX, and Avalanche C-Chain.

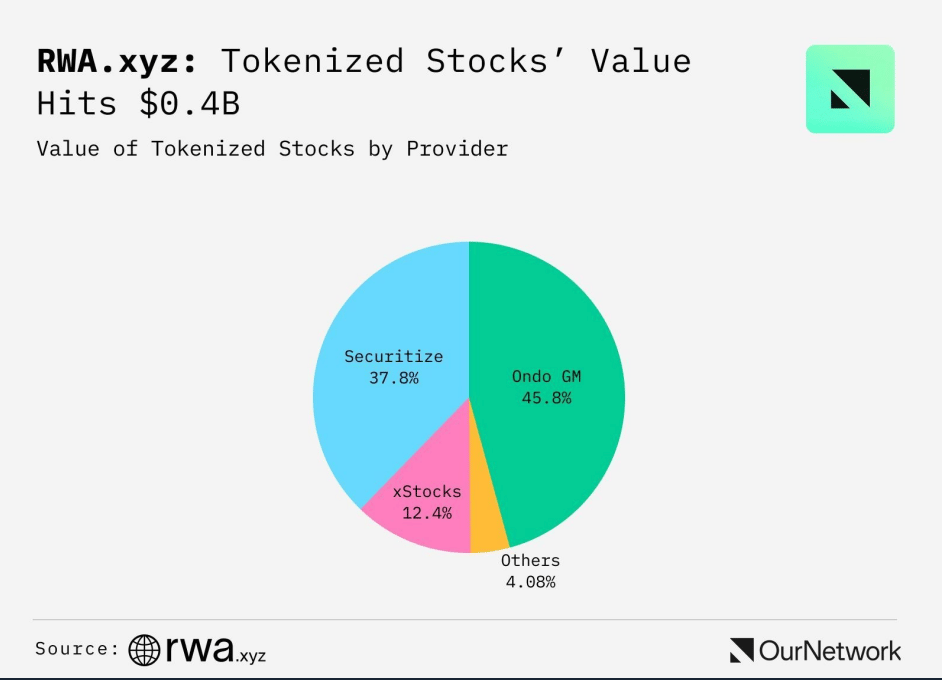

Tokenized equities are starting to look like a real segment, not a side experiment. Q3 value climbed to around $0.4B (+115%), but it’s highly concentrated: Ondo GM controls nearly half the market (~$303M, 45.8%), with Securitize close behind (~$250M, 37.8%) and xStocks a distant third (~$82M, 12.4%).

The holder data flips that picture: xStocks has 70K+ wallets versus just 4K for Superstate Opening Bell and 3.6K for Ondo, suggesting Ondo/Securitize have landed the larger-ticket, institutional-style flows while xStocks is winning distribution and retail mindshare. If that gap closes over time—either retail moves up the risk curve into Ondo/Securitize, or xStocks’ AUM catches up—this $0.4B base can scale quickly from both sides of the barbell.

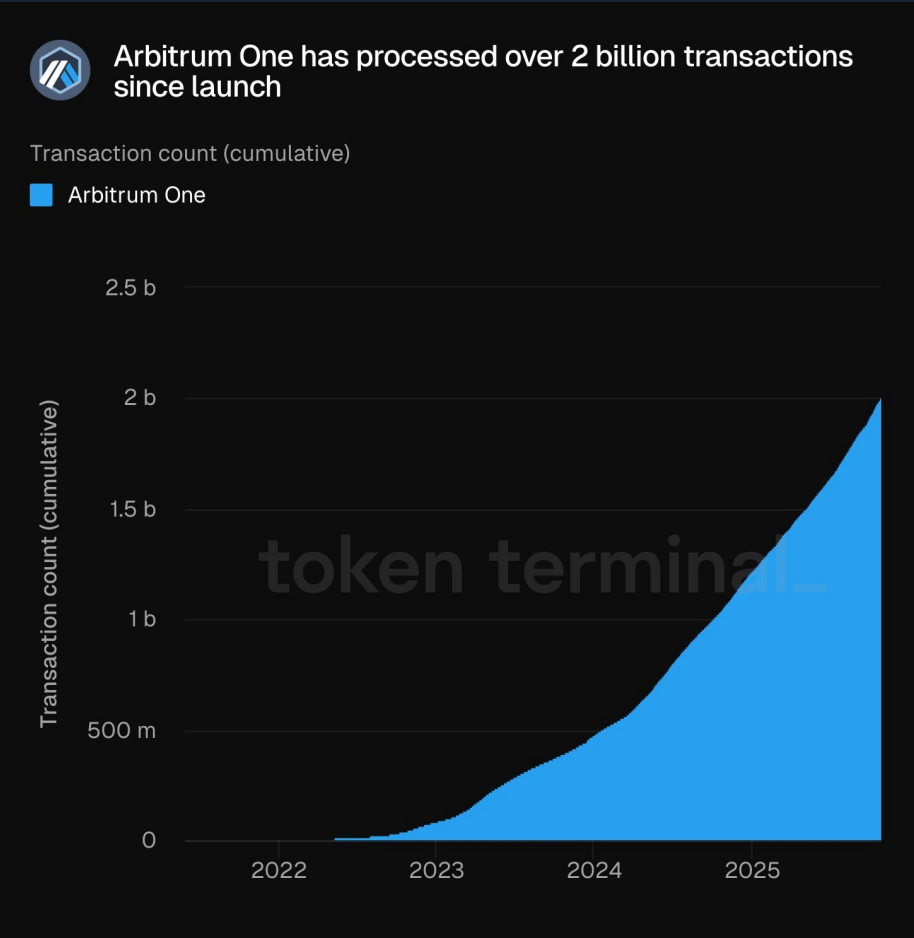

Arbitrum One recently crossed 2B cumulative transactions, with the curve steepening through 2025—evidence that rollup throughput is scaling where users actually transact. It’s a solid validator for the L2 thesis and for Arbitrum’s share of on-chain activity. Caveat: cumulative counts can hide churn, so the next checks are sustained DAUs, fee revenue, and settlement volume back to L1. If those hold up, this isn’t just bursty growth—it’s durable usage.

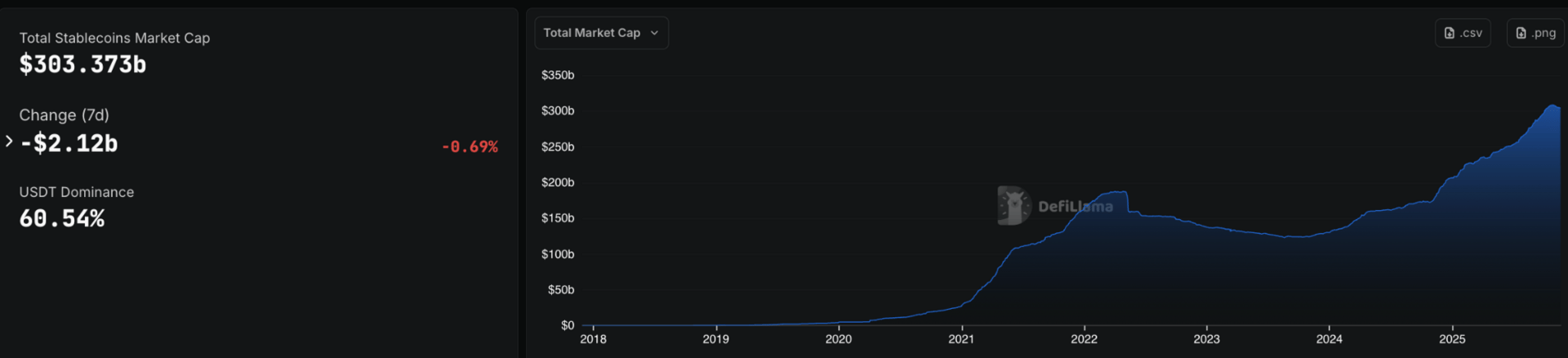

Stablecoin supply is slipping alongside the risk-off tape. Total cap sits near $303.4B, down $2.12B (-0.69%) over the last week, with USDT at ~60.5% dominance. In weak market conditions, a contracting stablecoin base usually means net redemptions and less incremental “dry powder” circulating on-chain—one reason rallies fade quickly. It’s not a breakdown (levels remain historically high), but the signal is cautionary: sustained upside typically coincides with stablecoin growth, while continued shrinkage would keep liquidity tight and breadth thin.

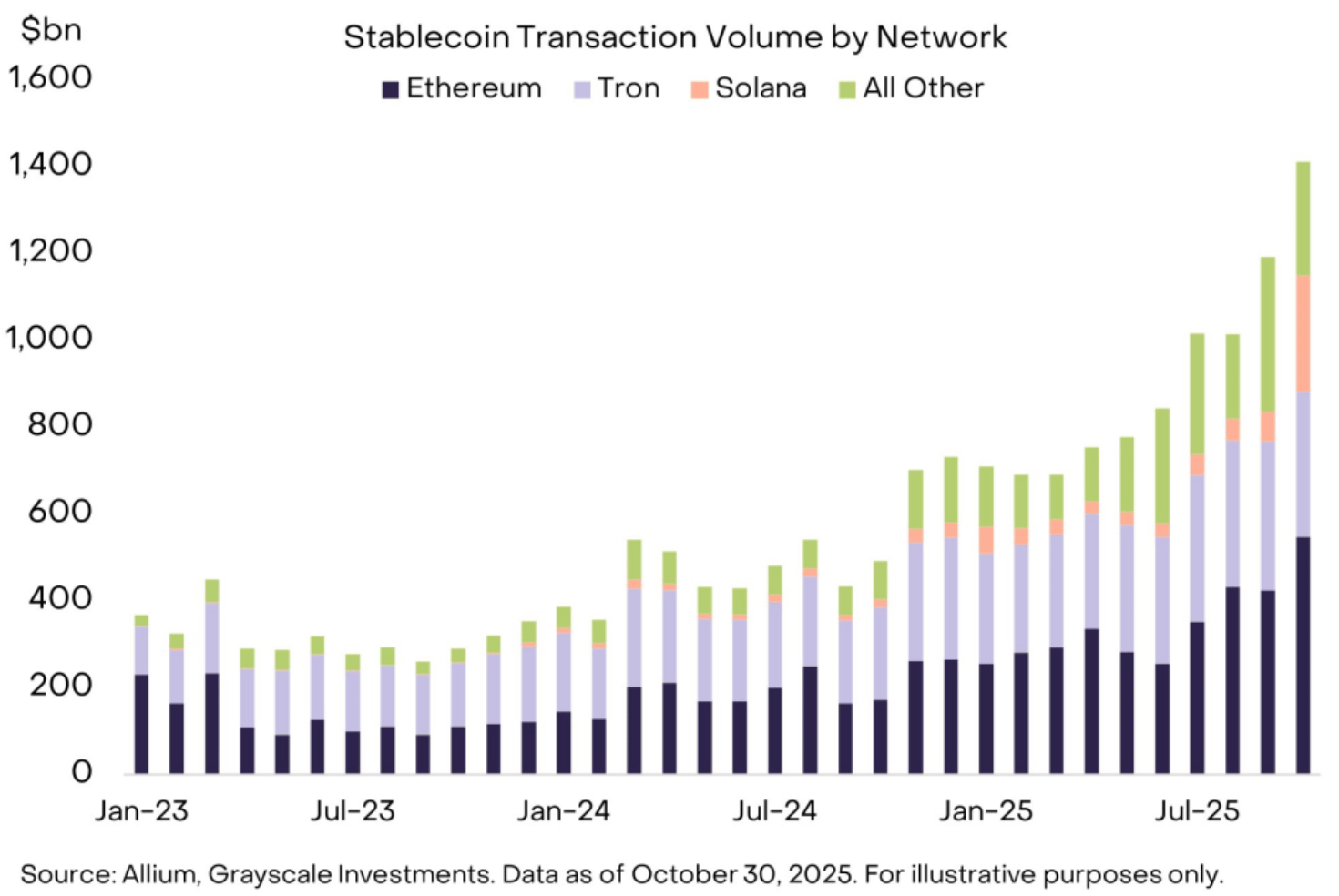

Stablecoin activity just printed a new peak: about $1.4T in on-chain volume for October. Flows remain anchored on Ethereum and Tron (remittances, CEX/OTC settlement), with Solana carving a visibly larger slice and “other” chains climbing as rails diversify.

The interesting bit is velocity: volumes are making highs even as total stablecoin cap has softened week-to-week, which implies faster turnover rather than fresh supply. That lines up with a volatile October—more hedging, redemptions/issuance cycles, and DEX/CEX arb moving dollars at speed. For markets, higher stablecoin throughput usually supports liquidity in perps and spot, shortens basis dislocations, and keeps risk transfer efficient even when prices chop. Sustainability from here depends on whether velocity stays elevated or we see renewed supply growth to pair with it.

Majors & Memes

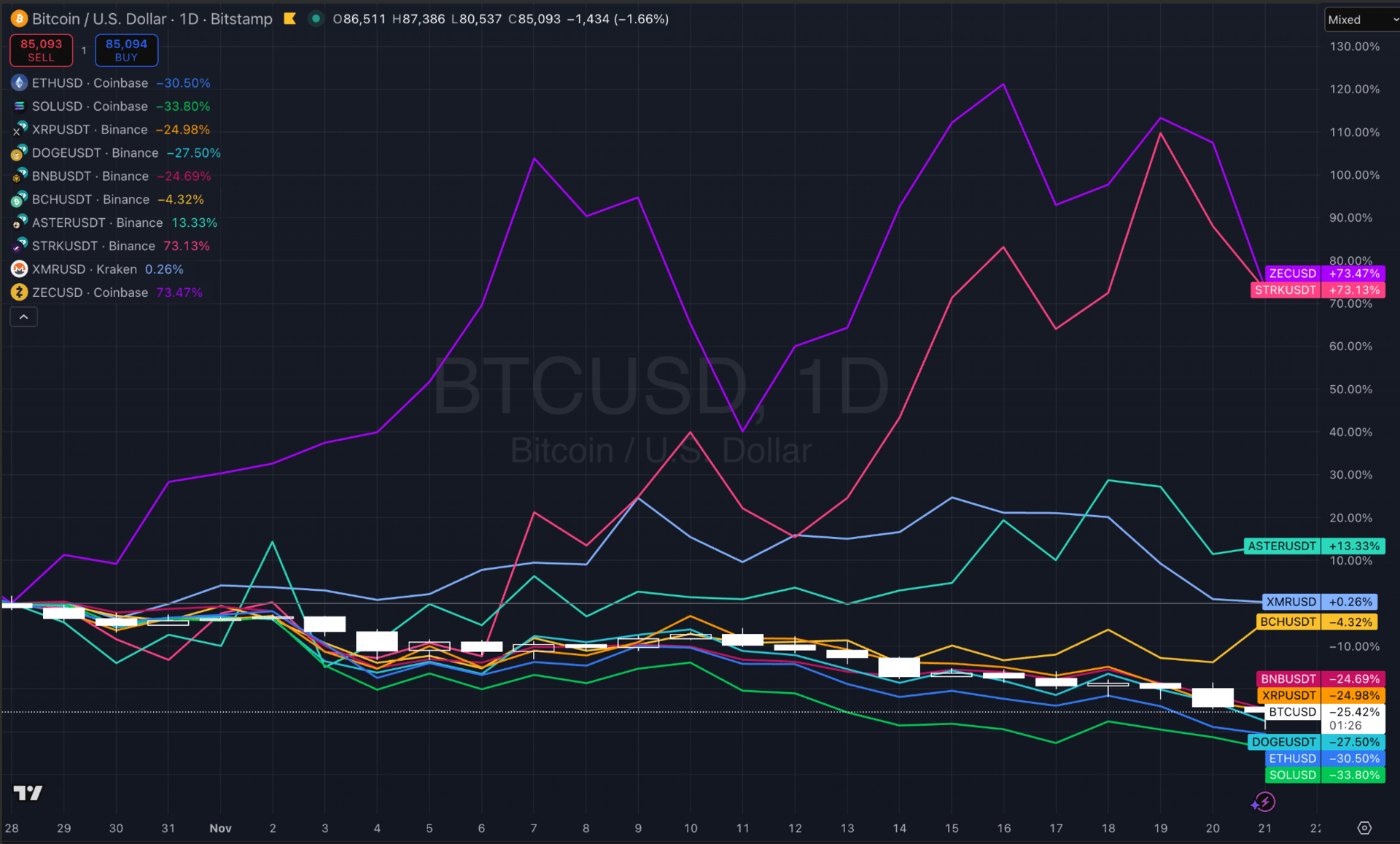

Majors spent the week on the back foot, with almost every large cap extending the drawdown. BTC slid about 10.4%, while ETH underperformed slightly with a 12.6% drop. BNB and SOL weren’t far behind, down roughly 9.7% and 8.6%, and high-beta names like DOGE and ADA absorbed some of the heaviest damage at 12.1% and 18.7%. XRP also retraced sharply, off 14.3%, and TRX held up only marginally better at –6.0%. The profile across the top of the board points to a clear de-risking phase where even the most liquid names struggled to find a bid.

Below the majors, strength was narrow and highly selective. BCH was one of the only larger names to put in a green week, up around 10.5% and again behaving like a relative-strength outlier. Among midcaps, ASTER, WBT, STRK, APEPE and REAL all posted double-digit gains, ranging roughly from 9% to over 18%, with follow-through interest also visible in PI, MERL, MYX and ASI. The common thread is traders concentrating on idiosyncratic narratives and high-momentum stories rather than expressing broad market risk, a typical pattern when headline sentiment is soft but pockets of speculation remain active.

The laggard side of the ledger was much more crowded. CC fell about 30.4%, PUMP dropped 22.8%, and a long list of liquid alt L1s and narrative plays followed lower: ICP, NEAR, SUI, ONDO, MNT, ADA, APT, VET, DOT, PEPE and WLD all declined in a rough 17–22% band. In the wider crypto universe, selling pressure was even more aggressive, with SOON down 71.3% and names like CCD, SYRUP, H, ATH, TIA, MORPHO, ZBCN, VIRTUAL, ZK, IP and WAL sliding 22–36%. Combined with the weakness in majors, this points to a market still firmly in risk-off mode, where capital is being pulled from higher-beta segments and only a handful of standout stories are managing to defy the broader trend.

Smart Money Accumulation

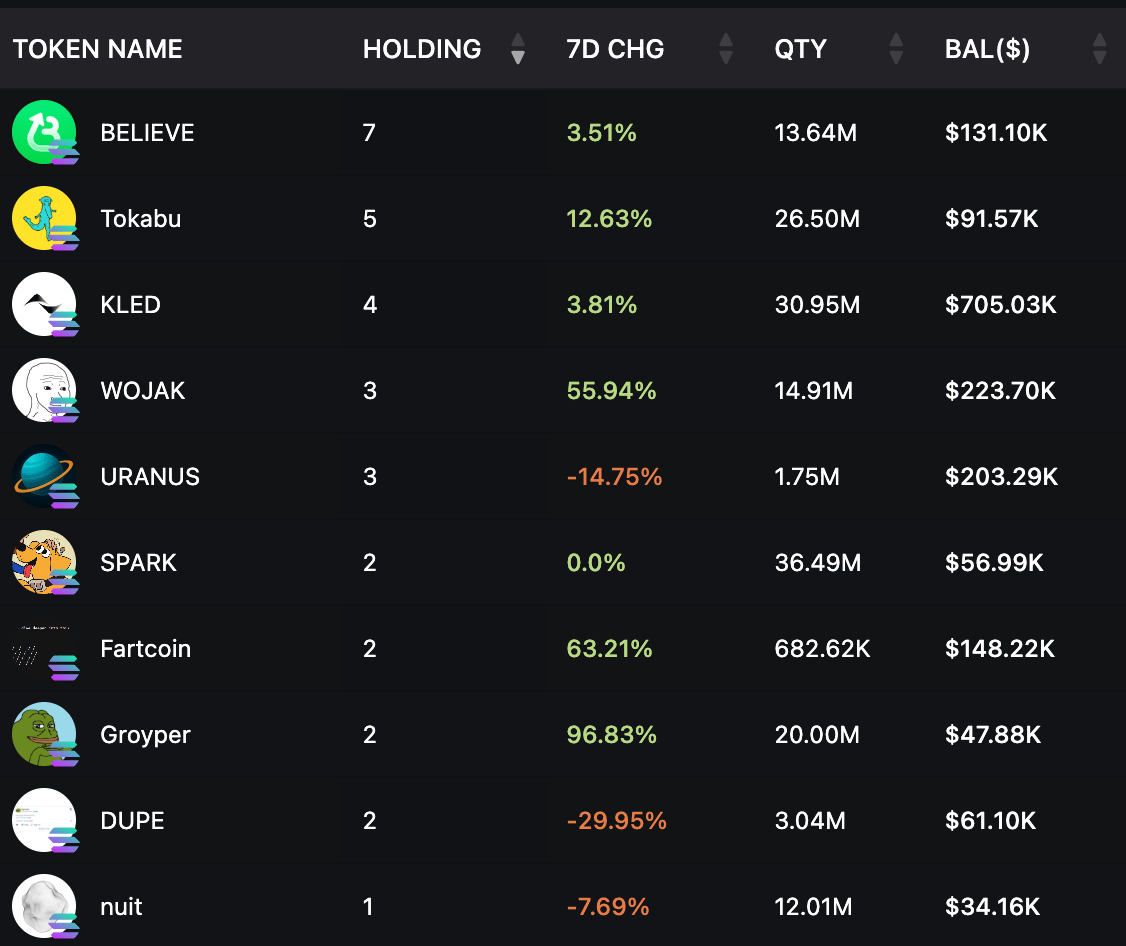

Across both ecosystems, the tone is the same: smart money has stepped back, scaled down, and is trading far less than in previous weeks. The Solana side already showed how sharply engagement has collapsed, with wallet counts flat, balances contracting, and only tiny pockets of selective rotation surviving. What was last week a cautious but still functioning market — with names like BELIEVE, SURGE and SPARK attracting incremental flows — has now turned into broad position shrinkage and a clear preference to preserve capital rather than chase narratives. That backdrop sets the stage for the EVM picture, which mirrors the same withdrawal of risk.

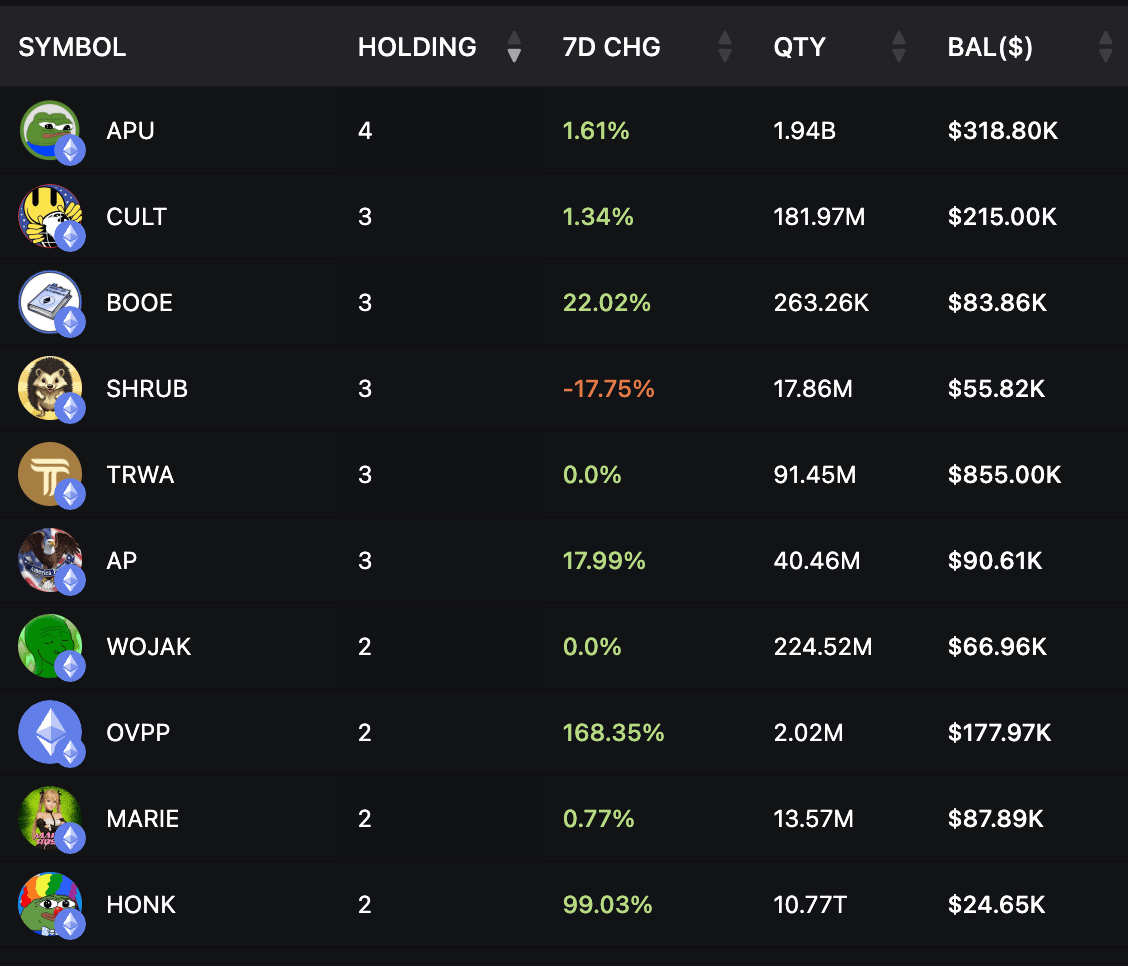

In the EVM meme ecosystem, activity has thinned even further. Last week still had a handful of modest adds across CULT, BOOE, SHRUB and AP, but this week the book is mostly static, with balances drifting lower and wallet behaviour signaling that investors are simply waiting out volatility. Only a few names showed meaningful accumulation. OVPP was the standout, with balances jumping 168% to roughly $177.97K — the strongest impulse buy and one of the only scaled allocations in an otherwise frozen market. HONK posted a 99% lift but still sits at a small $24.65K line, while BOOE, AP, APU, CULT and MARIE saw mild green but nothing that signals conviction.

Trimming was minimal but symbolic of the broader mood: SHRUB was the only clear reduction at –17.75% to around $55.82K, and everything else — TRWA, WOJAK, and similar core positions — barely moved. The combination of shrinking balances, an absence of high-conviction adds, and the contrast with last week’s slightly livelier rotation all point to the same conclusion as the Solana basket: smart money is in full risk-off mode. Capital is tight, participation is low, and positioning is being kept deliberately small until majors stabilize and the macro picture stops deteriorating.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply