- Crypto Pragmatist by M6 Labs

- Posts

- Liquidity Returns, Crypto Still Building

Liquidity Returns, Crypto Still Building

Hard Assets At Highs, ETF Flows Return, Institutions Continue Accumulation

The Coiners

January 17, 2026

GM Anon!

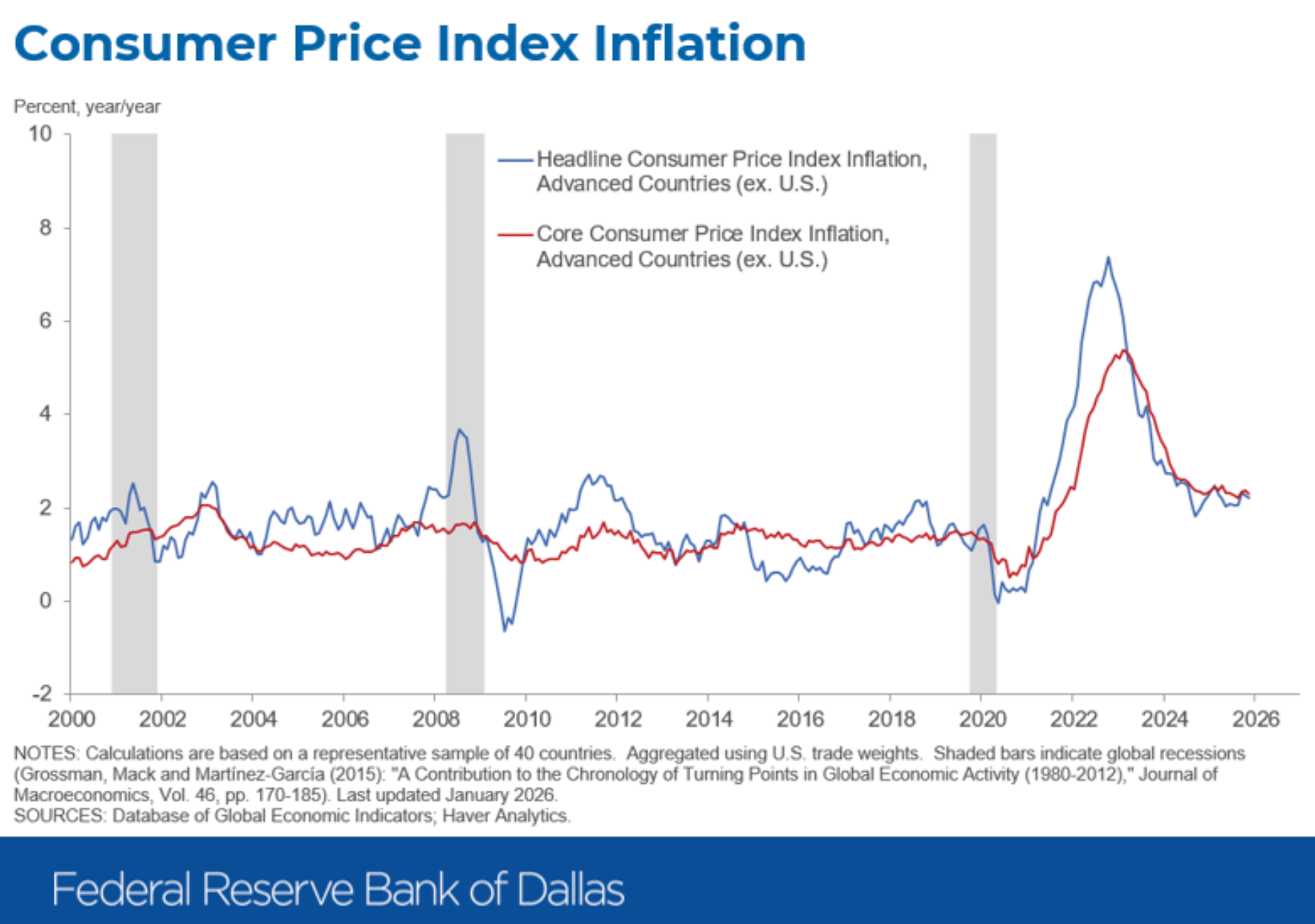

Markets continue to send mixed but increasingly constructive signals. Macro conditions are easing at the margin, with softer inflation data, improving liquidity expectations, and renewed strength in hard assets pointing to a backdrop that remains supportive for risk. Equities are holding up despite ongoing rotation, while gold, silver, and copper pushing to fresh highs underline persistent demand for inflation hedges and real assets.

Crypto is responding, but in a measured way. BTC pushed to a two-month high before stalling, leaving price range-bound even as ETF flows turned decisively positive and institutional activity picked up. Spot demand is quietly absorbing supply, volumes have returned, and structural adoption continues to advance, yet participation remains selective rather than euphoric. The gap between improving flows and cautious price action is widening, and how that tension resolves is likely to define the next phase of the market. Let’s dive in!

TLDR

Macro volatility eased into a more supportive tone as CPI came in cooler, jobless claims undershot estimates, and equities stabilized despite ongoing rotation and policy noise.

Hard assets surged, with gold, silver, and copper at all-time highs, reinforcing demand for inflation hedges and liquidity-sensitive positioning.

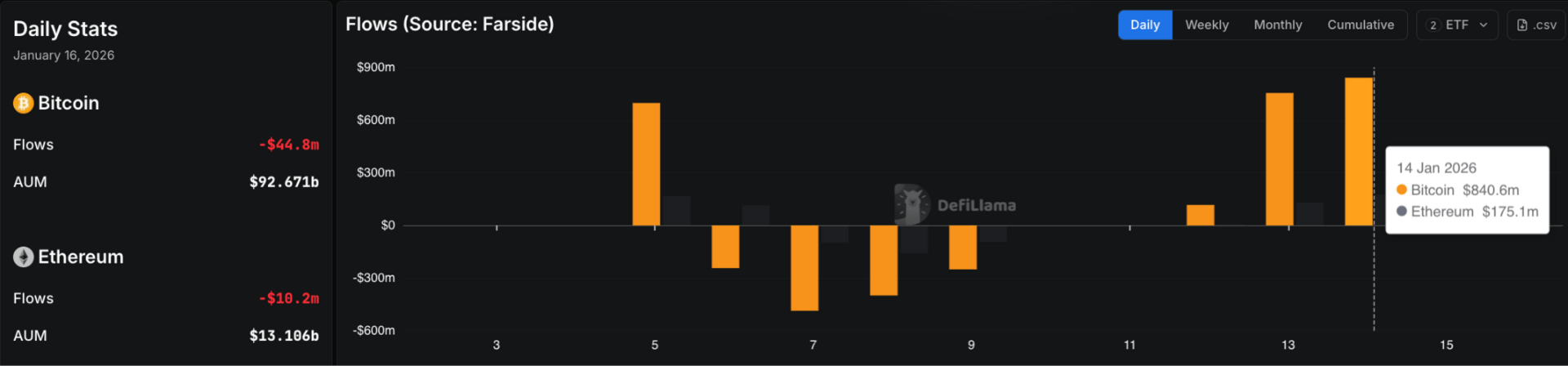

BTC pushed to a two-month high alongside a clear turnaround in ETF flows, marking the strongest inflow week in roughly three months.

BTC upside is being led by spot demand rather than leverage, pointing to healthier structure and stronger hands driving price.

ETH lagged BTC on price but saw its staking queue rise to the highest level since 2023, signaling longer-term positioning.

SOL and BNB benefited from a pickup in activity, with on-chain usage reaching a nine-month high and volumes returning across the market.

Institutional adoption continued to deepen, with banks, asset managers, and treasuries expanding crypto exposure and infrastructure.

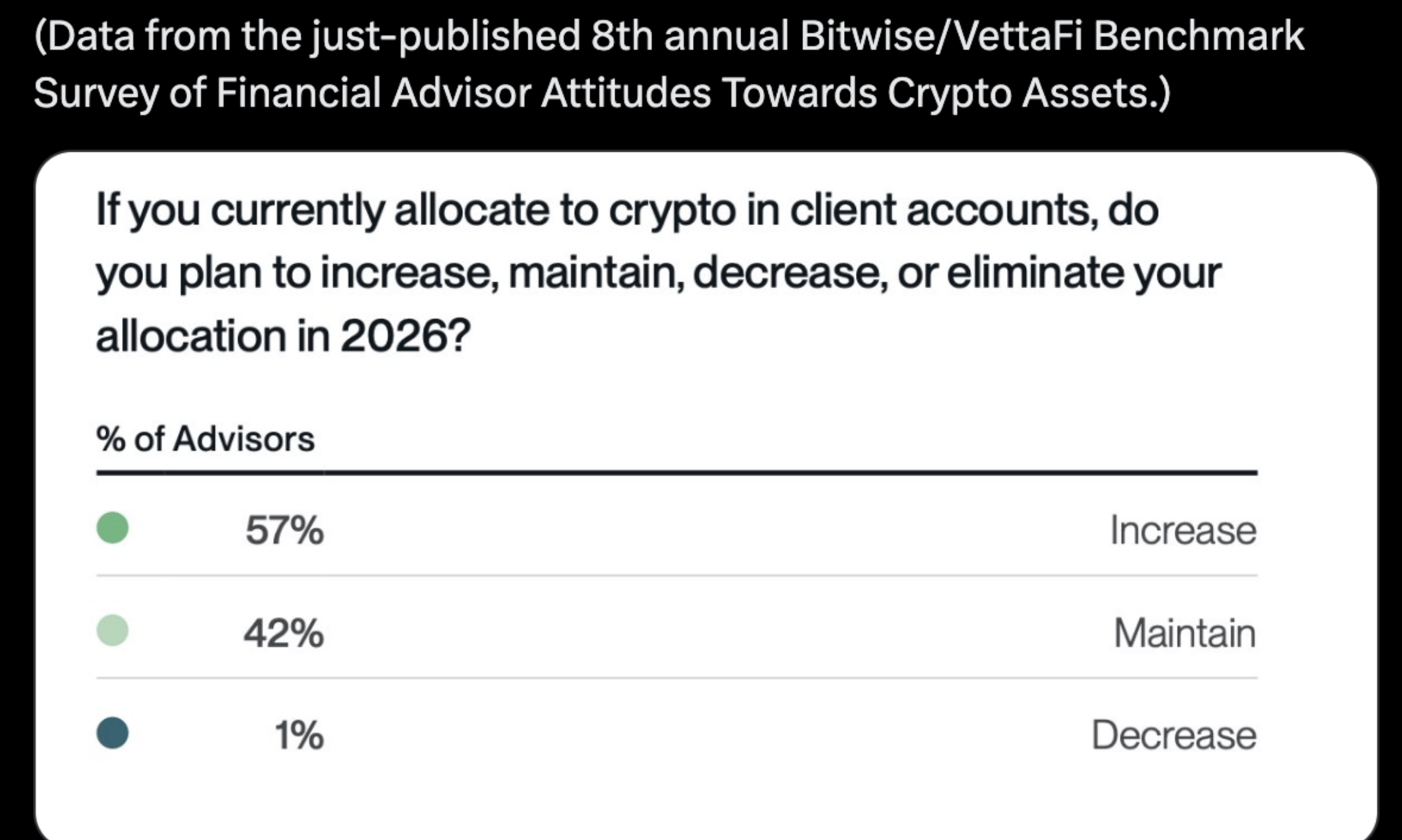

Advisor surveys show overwhelming intent to maintain or increase crypto allocations into 2026, supporting structural demand.

Market breadth remains selective, with strength concentrated in a few leaders and momentum pockets while many tokens lag.

🚀 The Easiest Perp DEX Airdrop Strategy

Perp DEXes remain one of the clearest structural opportunities heading into 2026. They generate real volume, real fees, and historically reward early, consistent participation — not short-term speculation. As we’ve seen this cycle, the biggest outcomes have gone to users who positioned early, stayed active, and focused on execution rather than noise.

If you want a practical, low-friction way to participate, we’ve put together a step-by-step breakdown of the simplest perp DEX airdrop strategy, designed to help you generate qualifying volume while staying market-neutral. It’s the same framework early users have used across multiple perp platforms, adapted for where we are in the cycle today.

This isn’t about guarantees. It’s about understanding where incentives are forming early and applying a repeatable process while participation is still relatively small. We’ll continue to share updates, refinements, and new opportunities as this perp DEX cycle develops.

The Coiners

Market Update

Markets moved through another volatile but constructive week, with macro signals pulling sentiment in both directions before settling into a more supportive tone. US equity futures swung around inflation data, initially slipping on PPI and ahead of CPI, then stabilizing as CPI came in cooler than expected and jobless claims undershot estimates.

Beneath the surface, rotation remained a dominant theme, with tech facing intermittent sell pressure even as broader indices found support from banks and value exposure. Policy noise stayed elevated, from renewed uncertainty around Trump-era tariffs and fresh chip export restrictions to headlines around the DOJ opening a criminal investigation into Chair Powell, which briefly rattled risk assets before Powell publicly reaffirmed he would remain in his post.

Against that backdrop, the move to fresh all-time highs in gold, silver, and copper signaled persistent demand for hard-asset exposure and reinforced the sense that liquidity and inflation hedging remain central to positioning.

Crypto tracked that improving macro tone with clearer follow-through. BTC pushed to a two-month high as inflows accelerated, coinciding with a notable turnaround in ETF activity and the largest net inflow seen in roughly three months. That shift marked a change from the recent stop-start pattern and suggested institutional demand was re-engaging rather than fading.

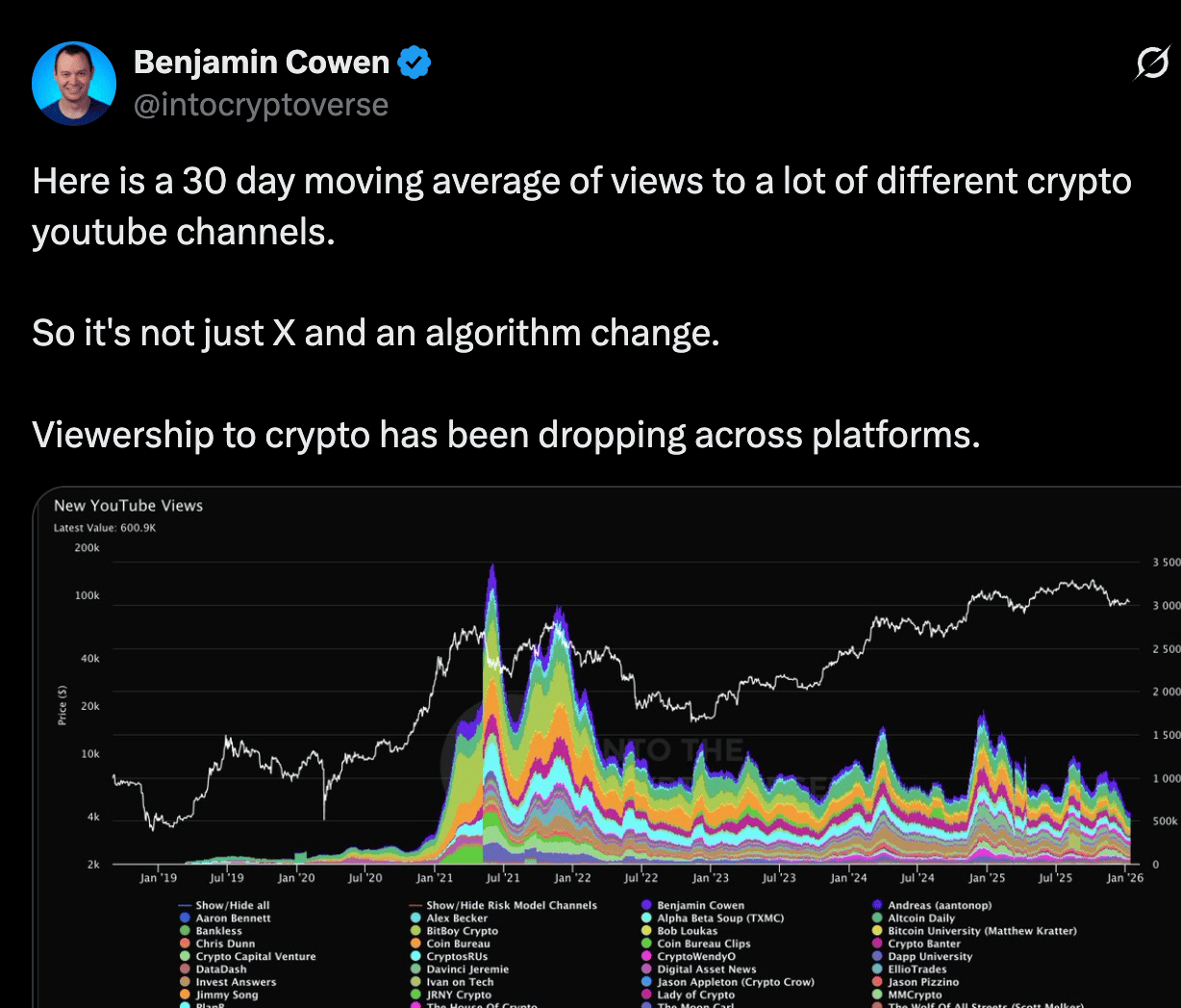

ETH lagged BTC on price but saw a sharp buildup in its staking queue, the highest since 2023, pointing to longer-term positioning even as spot performance lagged. SOL and BNB benefited from a broader pickup in activity, with on-chain usage rising to a nine-month high, while overall trading volumes returned across the market, improving liquidity conditions after a quieter stretch. Retail signals, however, remained subdued, with crypto YouTube viewership falling sharply, reinforcing that this move continues to be driven from the top down rather than by speculative crowd behavior.

Institutional and infrastructure developments continued to shape sentiment. Wells Fargo’s decision to allow BTC as collateral for loans, BNY Mellon activating tokenized deposits, State Street expanding its tokenization efforts, and Galaxy closing a $75M tokenized CLO all highlight the steady normalization of crypto within traditional financial plumbing.

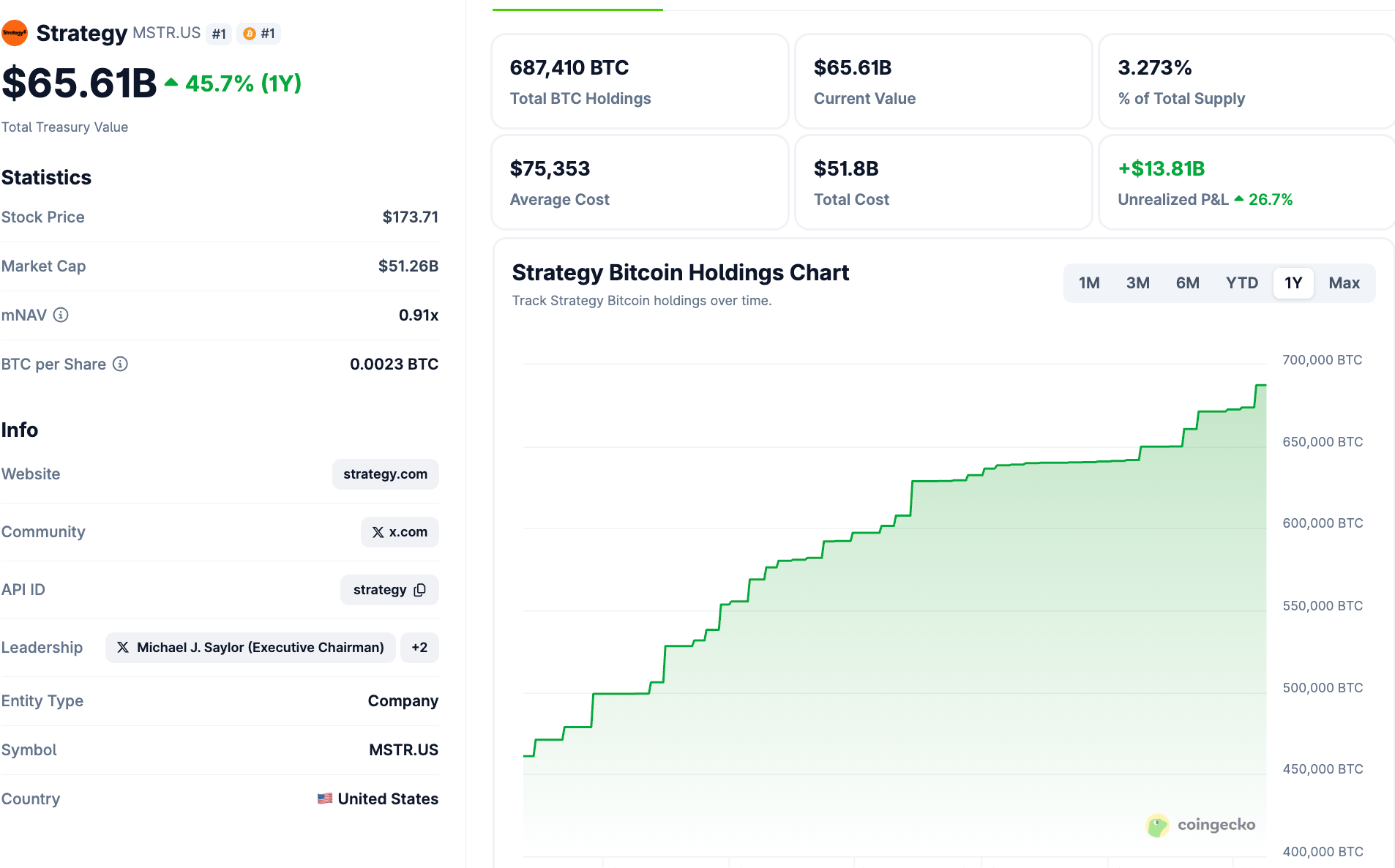

Strategy added another $1.25B of BTC to its treasury, while Standard Chartered doubled down on its constructive stance, calling 2026 a pivotal year for ETH and outlining plans for a crypto prime brokerage. Market access widened further with CME adding new crypto derivatives, Bitwise launching a LINK ETF, and Deribit rolling out USDC-settled options for AVAX and TRX. At the same time, inflow expectations remained constructive, with JPMorgan flagging further increases into 2026, even as political friction around market structure and stablecoin legislation continued to delay clarity in the US.

Regulation and corporate activity remained noisy but directional. Crypto bills advanced in draft form but faced repeated postponements, stablecoin provisions remained contested, and lawmakers pressed regulators over enforcement retrenchment and developer protections.

Internationally, momentum was more decisive, with Ripple securing regulatory approvals in the UK and Europe, South Korea lifting its corporate crypto investment ban while tightening exchange rules, and multiple jurisdictions advancing tokenized securities frameworks. Elsewhere, privacy assets diverged sharply, with XMR hitting new highs before retreating as Dubai moved to ban privacy coins and scrutiny increased, while ZEC lagged despite the SEC ending its probe into the Zcash Foundation.

Taken together, the week reflected a market where macro pressure is easing, institutional participation is broadening again, volumes have returned, and crypto is beginning to respond through renewed flow, improving liquidity, and deeper structural engagement rather than speculative excess.

Market Data Points

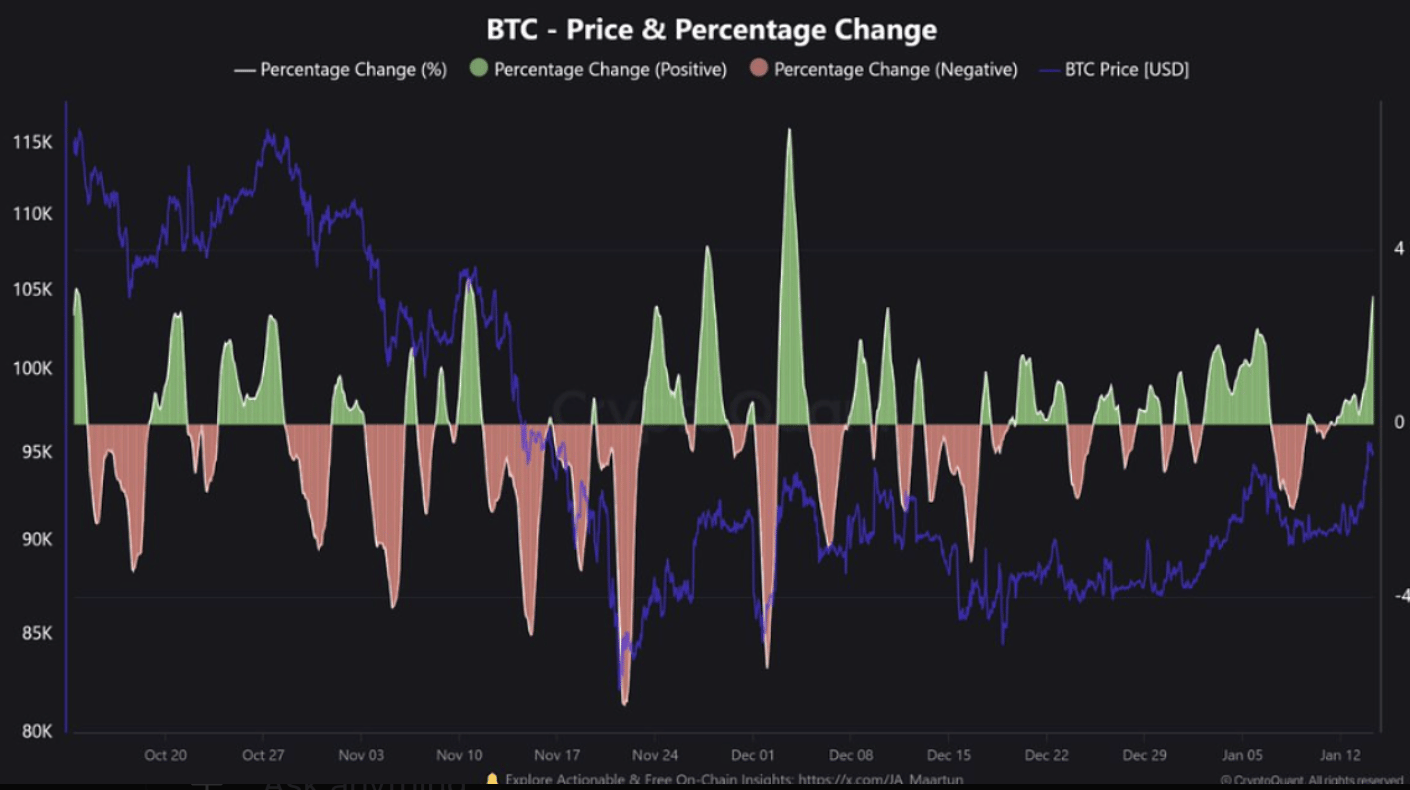

Recent upside in BTC appears to be driven primarily by spot market activity rather than leverage. Positive percentage changes increasingly align with price stabilization and recovery phases, while pullbacks have been shorter and less forceful. That pattern suggests buyers are absorbing supply on spot rather than relying on futures-driven momentum.

When advances are supported by spot demand instead of expanding leverage, it generally reflects healthier market structure, with stronger hands leading the move rather than short-term positioning.

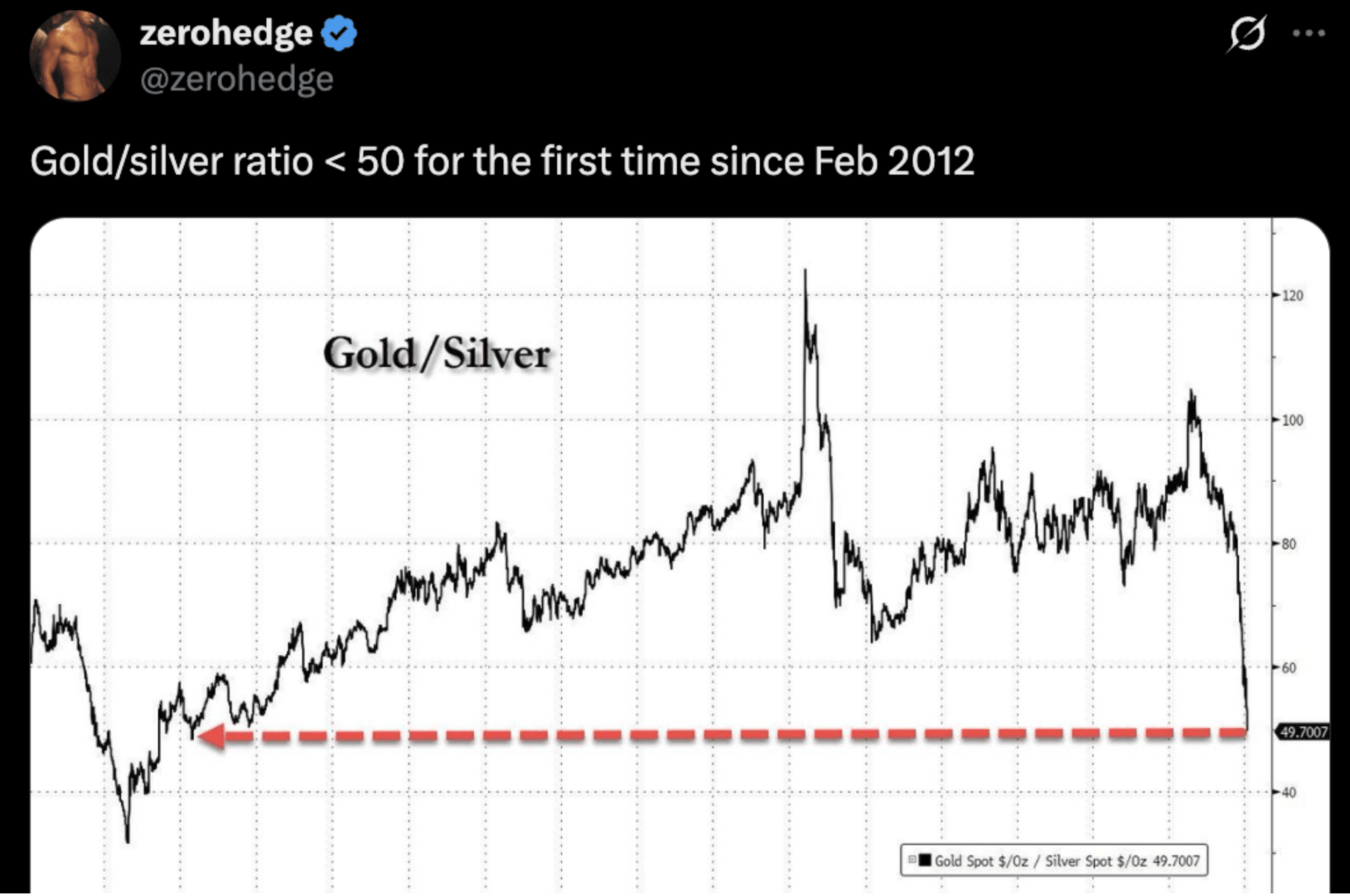

The gold-to-silver ratio has fallen below 50 for the first time since 2012, marking a meaningful shift in relative performance between the two metals. Historically, sustained compression in this ratio reflects rising risk appetite within hard assets, with silver outperforming as capital rotates toward higher-beta exposure.

Moves like this tend to coincide with reflationary backdrops and stronger speculative demand, rather than defensive positioning. In a broader macro context, this kind of ratio breakdown often signals that liquidity is favoring growth- and volatility-sensitive assets over pure capital preservation.

Survey data from financial advisors already allocating to crypto shows a strong skew toward continued or increased exposure in 2026. An overwhelming majority plan to either raise allocations or keep them unchanged, with only a negligible share indicating any intention to reduce exposure.

This points to growing institutional comfort with crypto as a portfolio component, where the debate has shifted away from whether to hold it at all and toward sizing and timing. In practice, that kind of stickiness on the advisor side tends to support demand through market pullbacks, as allocations are treated more like strategic exposure than opportunistic trades.

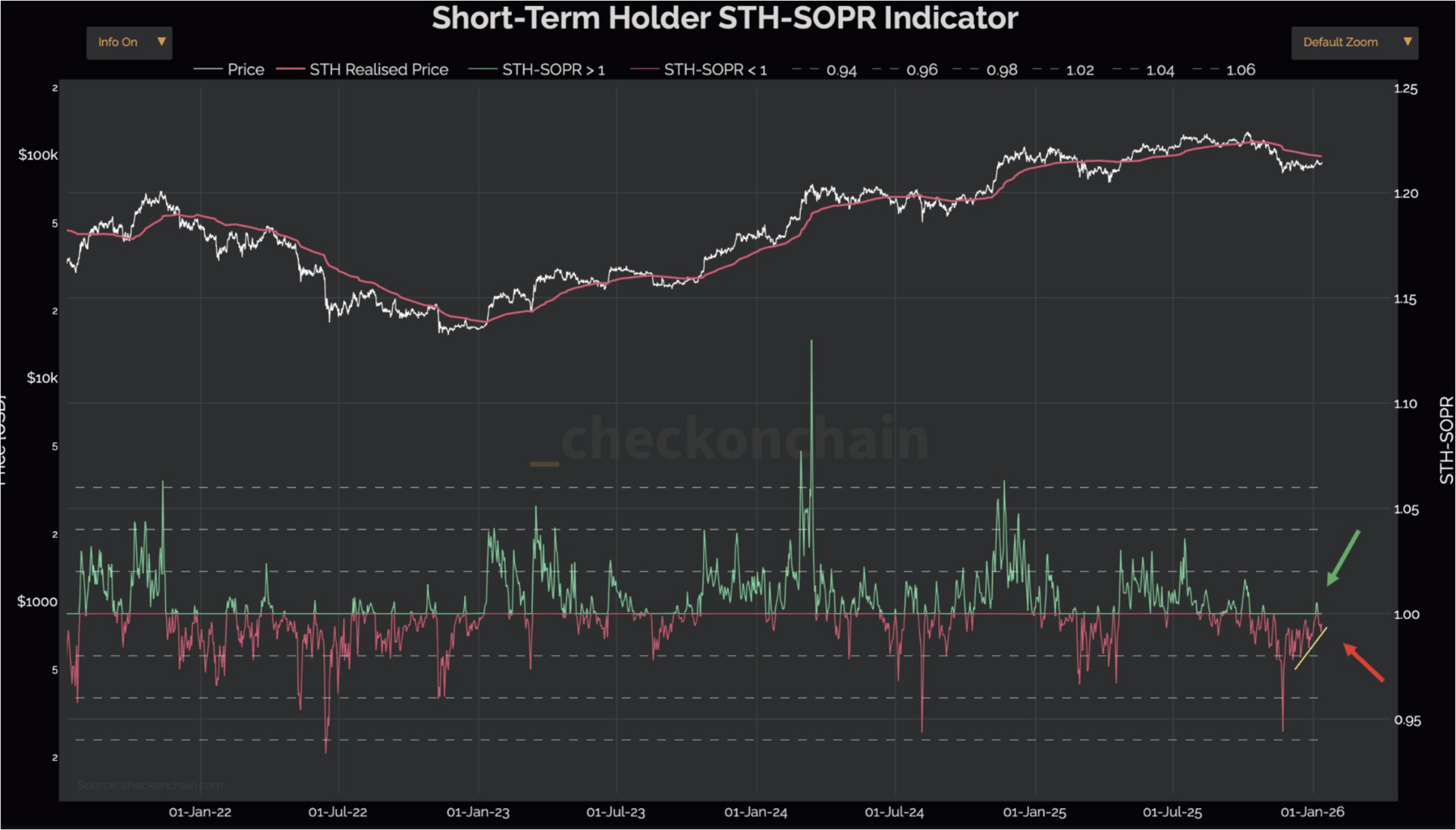

Short-term holder SOPR has slipped back below 1, indicating that recent sellers are realizing losses rather than distributing into strength. This typically reflects late entrants being flushed out as price chops sideways, rather than confident profit-taking. When STH-SOPR sits below 1 during consolidation, it usually points to ongoing base-building, with weaker hands exiting and supply gradually transferring to more patient holders. In that context, the data continues to support the view that the market is working through positioning rather than transitioning into a fully extended phase.

Majors & Memes

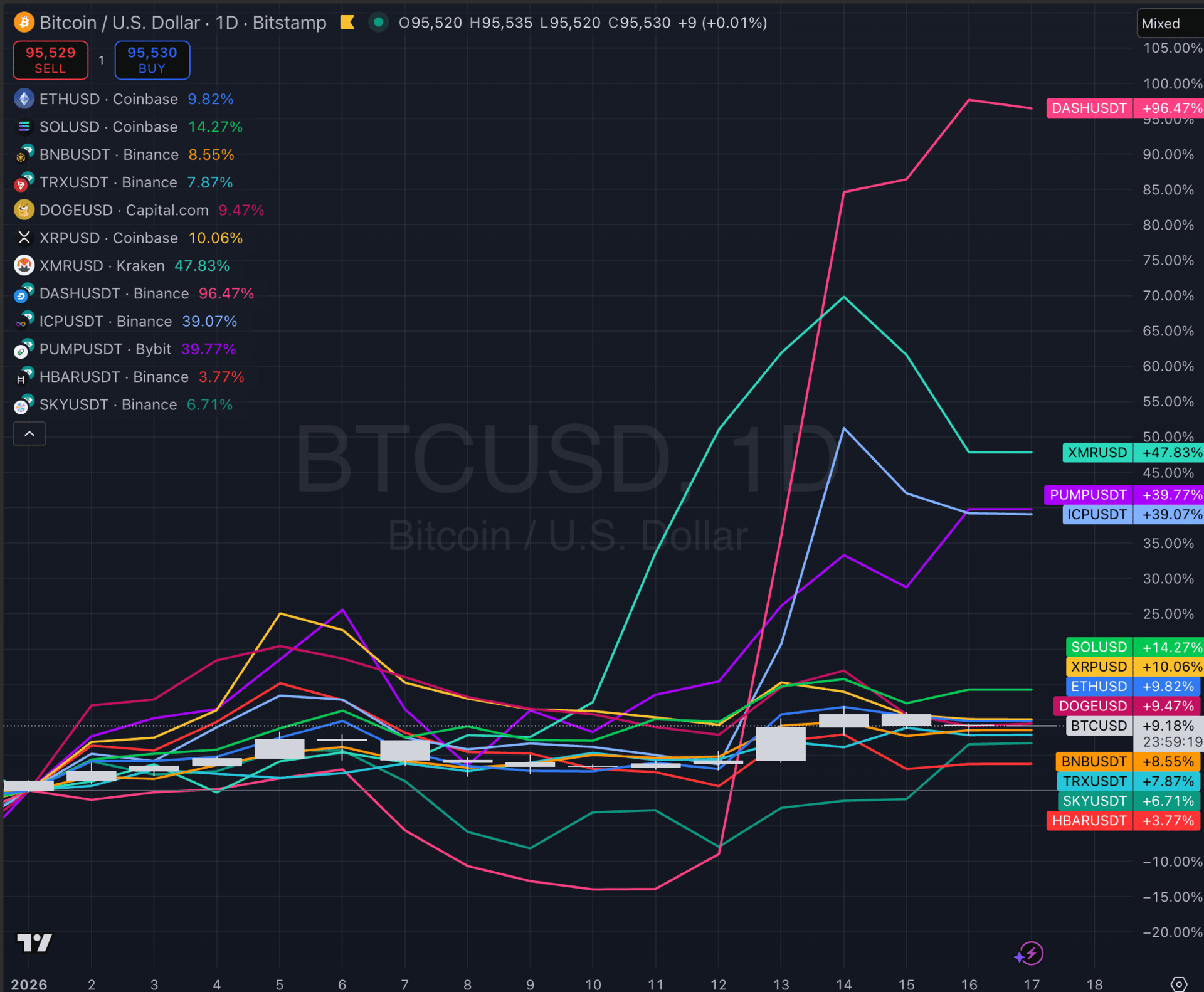

Majors ended the week with a broadly constructive but still uneven tone. BTC was higher over the last seven days and kept a steady upward profile, while ETH did a bit better on a relative basis, hinting at some rotation back toward the second largest major rather than a full risk-on surge. BNB and SOL both held up well and stayed among the cleaner large-cap tapes, with TRX also finishing in positive territory on a calmer, steadier path. The weaker pockets were XRP and DOGE, both fading while the rest of the top complex stayed supported, which kept leadership narrow and selective.

Outside of majors, upside was concentrated in a small cluster of higher-beta and idiosyncratic names. DASH was the clear outlier with a standout week, while XMR and ICP followed with strong double-digit advances. A second tier of winners including PUMP, HASH, and SKY also pushed higher, reinforcing that the market’s best returns were found in momentum pockets rather than across the broader alt field. The dispersion among gainers remained wide, but the common thread was rotation into names that were already moving, with traders leaning into follow-through where it existed.

On the downside, losses were more evenly spread across recognizable tokens. LTC and POL were among the heavier drags, with BCH and ENA also slipping, while ONDO, WLD, ATOM, KAS, and PEPE remained under pressure. A number of smaller caps saw sharper drawdowns, which fits a tape where rallies are being traded rather than chased, and where bid support can thin out quickly once momentum stalls.

The broader read-through is that, despite a handful of outsized breakouts, overall breadth still looks limited. Strength is showing up in bursts and rotating quickly, while a meaningful portion of liquid names struggle to hold bids. That said, the macro backdrop still appears supportive of a broader breakout attempt if risk appetite stays firm, and the way leadership is holding in BTC, ETH, BNB, and SOL keeps that outcome on the table. Until participation widens beyond a few leaders and the laggards stabilize, the market still reads more like consolidation with selective momentum than a clean, durable trend.

Smart Money Moves

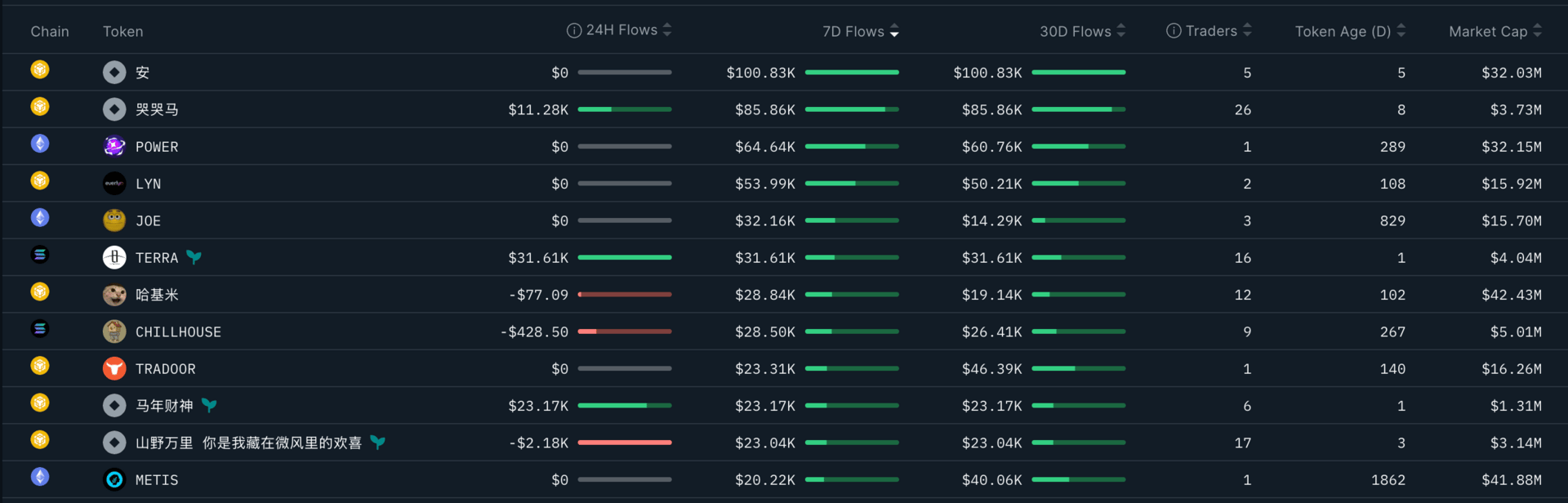

Smart money activity over the last seven days continues to look selective rather than aggressive, extending a pattern that has largely defined this market since around October 10. The week was quiet in absolute terms, but that quiet has been the regime for months, with capital rotating carefully rather than chasing momentum. Within that backdrop, a small set of names stands out for showing clean 7-day inflows that also remain supported on the 30-day window, which reads more like patient position-building than short-term trading. POWER, LYN, JOE, and TERRA fit that profile, with buying that looks steady and intentional rather than headline-driven.

A distinct feature this week is the presence of multiple tokens listed under Chinese-language names, including 安, 哭哭马, 哈基米, 马车财神, and 山野万里 你是我藏在微风里的欢喜. This activity is concentrated on BNB Chain, and the combination of sustained net inflows with a relatively small set of participants points to whale-driven accumulation outside the usual English-speaking venues. It also lines up with what a lot of traders have been observing on the ground: more effort to bridge into non-English communities and liquidity pockets where attention can be earlier and price discovery can be more fragmented. When flows start showing up in these zones, it’s often a signal that risk appetite isn’t gone, it’s just operating off the main stage.

Zooming out, buyer distribution reinforces the same theme. A few names are clearly driven by concentrated wallets, while others show slightly broader engagement, but still nothing resembling broad speculative heat. TRADOOR and METIS stand out for stronger 30-day accumulation relative to their most recent weekly pace, which can point to earlier positioning ahead of a rotation rather than a late momentum chase. Taken together, the data still reflects a cautious tape, but one where capital is quietly finding its targets, and where the most interesting activity is increasingly happening in smaller, less crowded corners of the market.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply