- Crypto Pragmatist by M6 Labs

- Posts

- Macro Shocks Hit, BTC Holds

Macro Shocks Hit, BTC Holds

Macro Volatility Rises, Leverage Resets, ETFs Pause

The Coiners

January 24, 2026

GM Anon!

BTC spent the week moving from momentum into digestion. What started as a solid hold near the top of the range gave way once macro stress hit, and BTC ended up consolidating instead of following through higher. The drop itself was sharp, but the tell was in the follow-through: leverage got cleaned out, liquidations stayed contained, and price found its footing around higher-timeframe support.

On-chain looks like rotation under pressure, not a market top, with short-term holders doing the selling and longer-term cohorts staying steady. For now, BTC is range-bound and trading macro first. Let’s dive in.

TLDR

BTC shifted from momentum into digestion, consolidating below prior support

Macro took over: tariff fears + JGB stress drove higher rate volatility and risk-off

Open interest compressed hard, confirming deleveraging over spot capitulation

Funding cooled without flipping into an aggressive short regime

Liquidations were contained and mechanical, not cascading

Price stabilized near higher-timeframe support after the leverage reset

ETFs were the headwind: big outflows early, then flat not a real rebound

Cross-asset rotation was defensive: equities softer, yields up, gold/silver surging

On-chain shows rotation, not distribution: STH selling and overhead supply, LTH/whales steady, inflow spikes brief

BTC isn’t in trend mode right now. It’s in consolidation mode and that’s usually where the best positioning gets built.

While price chops, the real tells are elsewhere: macro catalysts lining up, flows getting more informative than candles, and long-term holder activity staying constructive. That mix tends to matter most before the move feels obvious.

That’s why we’ve tightened up our daily + weekly BTC updates around what actually moves the tape: key levels, ETF and on-chain flows, derivatives positioning, and a clean “what changed / what’s next” read.

If you’ve been half-checked-out, this is the easiest way to plug back in without doomscrolling or trying to nail the perfect entry.

If BTC stays range-bound, this is also where grid bots make sense: capture the chop, reduce emotion, let structure do the work.

And if you want to talk it through with other serious traders, jump back into the Circle.

Keep an eye on the Bitcoin Chart Tracker for the key zones, and use the Bitcoin Hub for the deeper flow and holder data.

This is a good window to get positioned early instead of getting convinced late.

See you inside,

The Coiners

Market Update

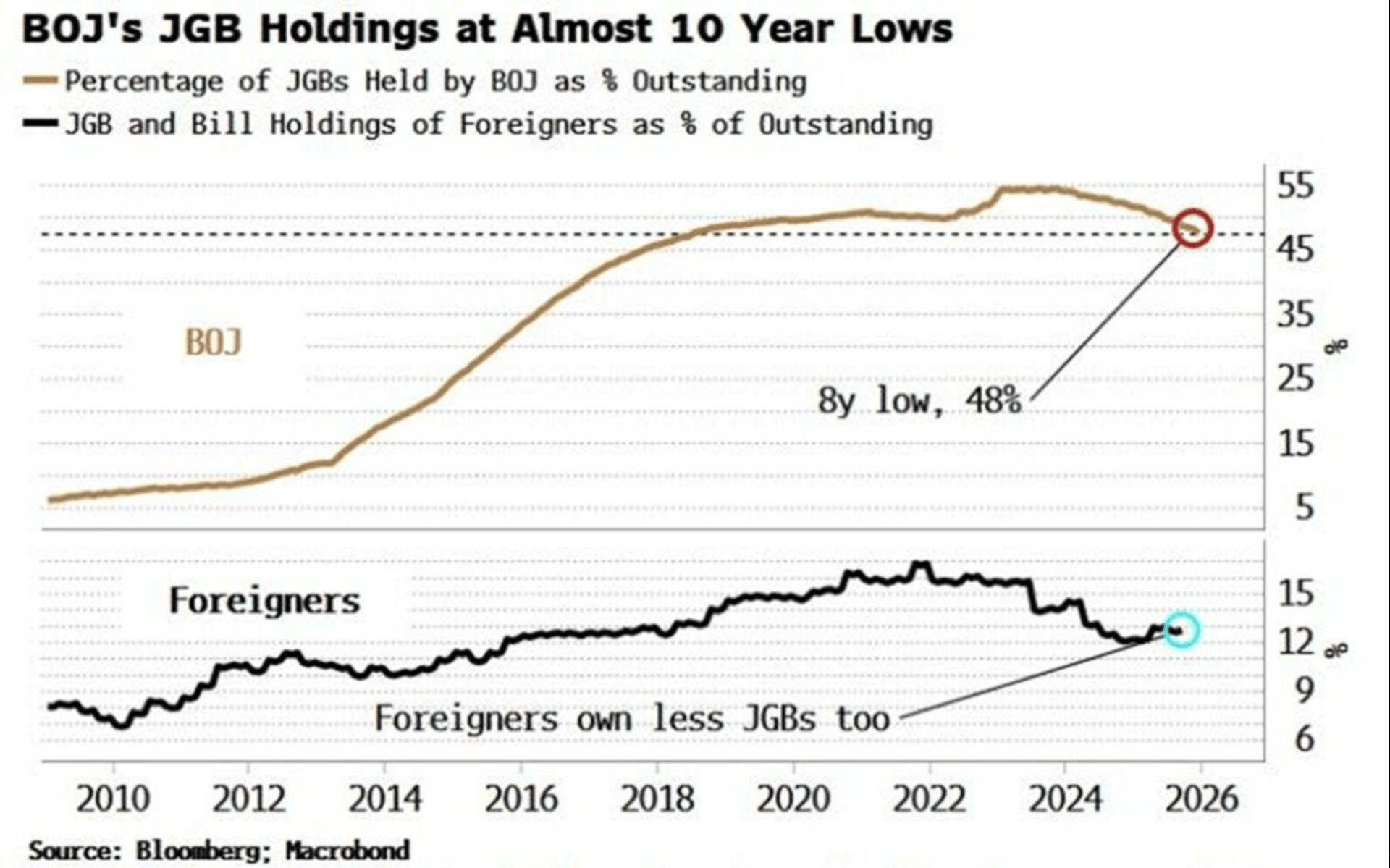

Macro did most of the heavy lifting this week. The risk tone improved early as futures lifted on a better-than-expected US Q4 GDP print, but the market couldn’t hold a clean “growth is fine” narrative because rates kept tightening the frame. US 10Y yields pushed to their highest since August while Japan’s bond market repriced hard, with JGB yields hitting fresh highs as BoJ holdings slid toward 10-year lows. That combination turned each headline into a positioning event.

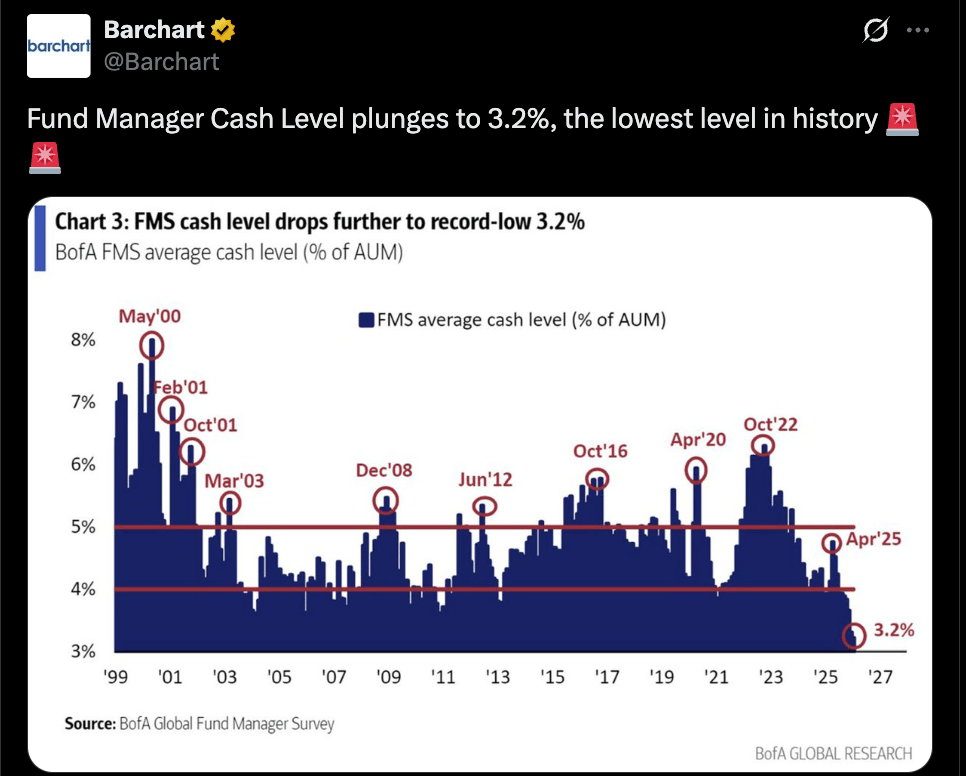

Equities bounced when Trump scrapped EU tariffs, then rolled over as trade-war fears returned alongside the Japan yield jump. Even with US M2 at $22.3T and China flagging a more flexible 2026 GDP target, the clearest tell was how capital behaved: gold, silver, and platinum making new ATHs pointed to hedging and defense, and the slump in pending home sales was a reminder that higher yields still bite. With fund manager cash at the lowest ever, there wasn’t much buffer for volatility.

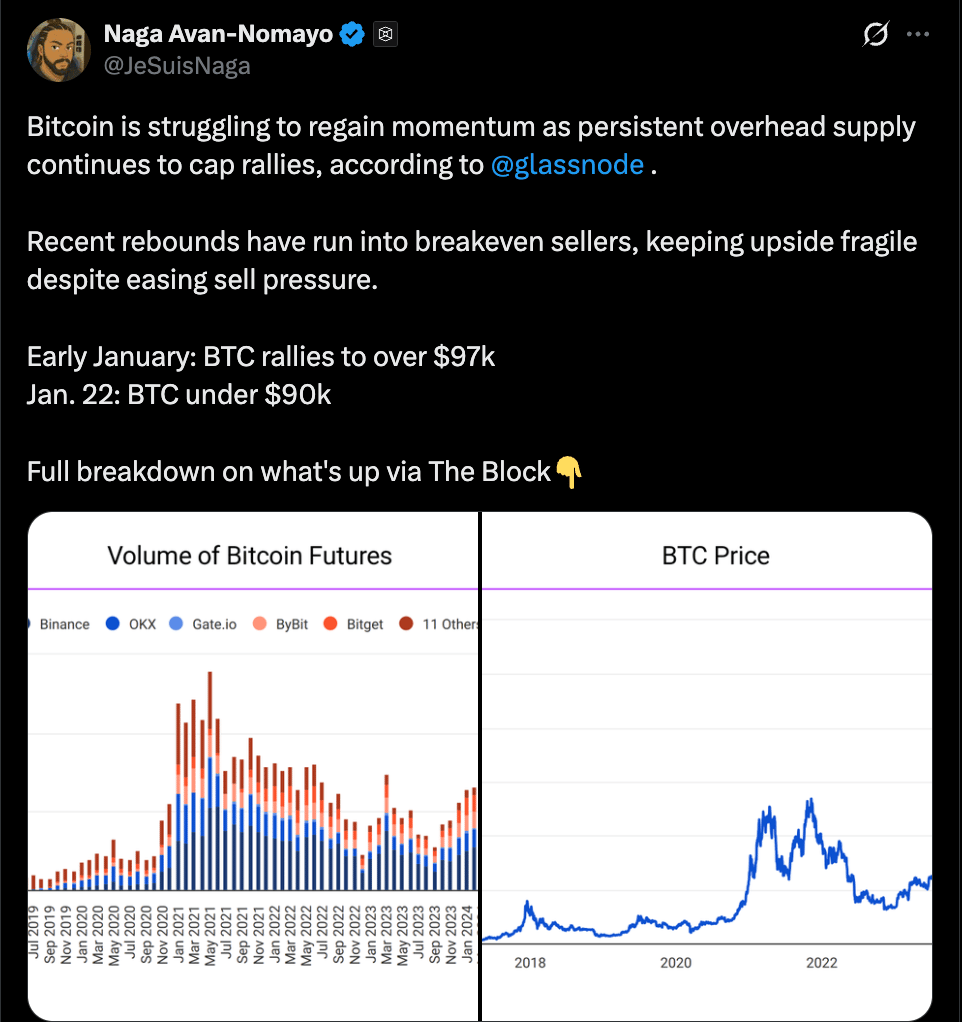

BTC and ETH followed that macro tape. BTC couldn’t turn rallies into momentum, and Glassnode’s point about overhead supply fits with what you see in a headline market: sellers show up quickly into strength and follow-through dries up. ETH was weaker, sliding even when macro looked briefly supportive, and JPMorgan’s view that the recent activity bump may not last added to the cautious read on demand.

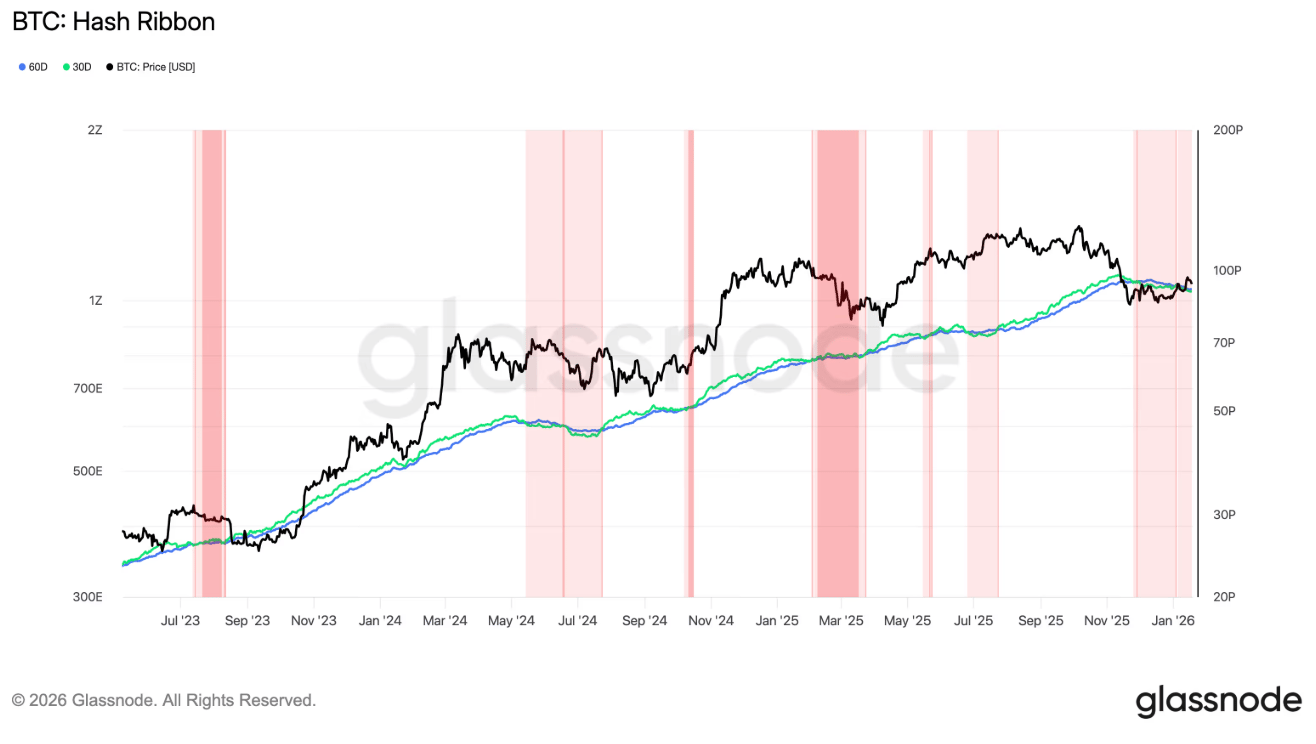

The week also had enough crypto-specific noise to keep people defensive: BTC hashrate fell from October highs, ETH saw a transaction spike tied to address poisoning, and a dormant whale moved $85M of BTC after 13 years. None of that changes the longer-term story on its own, but it does raise the bar for chasing risk while macro is dictating the pace. Elsewhere, leadership was narrow, with RIVER standing out and isolated flows rather than broad risk-on participation.

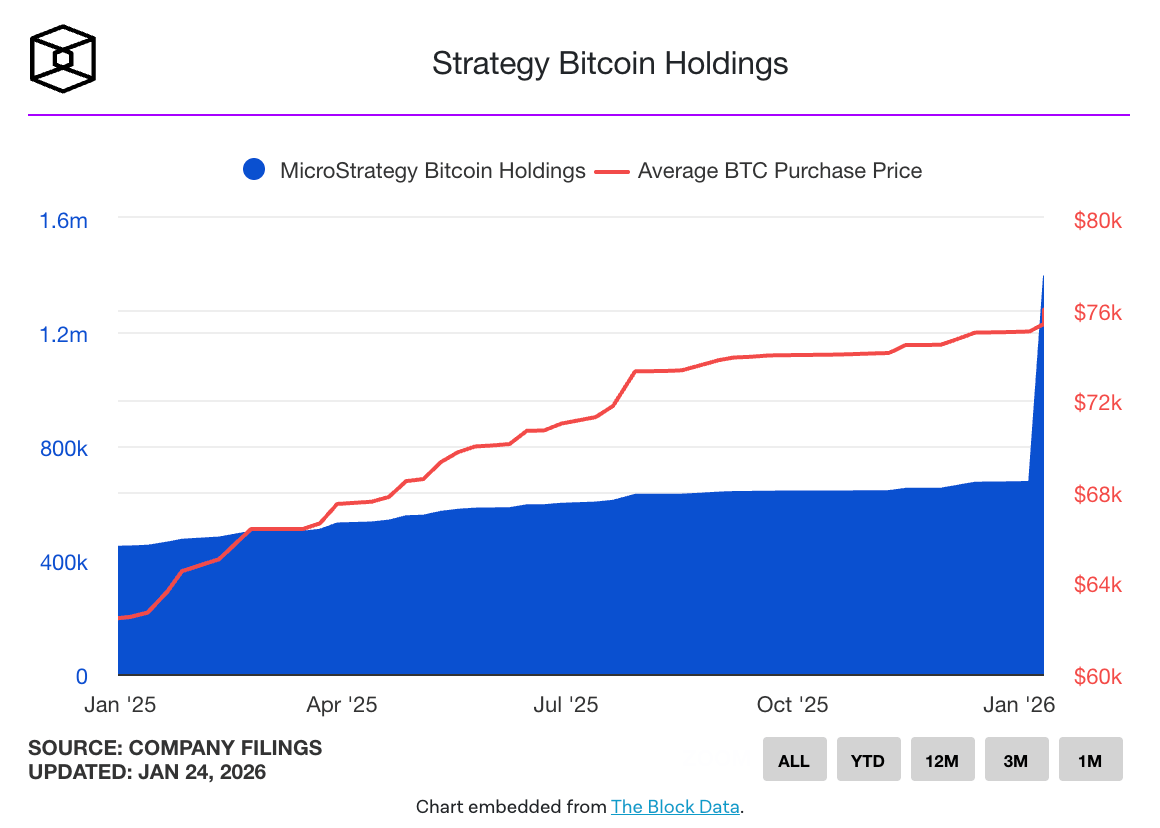

Institutional activity, by contrast, kept pushing forward and was arguably the more important signal than the day-to-day chop. MSTR’s $2.1B BTC purchase, its largest in more than a year, reinforced that the corporate bid is still there. Strive’s plan to raise $150M to buy BTC and retire debt landed in the same bucket: balance sheets are still being positioned around BTC even when the market is stuck in a range.

On the product and capital markets side, GLXY’s plan for a $100M crypto hedge fund and Delaware Life offering an annuity with BTC exposure showed crypto continuing to get wrapped into more traditional vehicles. BitGo’s IPO and Ledger weighing a NY IPO added to the sense that the industry is still moving toward regulated, mainstream funding channels, especially with Revolut preparing to apply for a US banking license.

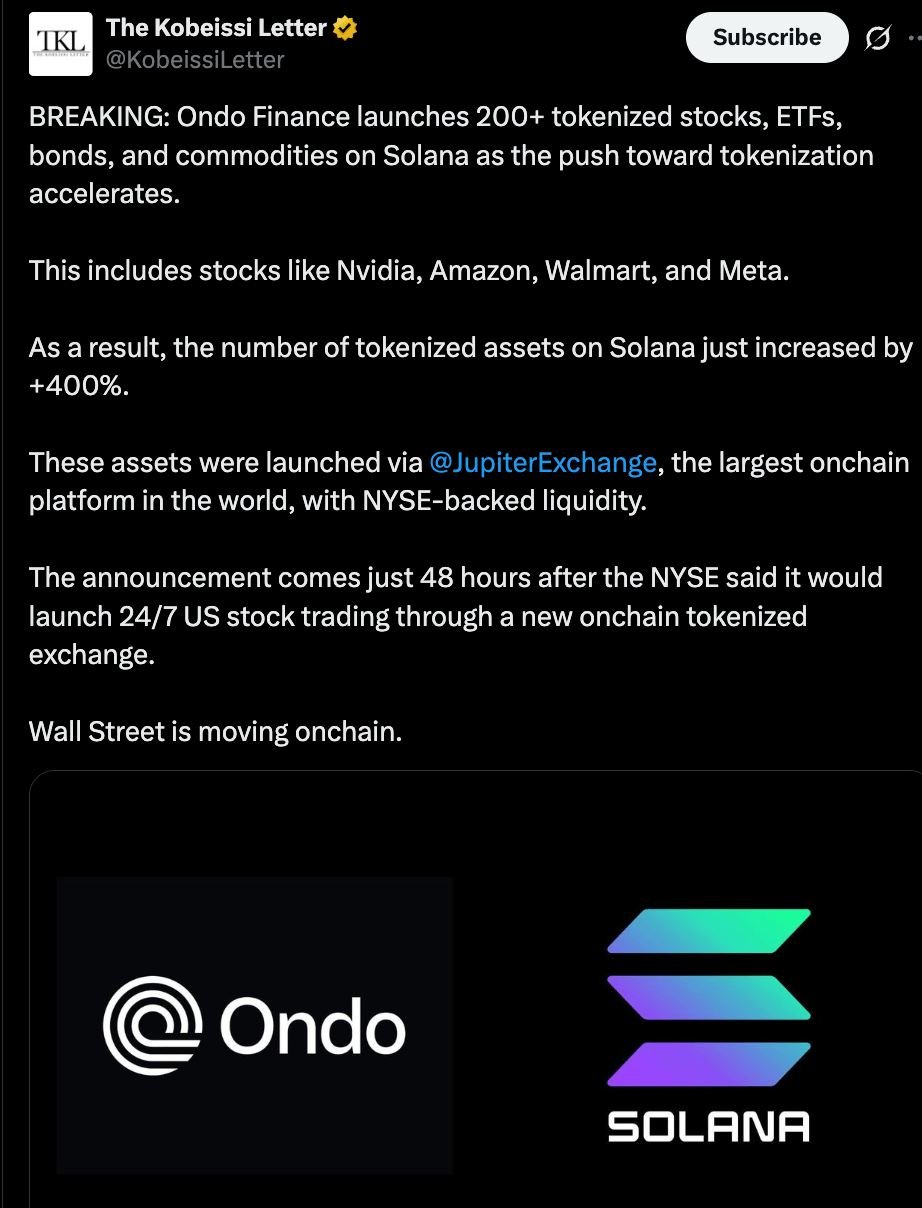

The strongest thematic flow sat in tokenization and market structure. NYSE planning 24/7 tokenized securities trading, SuperState raising $82.5M for RWA tokenization, ONDO launching tokenized stocks on SOL, and LINK rolling out on-chain data for tokenized US stocks all pointed in the same direction, which is why Fink’s call for “one common blockchain” resonated.

Moving on, SAGA paused its EVM chain after a $7M exploit, Makina Finance saw a $5M stablecoin pool exploit, and a pricing glitch at Paradex triggered mass liquidations, all reminders that execution risk remains part of the package. Lastly, regulation moved in parallel, not cleanly but steadily: HK is moving toward stablecoin licensing in Q1, Thailand signaled crypto ETFs and futures, Vietnam opened exchange licensing, and US bill progress continued alongside signs of delay.

Taken together, the setup stayed split: macro volatility is still gating near-term risk, but the institutional and market-structure build continues in the background.

Market Data Points

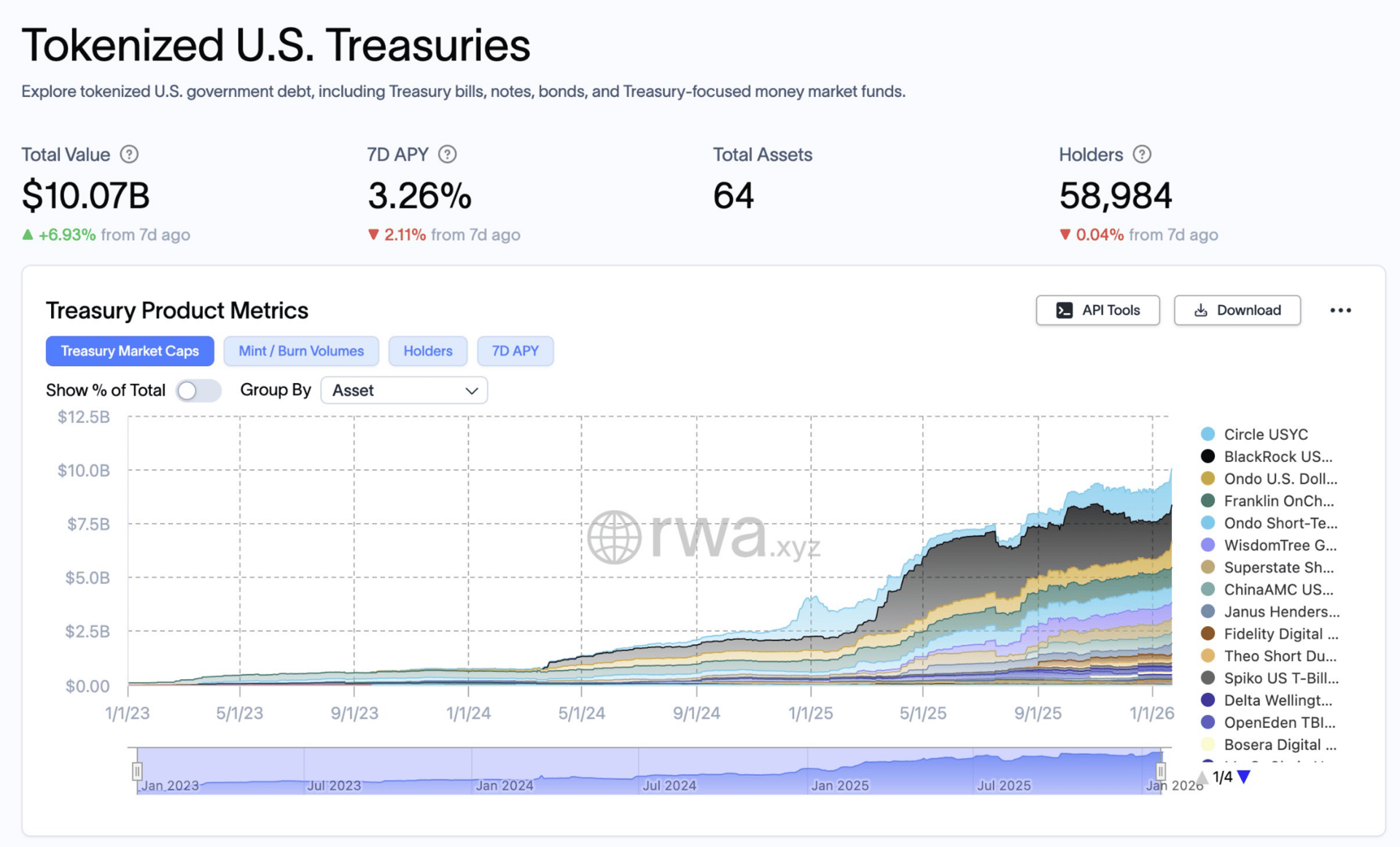

Tokenized Treasuries crossed a meaningful threshold this week, with total value surpassing $10B, highlighting how quickly real-world asset tokenization is moving from pilot phase into scale.

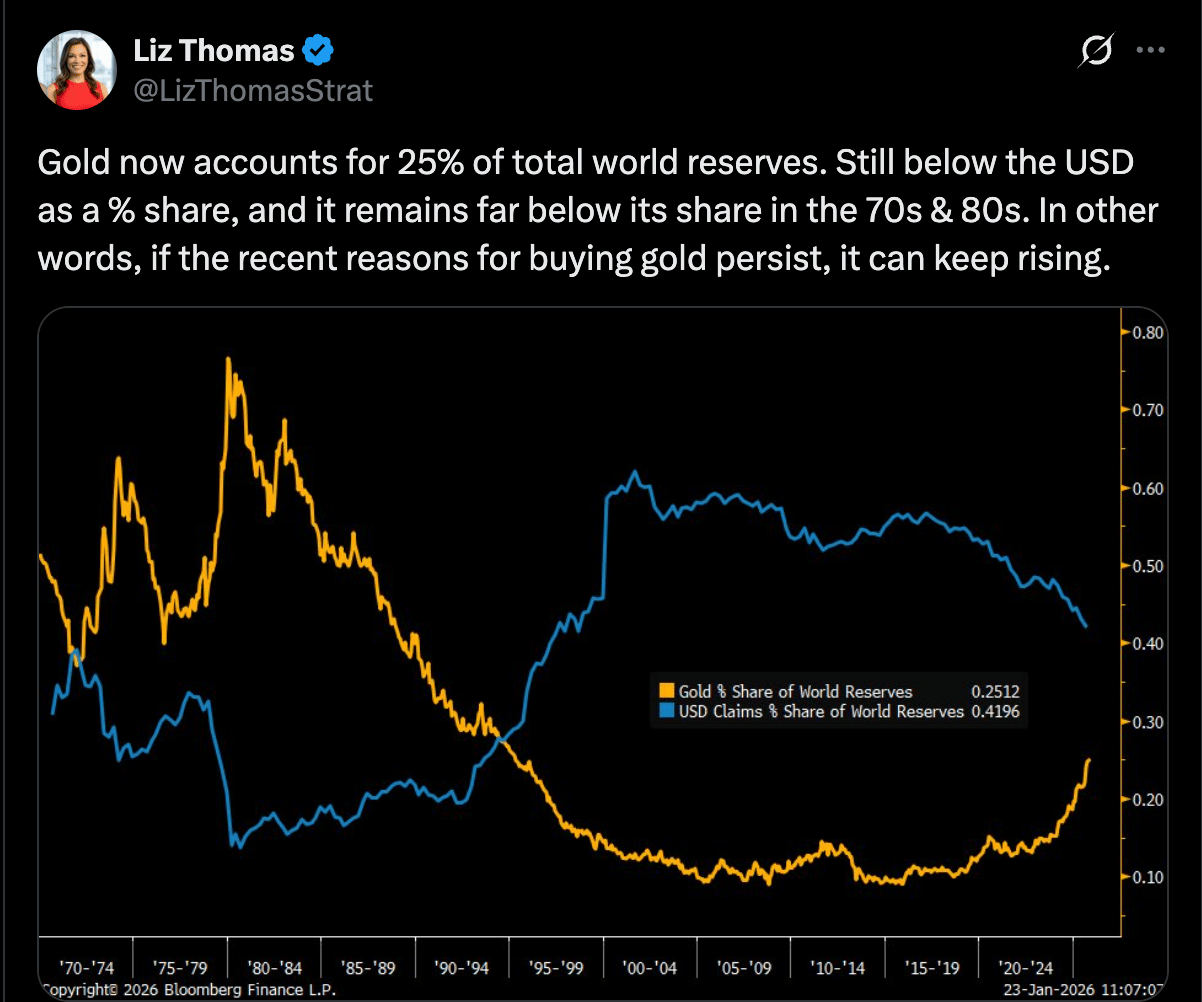

Gold’s role in global reserves continues to expand in a way that reinforces the broader defensive shift underway. It now accounts for roughly 25% of total world reserves, a meaningful increase, yet still sits well below both the USD’s share and gold’s own weighting during the 1970s and 1980s.

That context matters. The recent move is not a sign of saturation, but of catch-up, driven by persistent concerns around currency debasement, geopolitical risk, and reserve diversification. As Liz Thomas points out, if the forces behind current gold accumulation remain in place, there is still room for the trend to extend. The implication for markets is clear: this is less about short-term price momentum and more about a structural reallocation toward hard assets that continues to run alongside tighter financial conditions and elevated policy uncertainty.

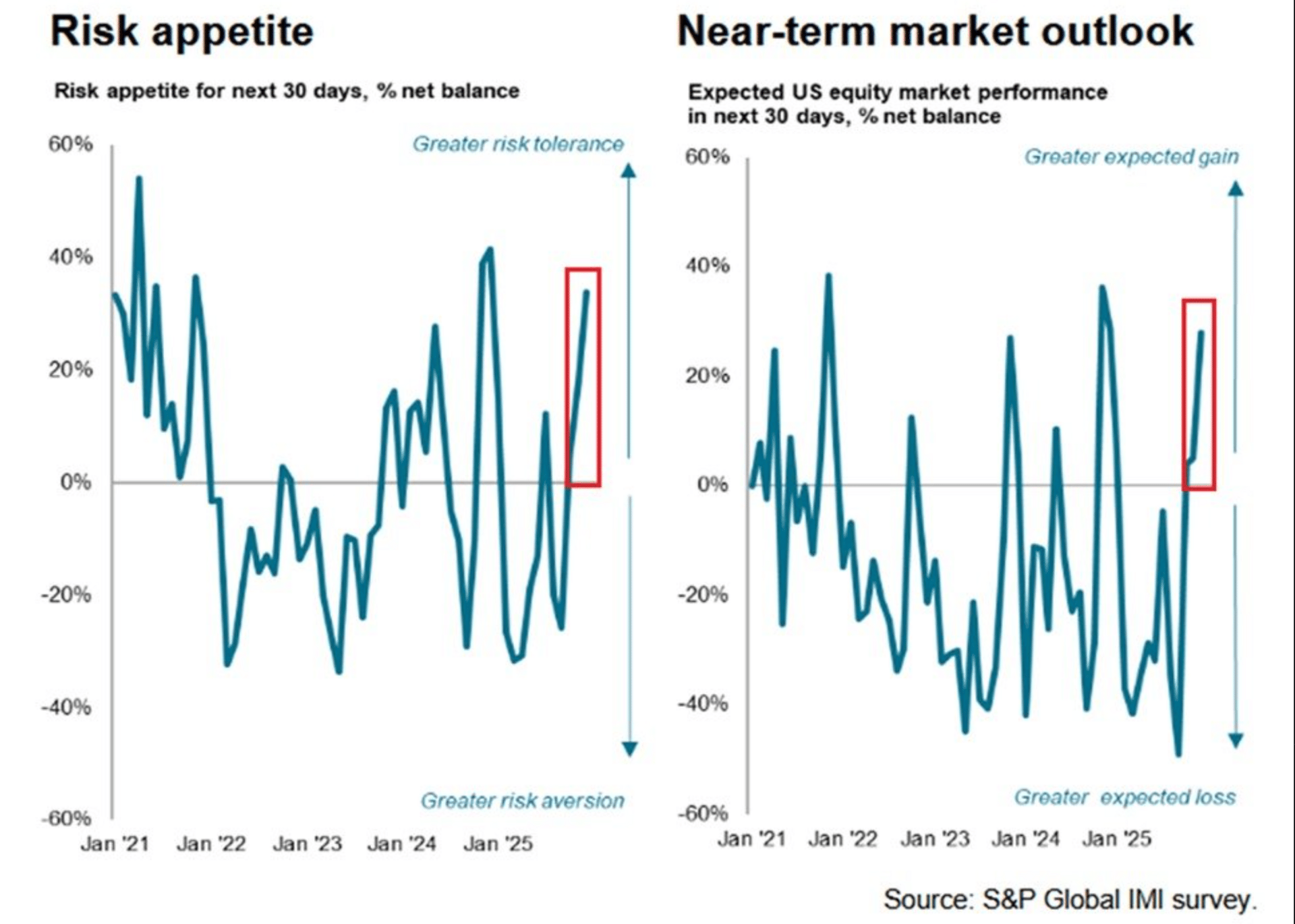

Investor sentiment has swung decisively toward risk, with institutional appetite now sitting near cycle highs. According to The Kobeissi Letter, the S&P Global Investment Manager Index climbed to +41 in January, its strongest reading since April 2021, marking a fourth consecutive monthly increase.

Expectations are similarly lopsided, with a clear majority of fund managers looking for US equity gains over the next 30 days and only a small minority bracing for losses. The signal here isn’t just optimism, but crowding. With risk appetite elevated and near-term outlooks stretched, positioning looks increasingly one-sided, raising the sensitivity of markets to any macro or policy shock that challenges the consensus.

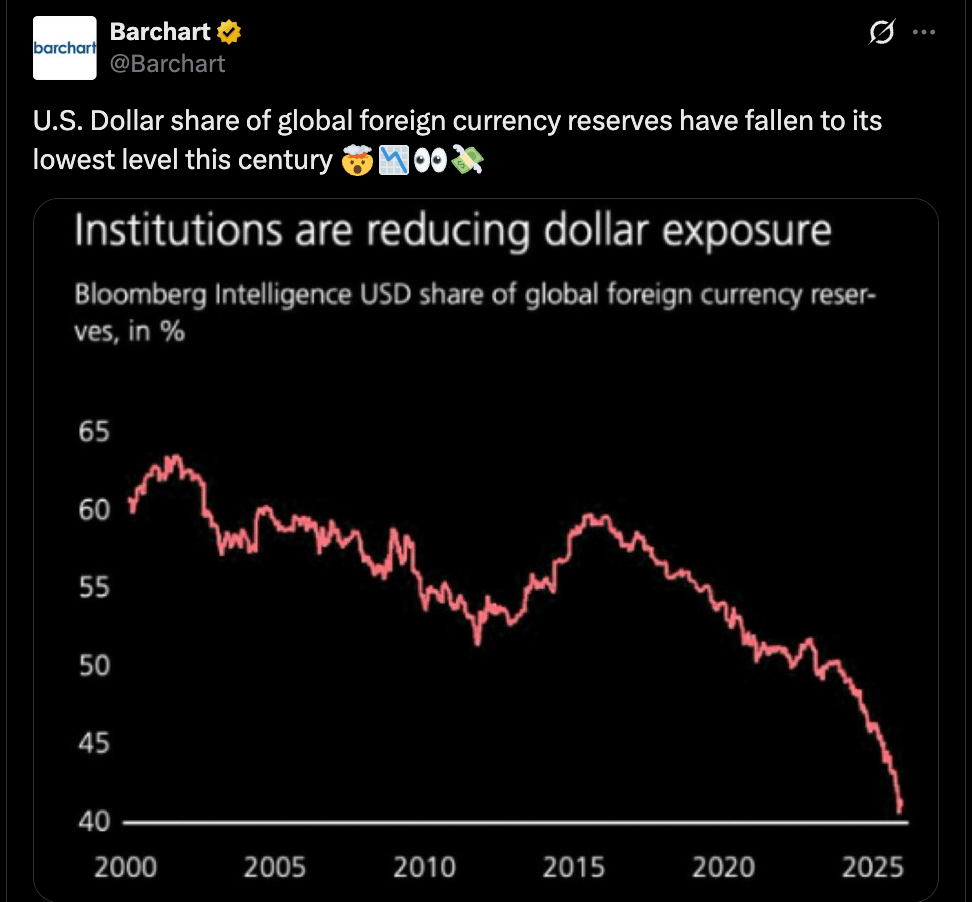

The dollar role in global reserves continues to erode, with its share falling to the lowest level of this century. Institutions have been steadily reducing dollar exposure over the past two decades, a trend that has accelerated more recently.

This isn’t a short-term trade, but a structural reallocation tied to diversification, geopolitical risk, and confidence in alternative reserve assets. In the current context, it helps explain both the persistent bid in gold and the growing interest in non-sovereign or tokenized alternatives, as reserve managers look to spread risk rather than concentrate it in a single currency bloc.

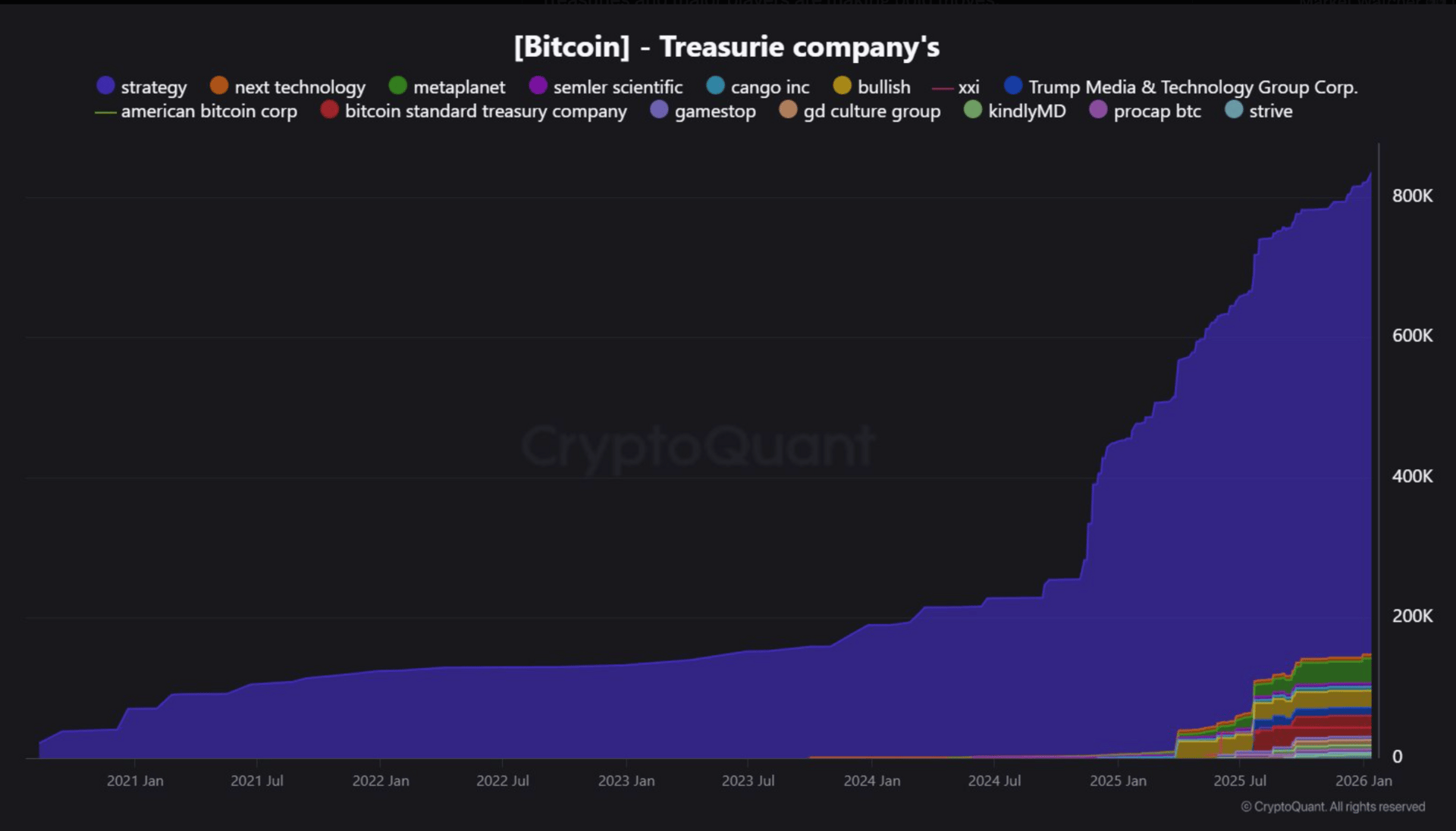

Large-holder and treasury-linked activity picked up this week, with several notable BTC movements that reinforce how much supply is consolidating in strategic hands. The treasury cohort continues to grow its footprint over time, and the recent acceleration reads less like opportunistic trading and more like deliberate balance-sheet positioning.

The takeaway is simple: even when spot is choppy, larger players are still actively managing exposure, which supports medium-term structure while the market works through short-term noise.

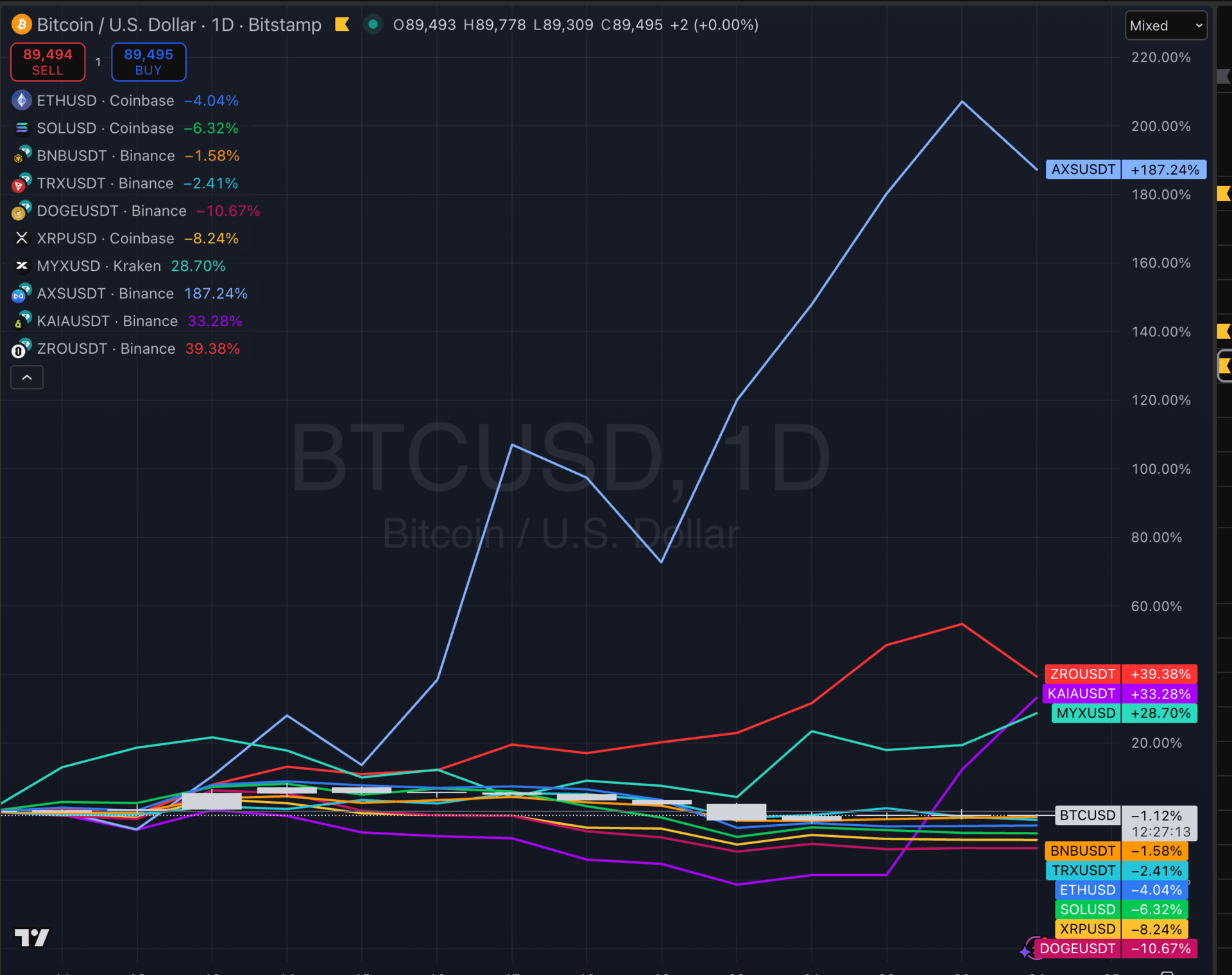

Majors & Memes

Majors ended the week under pressure, with the tone clearly shifting from consolidation into a broader pullback. BTC closed the last seven days lower by mid-single digits, losing momentum after failing to hold recent highs. ETH underperformed on a relative basis, posting a double-digit weekly decline and continuing to lag the broader complex, which kept rotation away from the second-largest asset rather than toward it. BNB and TRX both held up comparatively better but still finished the week lower, while SOL was among the weaker large caps, retracing sharply and giving back more than the rest of the majors. XRP and DOGE also faded over the period, reinforcing a tape where leadership narrowed and downside pressure spread unevenly across the top end of the market.

Outside the majors, upside was highly concentrated and largely idiosyncratic. RIVER was the clear outlier, posting a triple-digit weekly gain and standing well apart from the rest of the field. A second tier of winners followed, led by AXS, KAIA, OG, MYX, and ZRO, all delivering strong multi-week advances that pointed to momentum-driven participation rather than broad-based risk appetite. The common thread among gainers was follow-through in names that were already moving, rather than fresh breakouts across the wider alt universe.

On the downside, losses were broader and more evenly distributed. ENA was among the heaviest laggards, joined by weakness in ARB, SUI, APT, and XMR, all of which saw double-digit weekly declines. Larger thematic names such as NEAR, FIL, WLD, ICP, and PEPE also remained under pressure, while POL, TAO, and CRV extended their drawdowns. In several cases, declines were accompanied by heavy volume, consistent with profit-taking and de-risking rather than simple illiquidity gaps.

The broader read-through is that participation remains limited and highly selective. While a handful of tokens posted outsized gains, most liquid names struggled to hold bids, and the majors failed to provide a stabilizing anchor. Strength showed up in bursts and rotated quickly, while weakness was more persistent across a wide set of recognizable tokens. Until leadership reasserts itself in BTC and relative performance in ETH improves, the market continues to look more like a corrective phase with isolated momentum pockets than the start of a durable, broad-based trend.

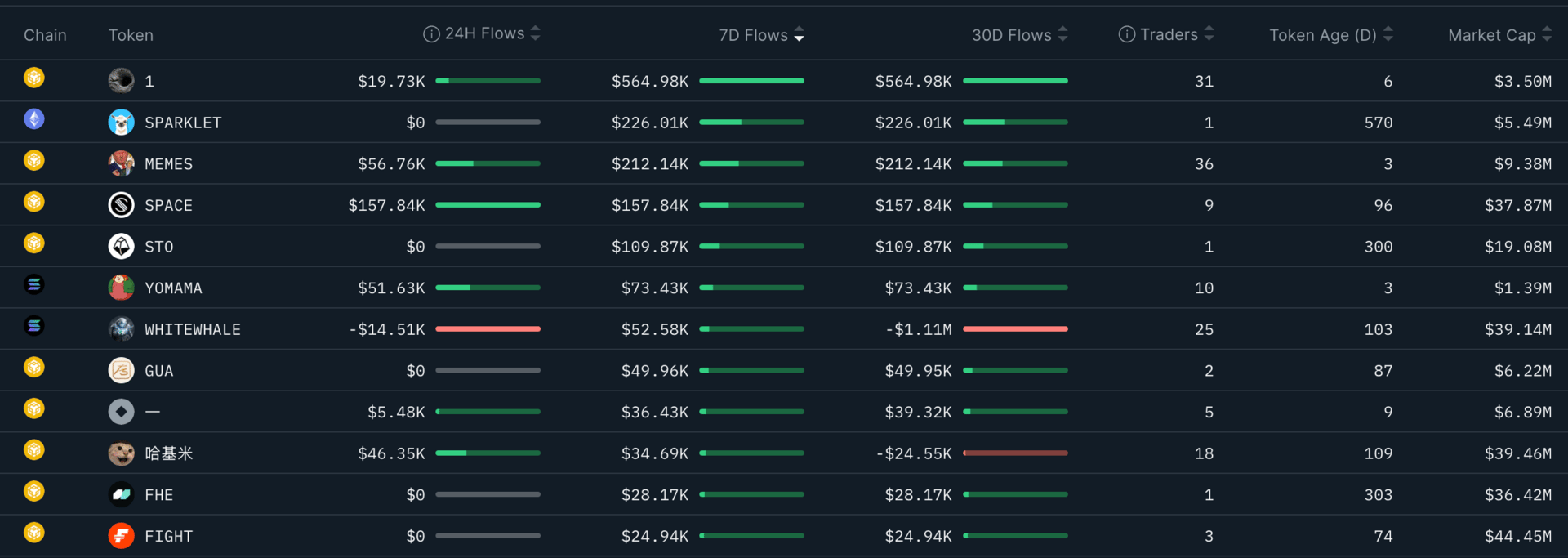

Smart Money Moves

Flows remain muted overall, which is consistent with the current market regime. What activity does show up is concentrated rather than expansive, with capital working selectively instead of rotating broadly across the tape. The cleanest positioning signal is 1, which leads both the 7D and 30D windows (~$565K) while participation stays relatively contained at 31 traders.

That combination, sustained net inflows without a surge in trader count, reads as intentional accumulation rather than momentum chasing. MEMES and SPACE also hold constructive profiles, with positive 24H flow layered on top of positive 7D and 30D balances, suggesting the bid remains present but controlled.

The concentration of flows is the more important signal than the absolute size. SPARKLET and STO show meaningful 7D and 30D inflows ($226K and $110K) with just one trader involved, pointing to single-wallet positioning rather than participation-led moves. FHE and FIGHT show a similar pattern at smaller scale, reinforcing the view that positioning is being built quietly in thinner liquidity rather than chased in size.

Where the longer window diverges, the message is different. WHITEWHALE shows a small positive 7D flow against a deeply negative 30D balance (-$1.1M), which looks more like short-term stabilization within a broader unwind than fresh accumulation. 哈基米 also shows recent inflows after a negative 30D trend, fitting rotation or speculative re-entry rather than sustained building. Overall, the picture fits the regime: limited risk appetite, muted flows, and selective accumulation where 7D and 30D trends align and participation remains tight.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply