- Crypto Pragmatist by M6 Labs

- Posts

- Macro Stays in Control, Sentiment Breaks

Macro Stays in Control, Sentiment Breaks

Commodities Whipsaw, Warsh Named Fed Chair, Crypto Sells Off

The Coiners

January 31, 2026

GM Anon!

Macro has been in control for some time, and this week pushed that reality to the forefront. Commodities surged to extremes before snapping back sharply, while policy uncertainty intensified following Trump’s decision to appoint Kevin Warsh as the next Fed chair, a move the market views as more restrictive.

Crypto absorbed the shock poorly. Prices sold off decisively, sentiment turned deeply bearish, and concern shifted toward whether the move marks further downside rather than simple consolidation. The pressure looks macro-driven rather than idiosyncratic, but the damage has been real, and risk appetite remains thin. For now, markets are trading defense first, with stabilization still unproven. Let’s dig in.

TLDR

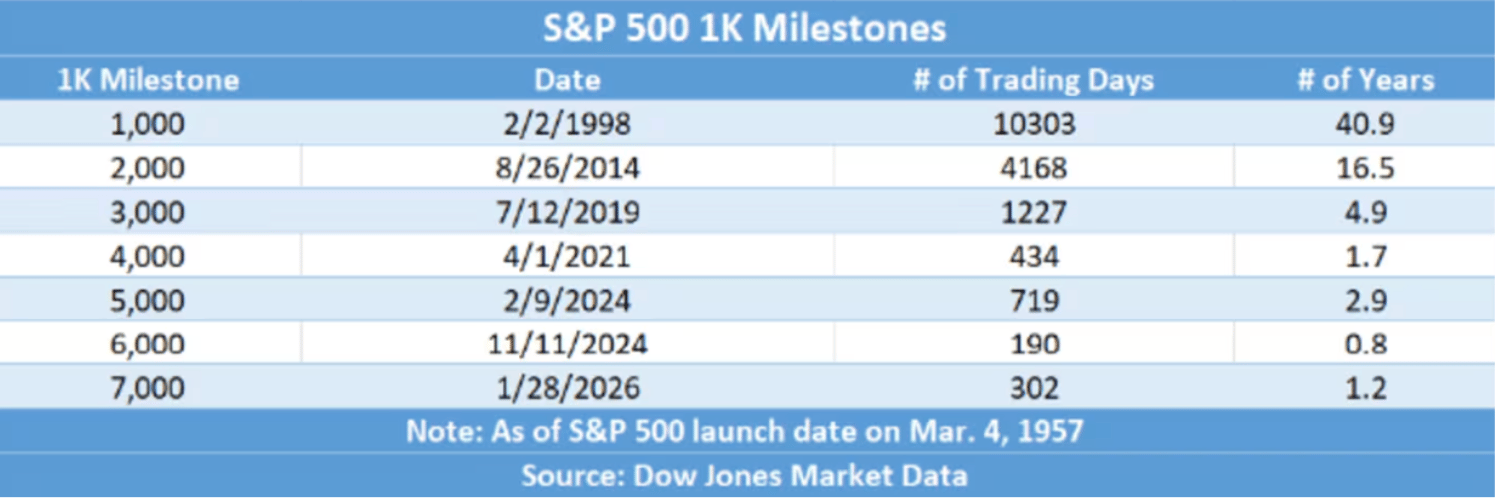

Macro was volatile, with shutdown risk and a rate hold clashing with the S&P 500 hitting 7,000.

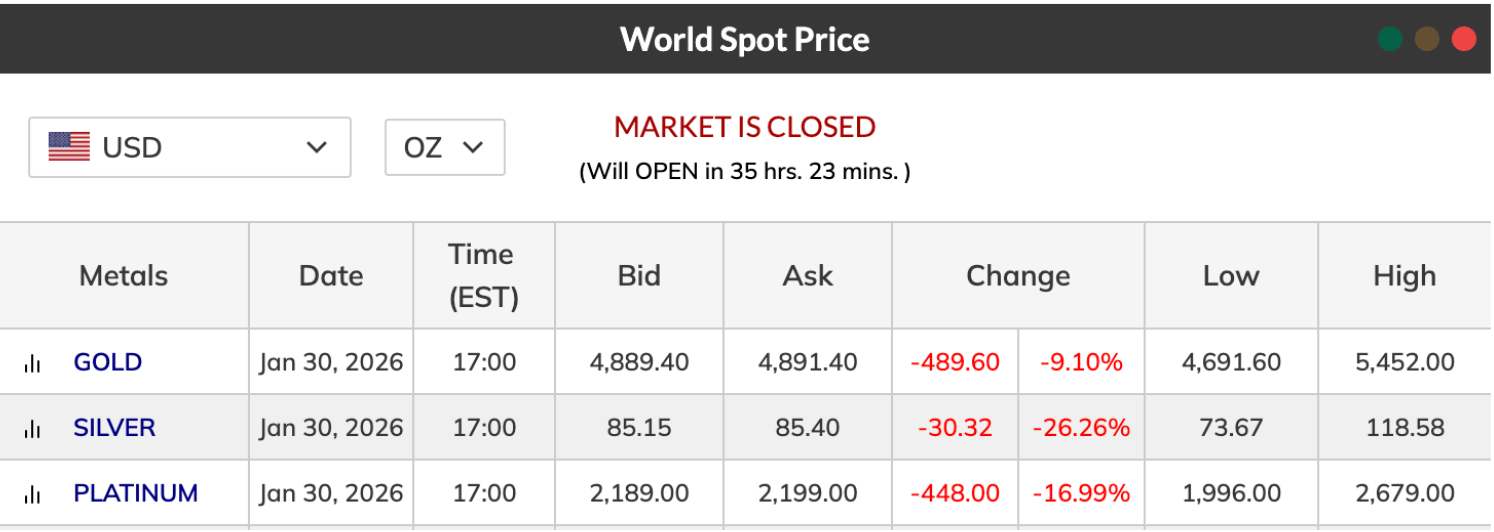

Commodities led risk appetite as gold hit $5.5K and silver $120 before sharp reversals.

Crypto traded as a funding source, selling off around the Fed and staying mixed as metals dominated.

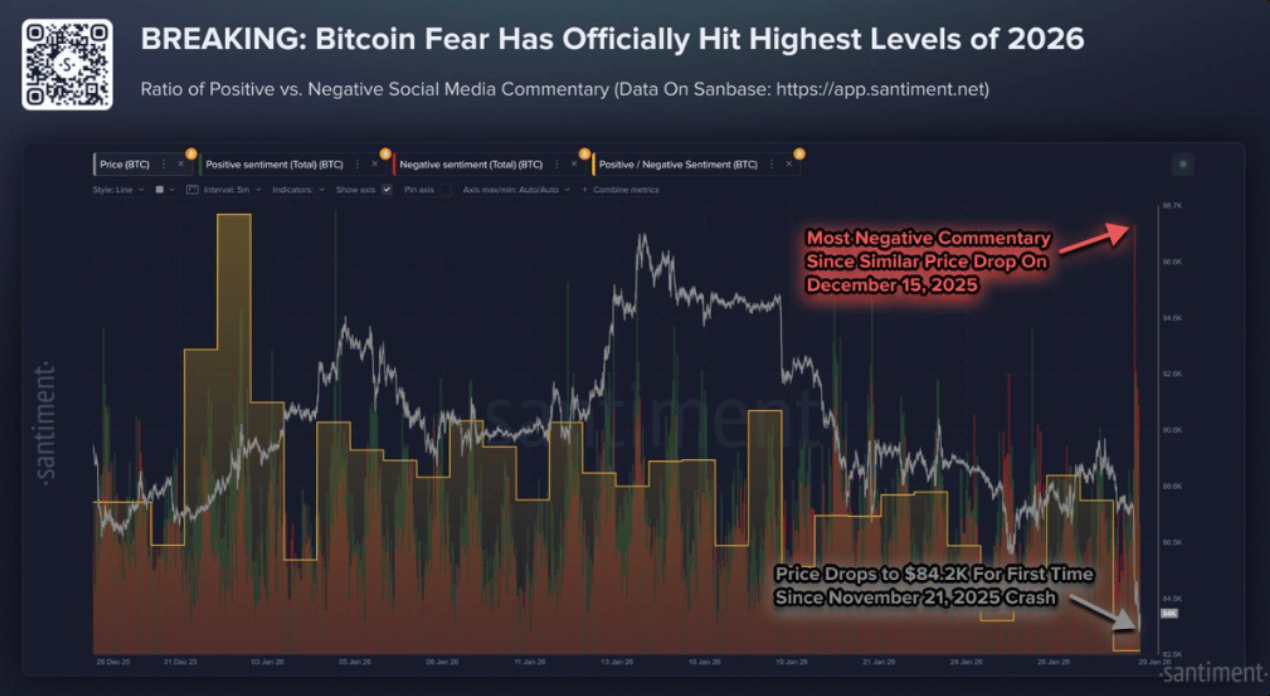

BTC sentiment deteriorated sharply, pointing to late-stage correction dynamics and choppy price action.

Structural macro stress persists, with weaker US consumer savings and pressure on bank balance sheets.

Crypto majors had a weak week, led lower by ETH and SOL, with no broad inflow signal.

Altcoin performance was narrow, with HYPE leading gains while most names continued to unwind.

Institutional activity focused on long-term positioning rather than risk expansion.

Regulation and market structure advanced in prediction markets, tokenization, and stablecoins.

BTC isn’t in trend mode right now. It’s in consolidation mode and that’s usually where the best positioning gets built.

While price chops, the real tells are elsewhere: macro catalysts lining up, flows getting more informative than candles, and long-term holder activity staying constructive. That mix tends to matter most before the move feels obvious.

That’s why we’ve tightened up our daily + weekly BTC updates around what actually moves the tape: key levels, ETF and on-chain flows, derivatives positioning, and a clean “what changed / what’s next” read.

If you’ve been half-checked-out, this is the easiest way to plug back in without doomscrolling or trying to nail the perfect entry.

If BTC stays range-bound, this is also where grid bots make sense: capture the chop, reduce emotion, let structure do the work.

And if you want to talk it through with other serious traders, jump back into the Circle.

Keep an eye on the Bitcoin Chart Tracker for the key zones, and use the Bitcoin Hub for the deeper flow and holder data.

This is a good window to get positioned early instead of getting convinced late.

See you inside,

The Coiners

Market Update

Macro conditions were volatile and contradictory. US equity futures slipped after a vote to avoid a government shutdown failed, yet the S&P 500 pushed to 7,000 for the first time, highlighting the growing disconnect between headline risk and equity price strength. The FOMC left rates unchanged in a split decision, while the policy backdrop shifted again with Trump announcing Warsh as the next Fed chair.

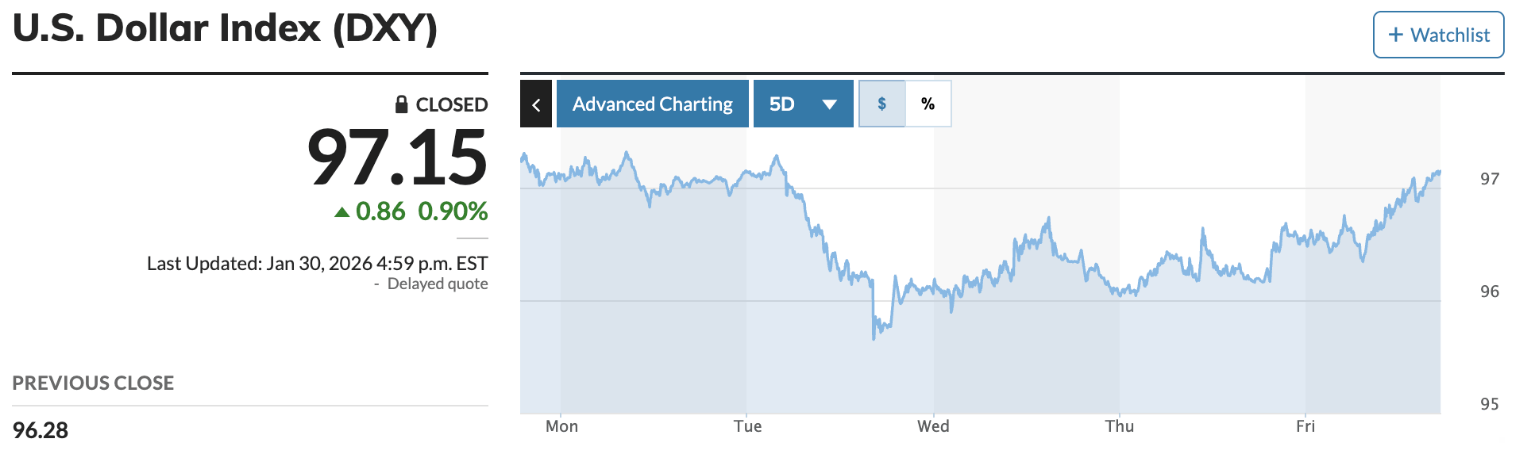

FX markets added noise as reports suggested BoJ intervention in JPY. Commodities remained the clear leadership trade: gold surged to $5.5K and silver to $120 before both reversed sharply in violent swings, uranium went parabolic, and aluminum reached a four-year high. Against this backdrop, crypto traded as a source of liquidity rather than a destination, repeatedly framed as dumping or mixed while metals continued to command attention.

Crypto price action largely reflected that macro dominance. Headlines pointed to crypto selling off after the Fed decision and again as metals whipsawed, with only brief stabilization when the dollar weakened. Activity was highly concentrated rather than broad-based. HYPE stood out, rising 25% as HIP-3 open interest hit $790M, then accelerating 50% in two days as volume surged.

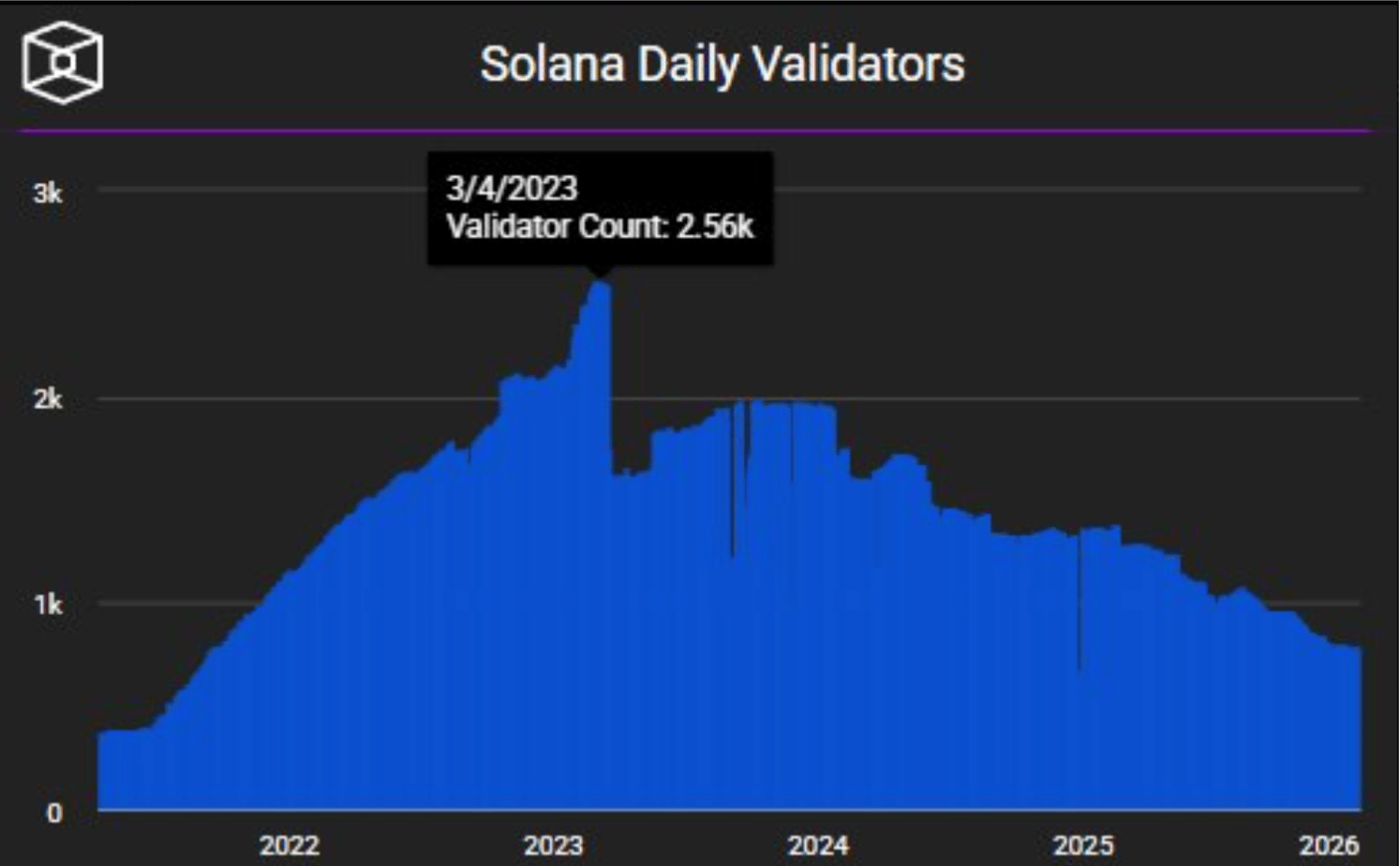

Meme activity was cited as doubling in daily active addresses, driving sharp but fragile moves, including CopperInu reaching $15M and CLAWD collapsing 90% following a bot name change. Structural stress also surfaced beneath the surface, with SOL validator count down 65% versus 2023 and BTC mining hashrate crashing due to Storm Fernan.

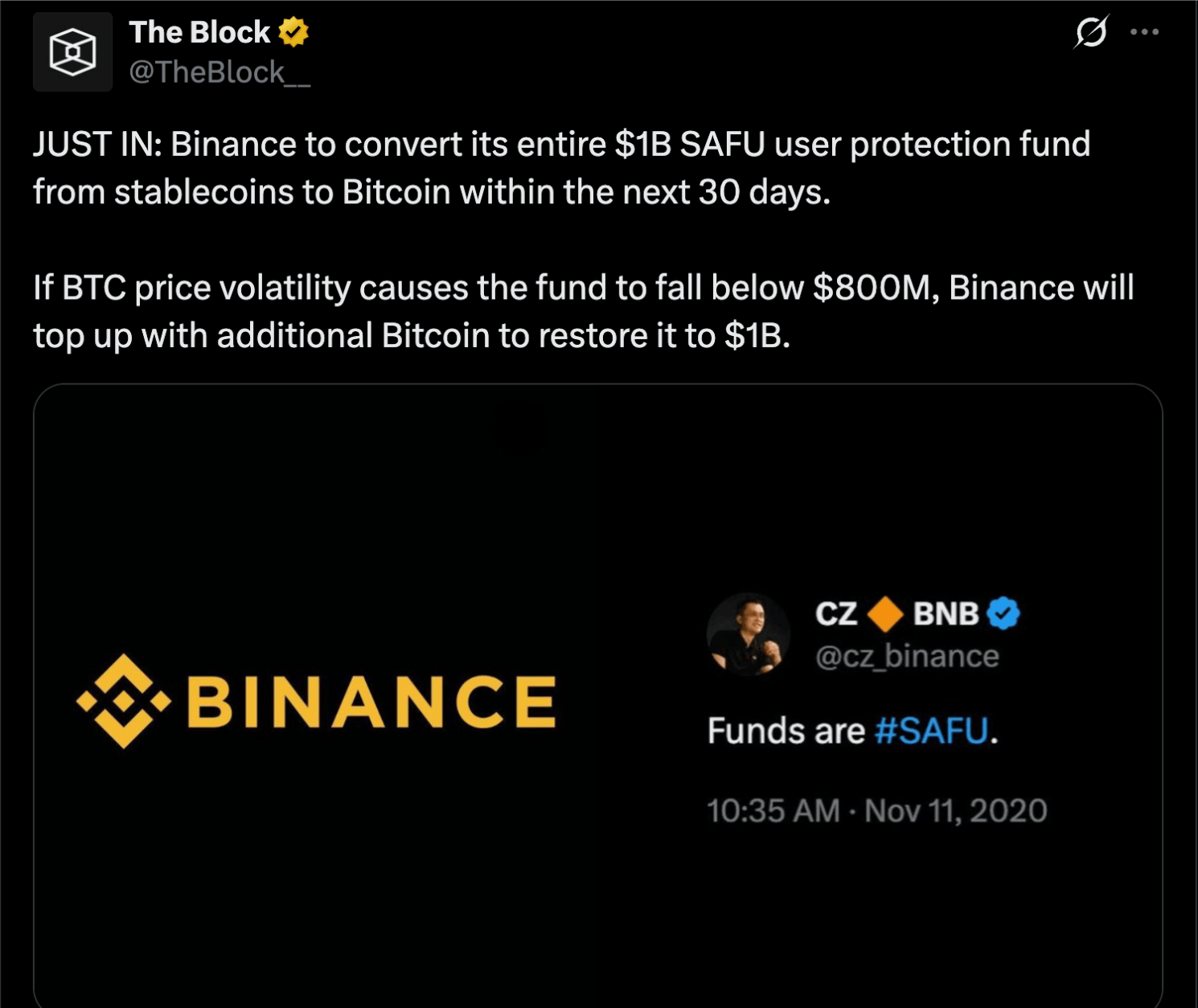

Institutional and infrastructure headlines leaned toward long-term positioning rather than short-term risk appetite. Strategy bought $264M of BTC while BMNR added $117M of ETH, and Metaplanet announced plans to raise $137M in equity to buy BTC. Binance pledged a $1B fund tied to BTC, while Kazakhstan moved to bolster reserves with seized BTC.

At the same time, notable flows highlighted ongoing repositioning, with $397M of ETH moved to Gemini and another dormant wallet shifting $145M. On the resilience side, BTC quantum risk was described as manageable, ETH developers moved hack funds into a new security fund, the ETH Foundation entered a period of mild austerity, and a post-quantum security team was formed alongside work on FOCIL and the upcoming MegaETH mainnet launch.

Product expansion and regulation continued to advance in parallel. COIN launched prediction markets nationwide via Kalshi, while Polymarket tracked toward an ATH $3B in monthly volume and signed an exclusive MLS licensing deal, even as the CFTC signaled new rules for prediction markets and Kalshi opened a DC office.

Tokenization momentum broadened with HOOD planning 24/7 tokenized stock trading, OKX and Binance considering tokenized stocks, and the Hang Seng debuting a tokenized gold ETF, echoed by new yield-bearing tokenized gold for DeFi.

Stablecoin narratives accelerated with Fidelity planning FIDD, Tether launching USAT in the US, and Tether described as the largest gold holder outside nations and banks, alongside a StanChart projection of $500B moving from banks to stablecoins by 2028, even as US banks were reported to block or delay 40% of crypto payments.

Regulatory momentum remained active but uneven, with the SEC and CFTC launching Project Crypto, the Senate Ag committee advancing on crypto only to delay hearings and face an ethics amendment, the White House pushing legislation forward, and the SEC clarifying tokenized securities rules while moving to dismiss the Gemini Earn lawsuit with prejudice. Internationally, Russia signaled a crypto framework rollout in July while banning WhiteBIT, Japan sought public input on stablecoin collateral and floated crypto ETFs in 2028, and South Korea moved to allow investment in overseas crypto.

Market Data Points

BTC sentiment has deteriorated sharply. Historically, spikes in fear of this magnitude have tended to emerge late in corrective phases rather than at the start, often coinciding with retail capitulation and elevated volatility. For now, sentiment remains fragile and price action is likely to stay choppy, particularly as broader risk markets and commodities continue to digest recent pullbacks. While extreme fear can eventually set the stage for stabilization, the near-term environment still favors caution over conviction.

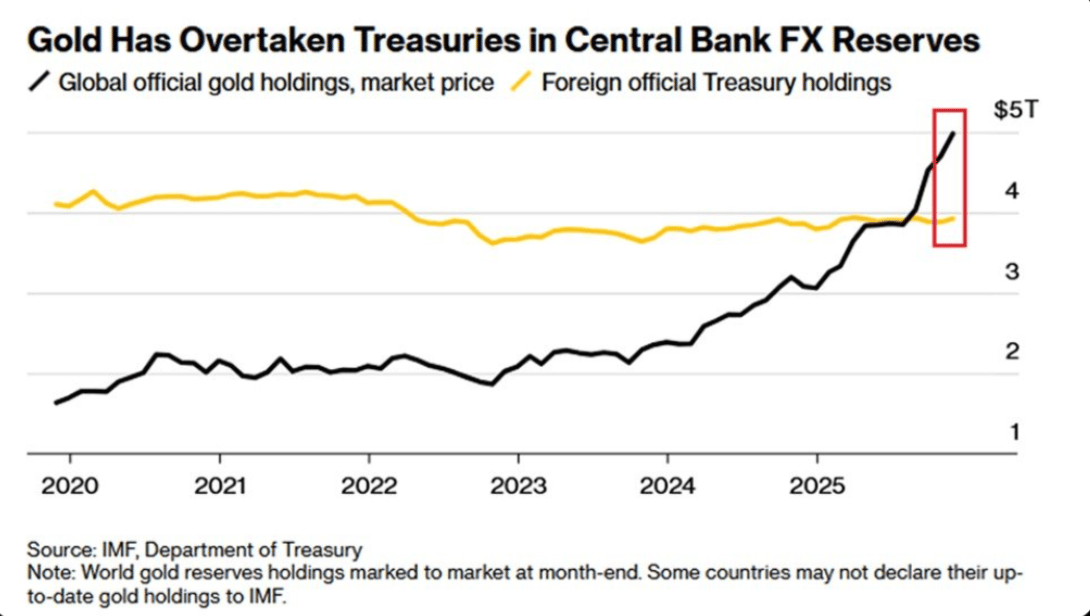

Gold continues to attract sustained institutional demand, with central bank holdings now exceeding foreign holdings of US Treasuries in global FX reserves for the first time in over two decades. Official gold reserves have risen sharply since 2019, driven by consistent central bank accumulation alongside higher prices, while Treasury holdings have remained broadly flat.

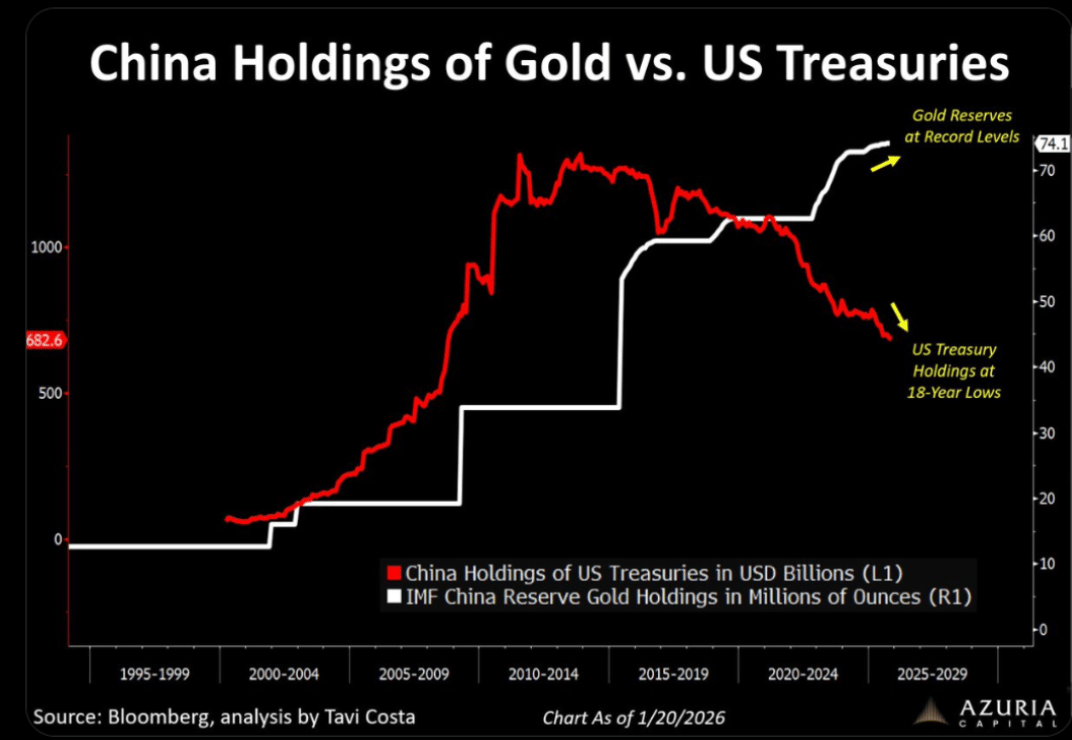

China continues to accelerate its shift away from dollar-denominated assets, reducing its holdings of US Treasuries while steadily increasing gold reserves. Gold holdings have reached a record high, more than doubling over the past decade, while Treasury exposure has fallen to the lowest level in nearly two decades. The divergence highlights an intentional diversification strategy toward hard assets and away from traditional reserve instruments.

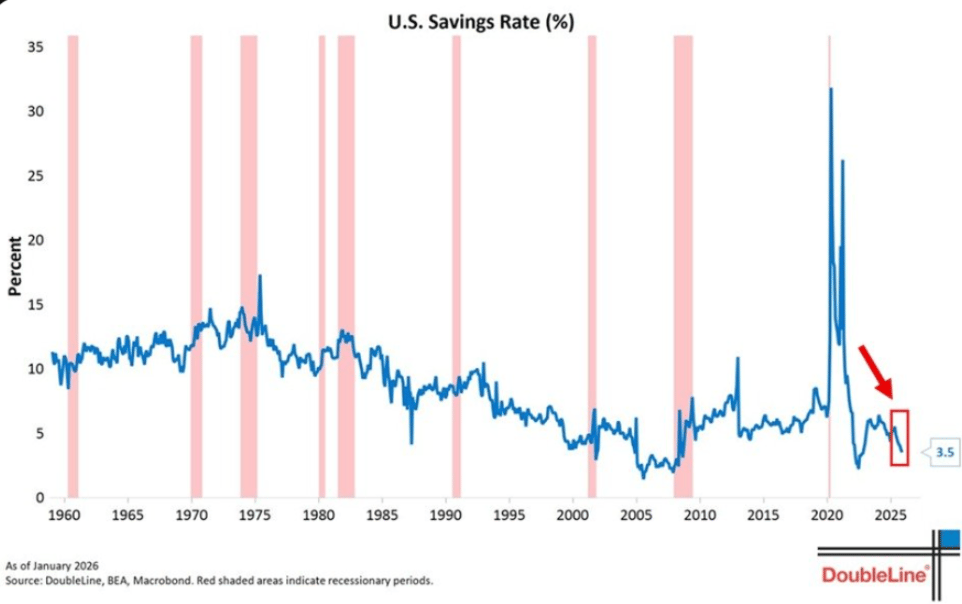

US consumer savings continue to deteriorate, with the personal savings rate falling to 3.5%, the lowest level since late 2022 and among the weakest readings outside crisis periods. Savings have declined sharply over the past year, with pandemic-era excess buffers now fully depleted and aggregate savings levels down nearly 40% from recent highs. The drawdown highlights growing pressure on household balance sheets and suggests reduced capacity for discretionary spending or risk-taking.

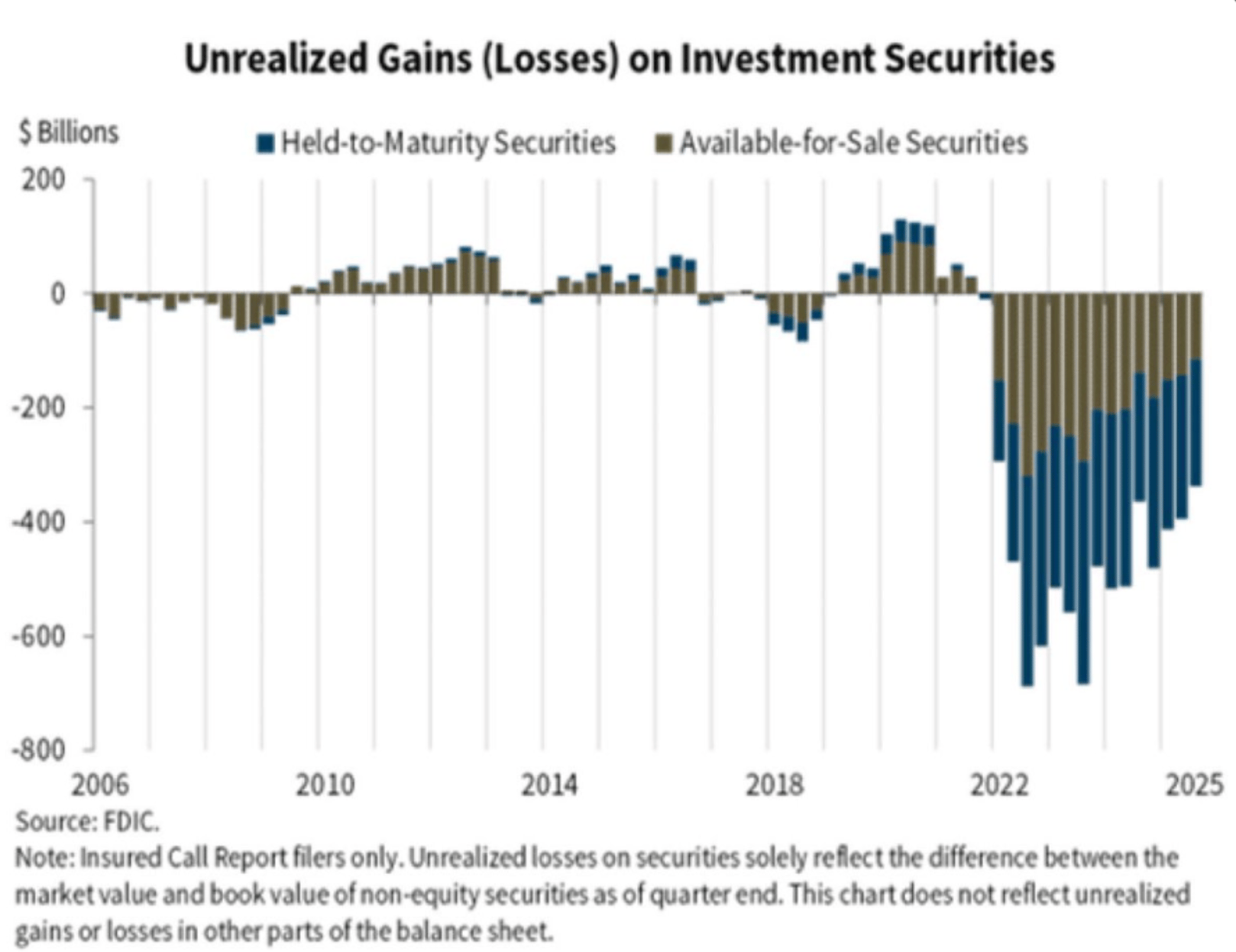

US banks continue to carry a sizable mark-to-market overhang, with unrealized losses on investment securities totaling roughly $337B. While these losses remain unrealized and concentrated in held-to-maturity portfolios, they reflect the lasting impact of higher interest rates on bank balance sheets. The persistence of these losses limits balance sheet flexibility and keeps pressure on lending conditions, even without immediate stress.

Majors & Memes

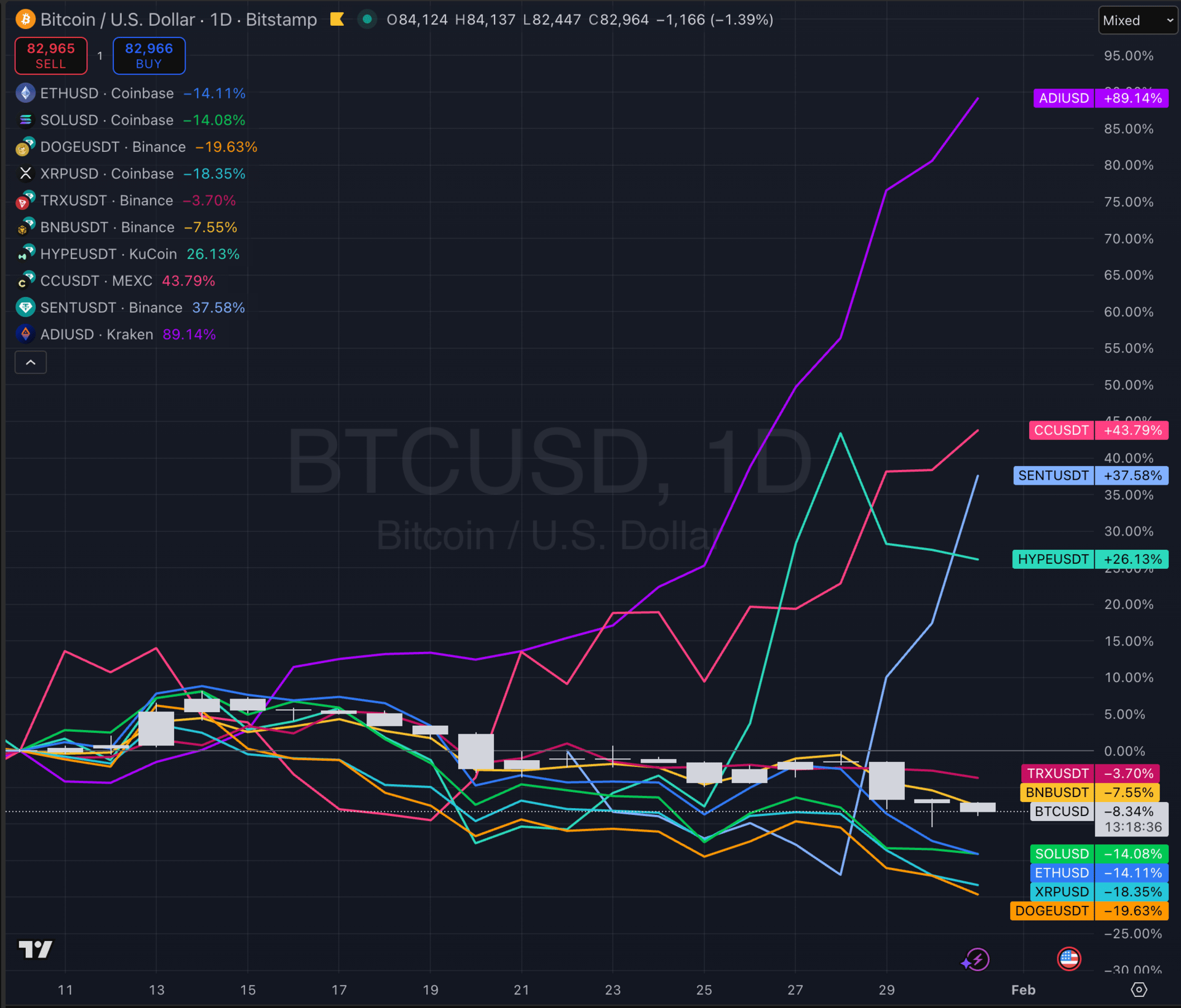

It was a difficult week for crypto, with price action reflecting risk aversion and a clear absence of fresh capital entering the space. BTC fell about 7.4% over the past seven days, while ETH underperformed again, down roughly 10.6% on the week, reinforcing a softer ETH/BTC dynamic as higher beta exposure remained out of favor. BNB was relatively resilient with a 6.1% decline, while SOL dropped around 8.4% after failing to hold upside momentum. XRP and DOGE both slid more than 10% on the week, while TRX stood out defensively, down just 2.2%.

Outside the majors, performance was uneven and highly selective. A small number of tokens posted strong weekly gains, led by HYPE, which rose nearly 30% on heavy volume. CC advanced about 24%, while SENT and ADI delivered outsized gains of roughly 40% and nearly 60% respectively. These moves appeared isolated and momentum-driven rather than indicative of a broader shift in sentiment.

Weakness, however, was far more widespread. SUI fell approximately 17.7%, ICP dropped about 17.0%, and ARB declined close to 15%, reflecting continued distribution and fading upside interest. Deeper drawdowns were visible further down the market, with AXS, DASH, SAND, and MANA posting weekly losses in the 25% to 30% range, highlighting how quickly speculative excess has been unwound.

Overall, the weekly tape points to a market still under pressure, with no clear signs of rotation or capital flowing back into crypto. Interest and enthusiasm continue to favor commodities, leaving digital assets in a defensive, consolidative posture. Until broader risk sentiment improves and leadership expands beyond a few isolated outperformers, crypto is likely to remain choppy and selective rather than trending decisively higher.

Smart Money Moves

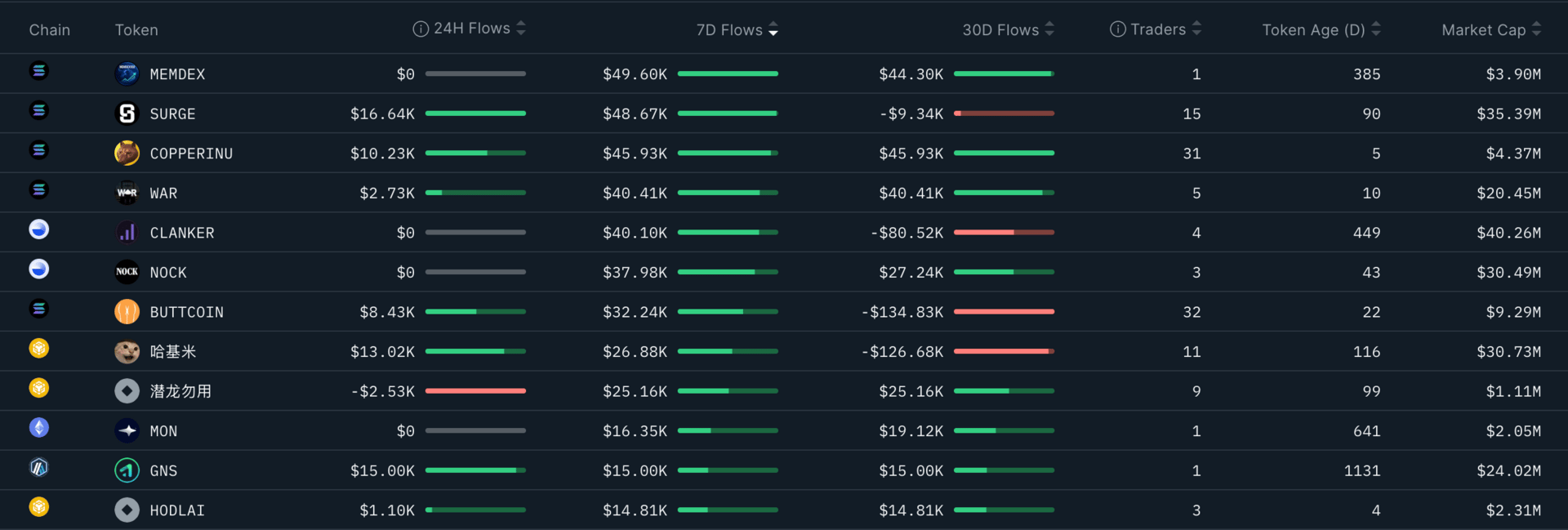

Flows remain constrained, but that has been the operating condition for months and is now the baseline rather than a signal. What matters in this environment is where capital continues to show up despite those limits, how much is being committed over the 30 day window, and whether participation reflects isolated positioning or shared conviction.

The more constructive profiles are those where weekly inflows are reinforcing an already positive longer term balance. MEMDEX shows roughly $49.6K of 7 day inflow sitting on top of a positive $44.3K over 30 days, with activity coming from a single wallet. The concentration keeps the footprint narrow, but the alignment across windows suggests the position is being maintained rather than flipped.

COPPERINU stands out more on participation. About $45.9K of 7 day accumulation aligns spread across 31 wallets. In a restricted flow regime, that breadth matters. It points to confidence being shared rather than sponsored by one actor, which tends to make the trend more durable. WAR shows a similar structure at slightly lower scale, with roughly $40.4K of inflow across both the 7 and 30 day windows, coming from five wallets.

NOCK also remains constructive, with about $38.0K over 7 days adding to a $27.2K positive 30 day balance, driven by three wallets. The flow is smaller, but the absence of longer term pressure keeps the profile supportive.

Where the read shifts is in names where 7 day inflows are working against still negative 30 day trends. CLANKER shows roughly $40.1K of weekly inflow, but that sits against a $80.5K net outflow over 30 days, with activity coming from four wallets. BUTTCOIN looks similar but larger, with about $32.2K over 7 days versus a much deeper $134.8K 30 day drawdown, despite 32 wallets taking positions. In both cases, the wallet count signals attention, but the longer window suggests stabilization or repositioning rather than confirmed accumulation.

The Chinese memecoin segment continues to show interest, but the momentum appears to be slowing rather than extending. 哈基米 has seen about $26.9K of 7 day inflow across 11 wallets, yet remains down roughly $126.7K over 30 days.

Overall, capital remains selective and deliberate. Positive 30 day balances continue to define which names are structurally supported, while 7 day flows highlight where interest is reinforcing those trends or cautiously rotating back into names that have already corrected. In this regime, persistence and participation matter more than size, and confidence shows up most clearly where inflows are sustained and shared rather than fleeting or concentrated.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply