- Crypto Pragmatist by M6 Labs

- Posts

- Markets De-Risk as Uncertainty Hits Extremes

Markets De-Risk as Uncertainty Hits Extremes

Macro Stress Rises, New Investor Demand Fades, Sentiment Breaks Lower

The Coiners

February 14, 2026

GM Anon!

Macro tightened its grip again this week, with risk assets reversing sharply as equities and commodities sold off together and positioning shifted toward defense. The backdrop remains fragile despite strong U.S. jobs data, with rising consumer delinquencies, earnings yields near historic lows, and global uncertainty at record levels. At the same time, nearly $10T of U.S. debt set to mature over the next year is reinforcing concerns that heavy Treasury supply could keep liquidity tight.

Crypto struggled to absorb the shift. Prices moved lower and ranged alongside the broader risk-off move, sentiment fell to extreme fear, and new investor flows turned negative. With BTC trading well below short-term holder cost basis and recent buyers sitting on large unrealized losses, supply pressure remains elevated. For now, markets are trading defense first, with risk appetite thin and stabilization still unproven.

TLDR

Broad risk-off move as stocks and commodities reversed lower; gold fell below $5K and silver below $80.

Macro backdrop fragile despite strong jobs data, with delinquencies rising, earnings yields near 100-year lows, and a potential U.S. shutdown.

Hedge funds added record equity shorts as positioning shifted decisively toward defense.

Crypto sold off with risk assets; BTC and ETH remain highly macro-driven as Fear & Greed hit a record low of 5.

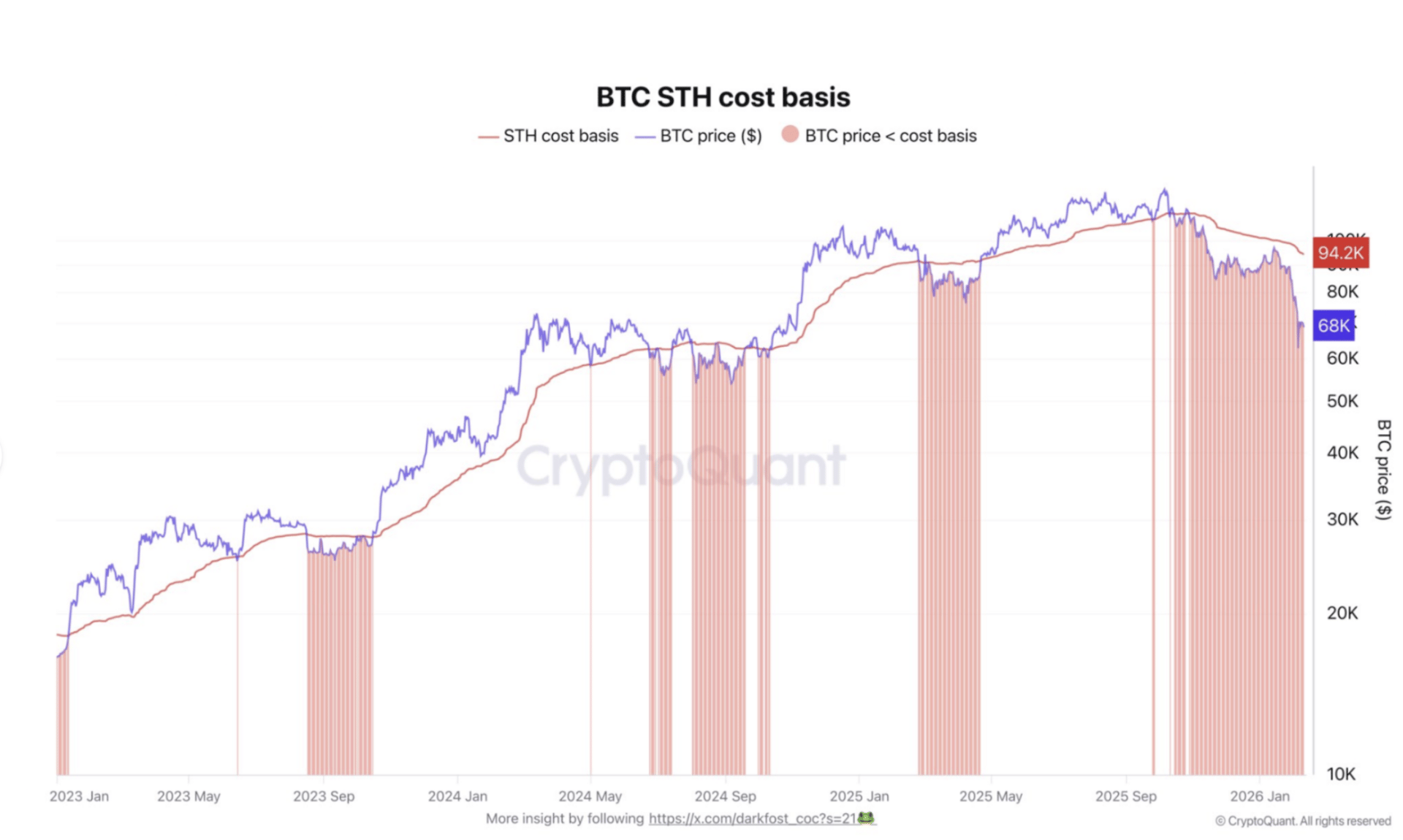

BTC is trading near $68K, ~28% below the $94.2K short-term holder cost basis, increasing capitulation risk and overhead supply.

New investor demand has turned negative, with ~$2.6B in outflows, signaling weakening momentum and distribution.

Institutional flows are mixed: Goldman cut BTC ETF exposure, but Binance (~$300M BTC) and Strategy ($90M BTC) continue selective accumulation.

The World Uncertainty Index hit an all-time high, pointing to tighter financial conditions, higher volatility, and reduced risk appetite.

Structural adoption continues beneath the surface, with tokenization growth ($6B tokenized gold), DeFi–TradFi integration, and new infrastructure launches.

Rising refinancing risk (~$10T U.S. debt maturing) threatens to absorb liquidity, reinforcing a macro environment of tight conditions and pressure on risk assets.

BTC isn’t in trend mode right now. It’s in consolidation mode and that’s usually where the best positioning gets built.

While price chops, the real tells are elsewhere: macro catalysts lining up, flows getting more informative than candles, and long-term holder activity staying constructive. That mix tends to matter most before the move feels obvious.

That’s why we’ve tightened up our daily + weekly BTC updates around what actually moves the tape: key levels, ETF and on-chain flows, derivatives positioning, and a clean “what changed / what’s next” read.

If you’ve been half-checked-out, this is the easiest way to plug back in without doomscrolling or trying to nail the perfect entry.

If BTC stays range-bound, this is also where grid bots make sense: capture the chop, reduce emotion, let structure do the work.

And if you want to talk it through with other serious traders, jump back into the Circle.

Keep an eye on the Bitcoin Chart Tracker for the key zones, and use the Bitcoin Hub for the deeper flow and holder data.

This is a good window to get positioned early instead of getting convinced late.

See you inside,

The Coiners

Market Update

A sharp reversal across risk assets set the tone for the week, with equities and commodities selling off together as sentiment deteriorated. Silver broke below $80 and gold fell under $5K, signaling broad liquidation rather than rotation into defensives. AI disruption fears weighed heavily on real estate, freight, and wealth manager stocks, while Alphabet’s plan to raise $32B in debt to fund AI capex reinforced concerns about rising cost burdens across the sector.

Despite much stronger-than-expected U.S. jobs data, the macro backdrop remains fragile: consumer delinquencies have reached a decade high, the S&P 500 earnings yield sits near 100-year lows, and markets are facing the risk of a partial U.S. government shutdown. Hedge funds have added record shorts during the equity rout, and although a potential Trump–Xi trade truce offered some stability at the margin, overall positioning has shifted toward defense.

Crypto traded lower alongside the macro move, with BTC and ETH remaining tightly linked to broader risk sentiment. Fear & Greed fell to 5, the lowest level on record, reflecting extreme caution among participants. The market narrative remains conflicted: JP Morgan highlighted BTC support near its $77K production cost, while Standard Chartered warned that further downside pressure is likely.

Longer-term structural themes remain intact, including ETH’s shift toward verifying ZK proofs and ongoing efforts to position the network at the center of AI infrastructure, but in the near term price action continues to be driven by liquidity and macro risk rather than crypto-specific catalysts. Activity within higher-beta segments has been selective, with isolated rebounds failing to shift overall market tone.

Institutional signals were mixed and leaned cautious. Goldman Sachs reduced its BTC ETF holdings by 40% in Q4, while digital asset investment products recorded $187M in weekly outflows, though the pace of redemptions has slowed. At the same time, strategic accumulation continued beneath the surface: Binance has purchased roughly $300M in BTC toward a $1B target, Strategy added $90M of BTC, and corporate treasury activity included $84M of ETH purchases by BMNR. Bhutan sold $6.7M of BTC, reinforcing how marginal sovereign and institutional flows are influencing short-term supply dynamics. The overall picture is one of selective accumulation by committed holders rather than broad-based institutional demand.

Under the surface, infrastructure, tokenization, and onchain financial rails remain areas of continued development despite weak price action. LayerZero introduced the Zero blockchain, Robinhood launched a blockchain testnet, and Coinbase rolled out Agentic Wallets as the industry pushes deeper into automation and AI-linked use cases.

In DeFi, Aave plans to direct 100% of protocol revenue to its DAO, while reports that BlackRock may offer DeFi trading via Uniswap highlight the continued convergence between traditional finance and onchain liquidity. Tokenized funds being enabled as collateral through a Financial Times–Binance initiative, the UK selecting HSBC for a tokenized bond, and tokenized gold reaching a $6B market cap all point to steady institutional adoption of real-world asset infrastructure even as market conditions remain risk-off.

Regulatory and corporate developments added to the cautious backdrop. A White House session on a crypto bill ended without progress, while U.S. banking access remains contested amid calls to delay OCC charters for crypto firms. Internationally, the policy environment remains mixed: the EU is seeking to ban Russian crypto transactions and China is moving to prohibit RWA tokenization, while Hong Kong plans to allow crypto margin financing and perpetual contracts and Denmark’s Danske Bank has lifted its eight-year crypto ban.

Corporate headlines reinforced the industry’s transitional phase, with Coinbase reporting a $664M Q4 loss, Kraken removing its CFO ahead of a planned IPO, Blockchain.com securing UK FCA registration, and several major fraud cases resulting in prison sentences. Together, the week’s developments reflect a market still dominated by macro risk and policy uncertainty, with positioning defensive and conviction dependent on a clear improvement in liquidity conditions.

Market Data Points

Short-term holders are deep underwater, with BTC trading near $68K against an estimated STH cost basis of ~$94.2K. This places recent buyers at roughly 28% unrealized losses, a level that historically increases the probability of capitulation-driven selling.

The extended period of price below the STH cost basis reflects ongoing distribution and weak conviction among newer market participants. Until price reclaims this level, short-term holder supply is likely to remain a source of overhead pressure, with any rallies facing increased sell-side liquidity from holders looking to exit at breakeven.

The World Uncertainty Index has surged to a record high, signaling a sharp deterioration in the global macro backdrop as policy risk, geopolitical tension, and economic instability converge.

Historically, spikes of this magnitude coincide with tightening financial conditions, reduced risk appetite, and elevated market volatility as investors shift toward capital preservation. In this environment, liquidity becomes more selective, cross-asset correlations rise, and risk assets face persistent pressure until uncertainty begins to ease and macro visibility improves.

New investor flows have turned negative, with roughly $2.6B in net outflows, signaling that fresh capital is no longer supporting current price levels. Historically, strong bull phases are sustained by persistent new money entering the market, while periods of declining or negative inflows reflect weakening demand and a shift toward distribution.

The recent contraction suggests momentum is fading, leaving price increasingly dependent on existing holders rather than new buyers. Until new capital returns, the market is likely to remain fragile, with reduced upside strength and a higher sensitivity to selling pressure.

Refinancing risk is rising sharply, with nearly $10T of U.S. government debt—about one-third of total outstanding—set to mature within the next year. This creates a significant funding challenge that increases the market’s reliance on strong Treasury demand and stable interest rates. If yields remain elevated or demand weakens, the government will be forced to refinance at higher costs, tightening financial conditions across the economy.

Coin Moves

Large caps traded with a defensive tone over the past week, as capital remained concentrated in the highest-liquidity assets while the broader market retraced. BTC declined modestly and held in the high-$60K range, continuing to act as the market’s primary stability anchor despite failing to regain upward momentum. ETH showed relative resilience with only a shallow pullback, reinforcing the pattern of institutional and core flow staying concentrated in the two dominant assets. Beyond the top tier, the large-cap complex broadly moved lower, with most majors declining in the mid-single-digit range. The notable exception was TRX, which posted a modest weekly gain, pointing to selective rotation into more defensive large-cap exposure rather than a broad risk-on shift.

Below the majors, performance was highly fragmented. Several established mid-cap names delivered high single-digit to low double-digit gains, including HBAR, NEXO, ZEC, and XMR, while others such as QNT, BCH, and ATOM advanced more modestly. The absence of leadership from any single sector suggests opportunistic positioning rather than a coordinated rotation into altcoins. Further down the market cap curve, dispersion widened significantly, with multiple smaller-cap tokens posting outsized moves ranging from 20% to well over 100%.

Overall, market structure remains defensive. Capital continues to favor BTC and ETH, breadth is narrow, and performance dispersion remains elevated. Upside participation is selective and momentum-driven, while downside pressure is broader across risk-sensitive areas. The current distribution of returns reflects a market prioritizing liquidity and capital preservation, with conviction insufficient to support any type of sustained recovery.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply