- Crypto Pragmatist by M6 Labs

- Posts

- Markets Hold The Line, Liquidity Stays Thin

Markets Hold The Line, Liquidity Stays Thin

BTC Slips Back Under $90K, Sovereigns Accumulate, Alts Lag as Trenches Collapse

The Coiners

December 06, 2025

GM Anon!

The market is still sitting on unstable ground, but not in a one-way bearish story. This week split sentiment again: some see the start of a deeper unwind, others think we’re just stretching the cycle rather than topping it.

Near-term price action is messy, but the backdrop hasn’t broken. Macro is noisy, not hostile — funding support is creeping in, rate-cut expectations are surging, and the tape is trying to stabilize even as BTC keeps slipping back under key levels. Let’s dive in!

TLDR

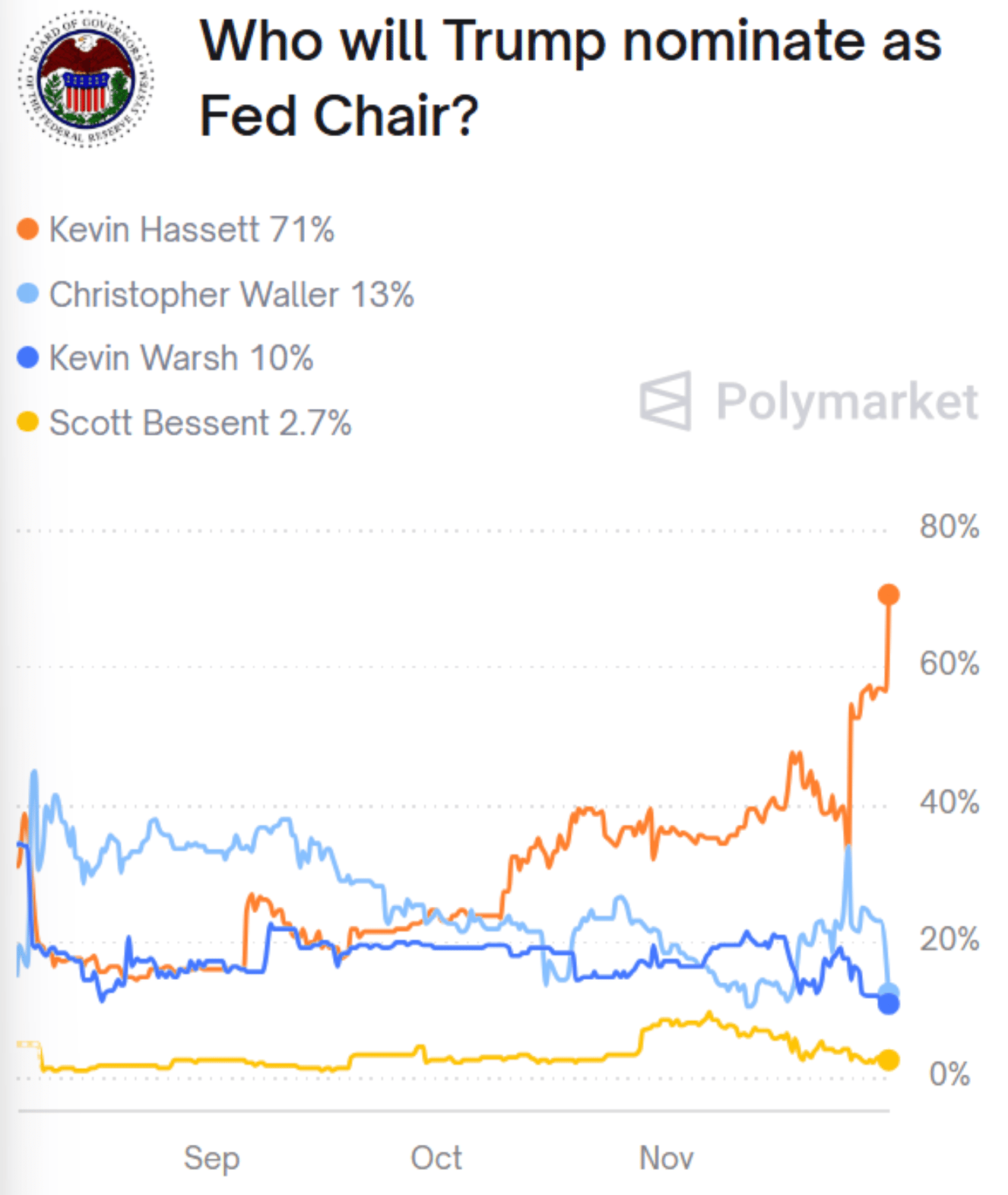

Macro stayed choppy: BoJ likely to hike, Hassett eyed for Fed, Fed adds $13.5B via repos.

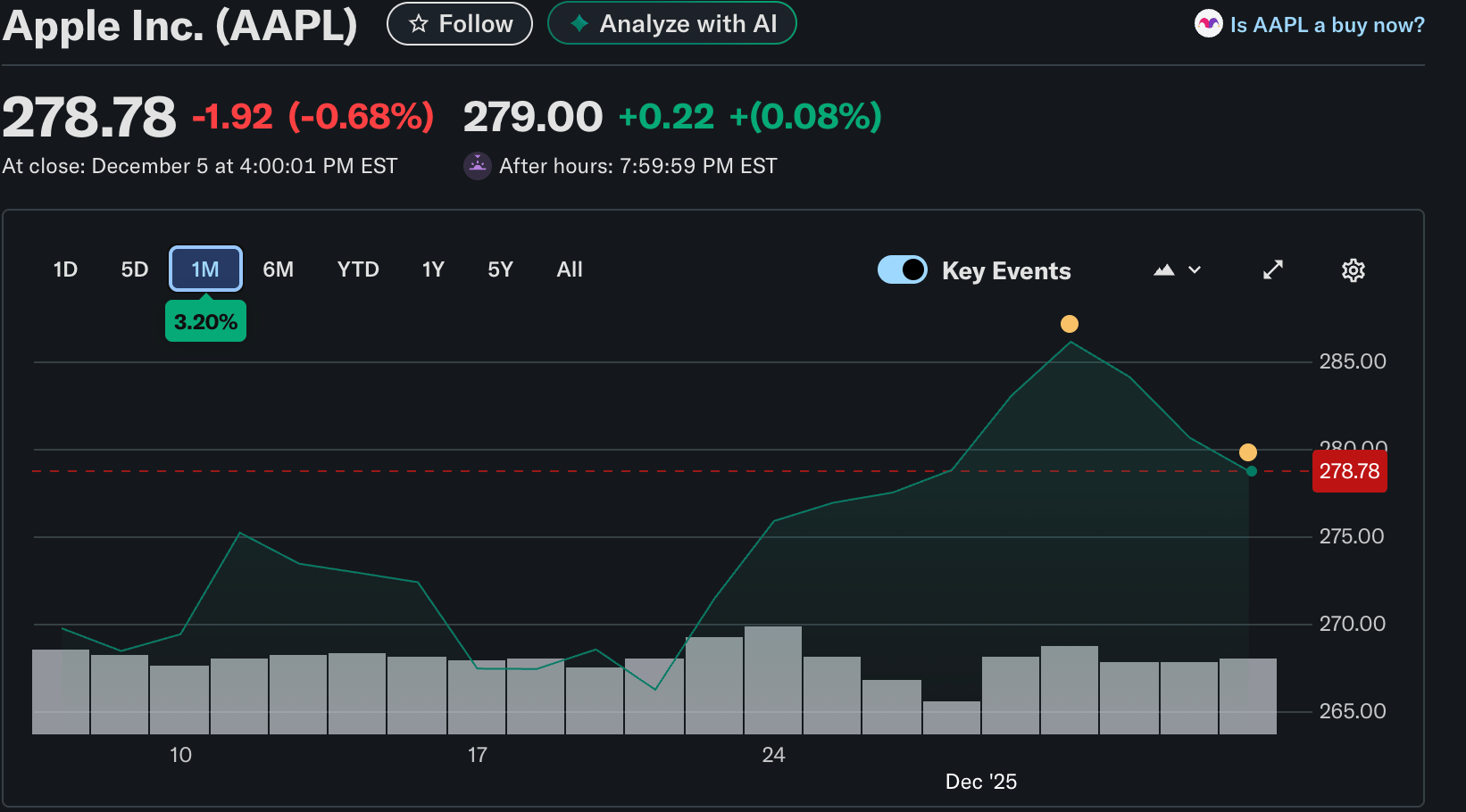

Apple hit a new ATH and $4.2T market cap while funding conditions stayed fragile.

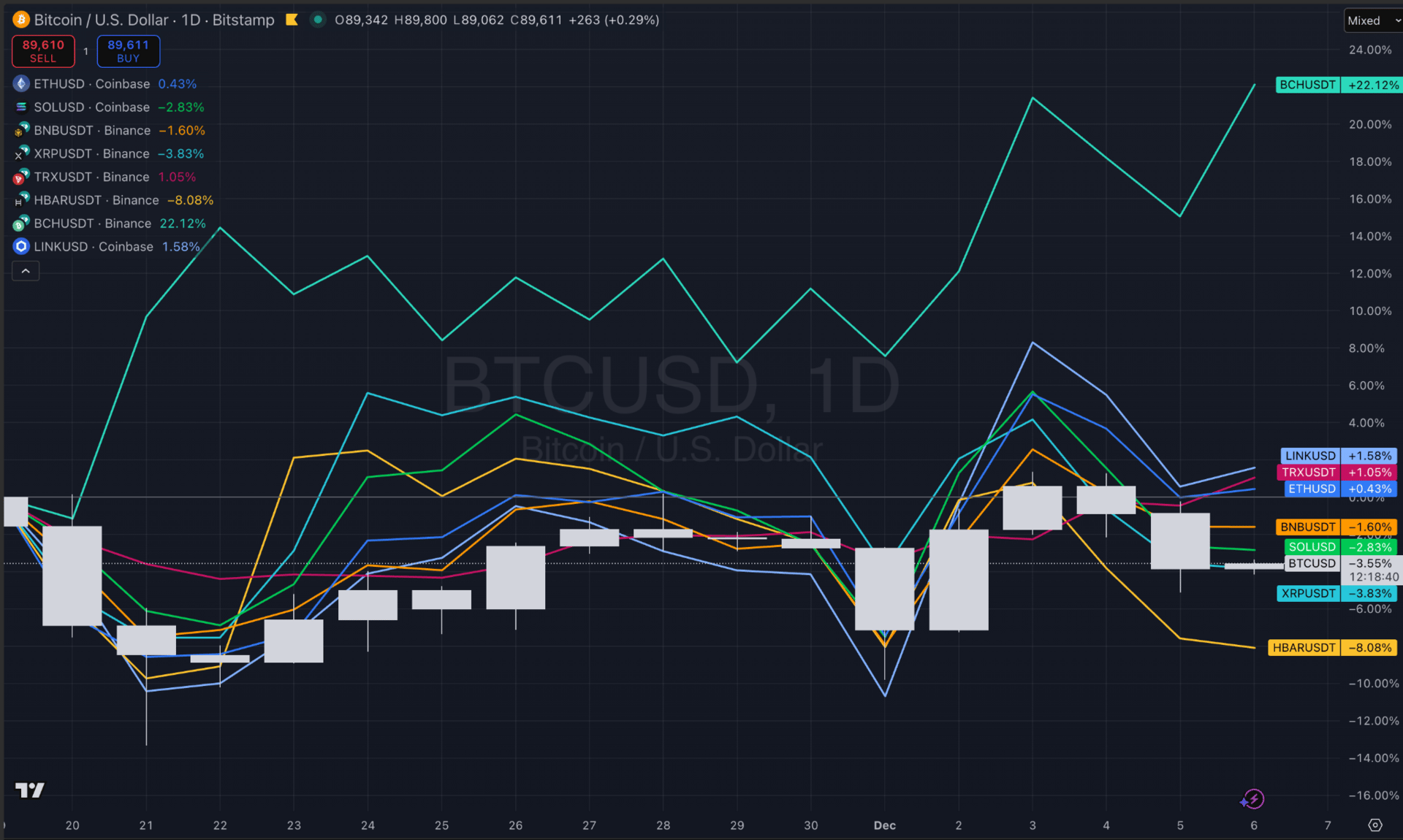

BTC chopped: ETF outflows spiked, a mid-week pump faded, and price slipped back under 90K.

Miner margins are tight, liquidity thin, but sovereign funds and Strategy are still adding BTC.

ETH shipped Fusaka and pushed ZK privacy, even as DAT purchases dropped sharply.

Tokenisation ramped: Kraken bought Backed Finance, Nasdaq and Sony moved on RWAs/stablecoins, PYUSD supply tripled.

Regulators were busy across US, EU, UK and Asia, with MiCAR’s Dec 30 deadline locked in.

Perp DEXs and on-chain rails remain core to price discovery and risk transfer.

Trenches have gone quiet as liquidity shifts to prediction markets with far higher volumes.

Only a few small caps (ADS, CLANKER, BIBI, NYAN, etc.) saw modest smart-money inflows.

The recent flush was one of the ugliest in a long time — the kind of move that makes people close the chart and step away for a while.

But this is exactly when you don’t look away. ⚠️

BTC is already telling a story before the headlines catch up. Not clearly bullish or bearish, but important: who’s buying, who’s forced to sell, and which levels matter. This is where positioning quietly counts.

We’re tightening our daily and weekly BTC updates around that: key levels, flows, what actually moved the market, what the market reacted to, and what’s worth watching next. If you’ve checked out for a bit, this is the cleanest way to plug back in without diving into chaos or doomscrolling.

If you want to stay active without playing emotional roulette trying to “nail the bottom,” this is also the kind of tape where grid bots make sense — slow DCA, range capture, letting structure do the work while everyone else panics. 📈

Now is also a good time to come back into the Circle community. If you’ve been drifting, this is a natural moment to reconnect, compare notes, and walk through what’s happening under the surface step by step.

Keep an eye on the Bitcoin chart tracker to see how the key zones are evolving.

And use the Bitcoin Hub for the deeper data and flows driving the move.

See you inside,

The Coiners

Market Update

Macro was noisy again this week. The BoJ is now seen as likely to hike this month, while in the US the market is adjusting to the idea of Hassett as the next Fed chair. The Fed quietly added $13.5B via overnight repos, a reminder that funding conditions are still delicate even as risk assets grind higher at the index level.

Apple continues to do the heavy lifting for equities, pushing to a fresh all-time high and a $4.2T market cap. At the policy level, the IMF warned that large stablecoin footprints could weaken central bank control, and China doubled down on its crypto ban and stablecoin risk messaging, setting a cautious tone around monetary sovereignty.

Crypto chopped around rather than trending. After BTC ETFs logged their largest daily outflow in two weeks, we saw a sharp mid-week pump as rate-cut odds firmed and Vanguard’s decision to allow crypto ETFs hit the tape, briefly improving sentiment. That strength didn’t fully stick, though; BTC rolled back over and dipped below 90K again into the end of the week.

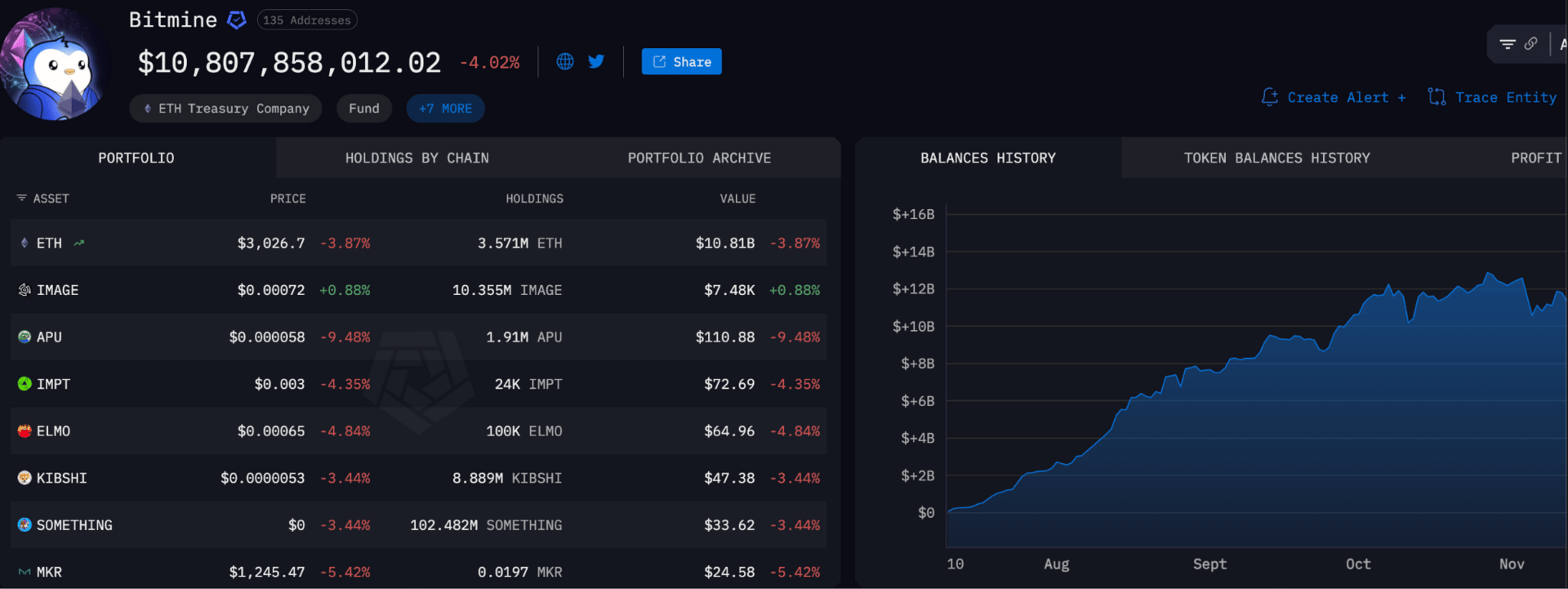

Larry Fink flagged sovereign wealth funds as active BTC buyers, providing a clearer anchor for the bid at the top of the market even as miners face the toughest margin squeeze of the cycle. Strategy leaned into that narrative, building a $1.44B dividend reserve and reiterating that selling BTC is a last resort; JPMorgan framed the firm’s balance-sheet resilience as a key piece of the BTC story. On the ETH side, the Fusaka upgrade went live, ZK privacy work moved forward, and BitMine’s holdings crossed 3% of supply, even as ETH DAT purchases slowed sharply to 370K ETH in November.

Institutional and tokenisation themes stayed busy beneath the price action. Kraken bought Backed Finance to deepen its RWA and tokenised-securities stack, while Nasdaq said it intends to move fast on tokenised stocks and Sony laid groundwork for a USD stablecoin.

EU banks kept pushing ahead on a EUR-denominated stablecoin, and PYUSD’s supply has already tripled since September. Hashkey cleared a key hearing and is set to start its IPO process next week, highlighting Hong Kong’s push to position itself as a regulated hub. Strategy’s balance-sheet moves, Vanguard’s ETF pivot and sovereign allocations all point to a slow but steady broadening of the institutional base, even as spot and derivatives volume on exchanges sits at the lowest levels since June.

On-chain and DeFi activity was more selective. Aave’s DAO is openly questioning the cost/benefit of its multichain expansion, while Yearn recovered $2.4M in stolen assets and ETH perps DEX Lighter added spot trading. Tokenisation and crypto finance kept building out: Sonnet shareholders approved a $1B HYPE DAT merger, Kalshi moved its prediction markets fully on-chain using Solana, and Base prepared to support SOL-based assets natively.

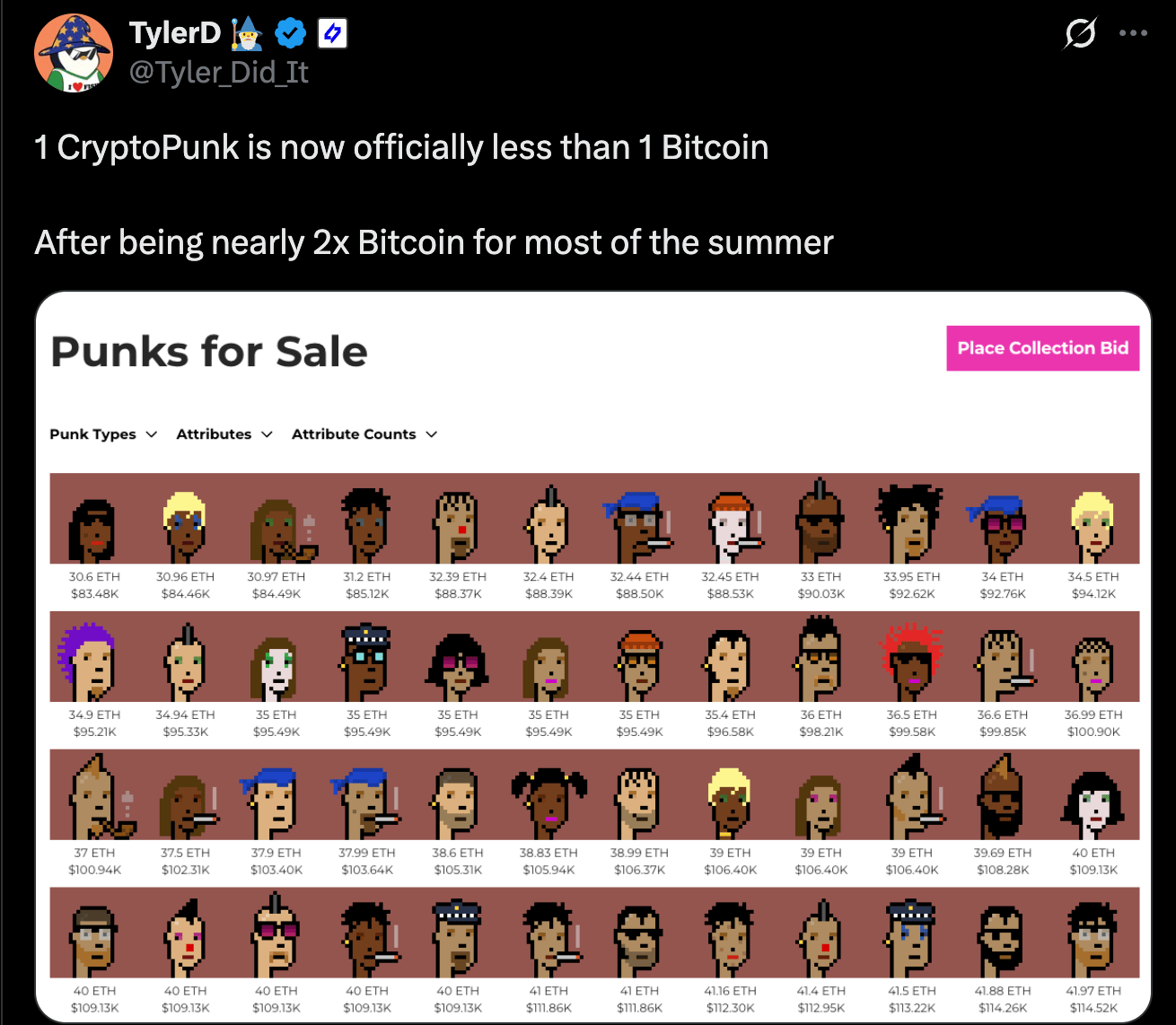

At the same time, BTC miners are under pressure, Cloudflare outages briefly disrupted crypto apps, and Huoine Pay had to shut down until January 5 after bank-run style stress. In the culture corner, Pudgy Penguins announced an NHL partnership and Punk floors slipped below BTC, highlighting how thin liquidity is even at the top of NFT collections.

Regulators and policymakers stayed active across regions. South Korea pushed forward both the second phase of its crypto act and a separate stablecoin bill, Russia signaled it may loosen parts of its crypto regime, and Argentina’s state energy firm YPF floated the idea of accepting crypto payments.

The UK passed a bill that brings property law explicitly to bear on digital assets, while Italy pinned down December 30 as the end of MiCAR’s transition period. Germany and Switzerland jointly shut down a $1.4B mixer, and the FDIC is preparing a December proposal for GENIUS implementation.

The SEC flagged an “innovation exemption” for crypto coming in about a month, even as CoinShares pulled back XRP, SOL and LTC ETF filings. Against that backdrop, Binance named He Yi as co-CEO, Upbit’s audit of a $30M hack uncovered a wallet flaw, and Tether’s CEO went back on the record defending USDT’s asset coverage. The net effect is a market that’s still feeling heavy on activity and light on outright risk-taking, but with clear signs that the institutional and regulatory rails are getting built regardless of short-term price noise.

Market Data Points

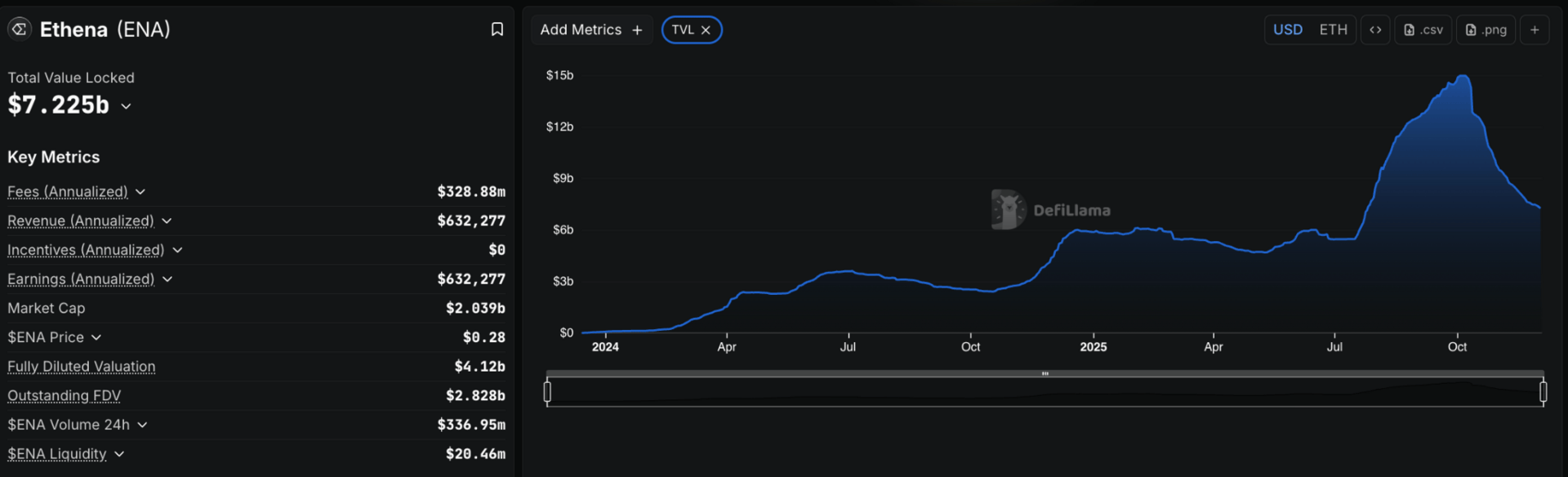

Ethena’s TVL has been cut roughly in half — from ~$15B to ~$7B — after a brief USDe de-peg on Binance spooked leveraged arb flows and forced a rapid unwind. The shock exposed how much TVL was tied to positive spread trades rather than sticky demand, and it arrived alongside ecosystem setbacks like the shutdown of Terminal Finance.

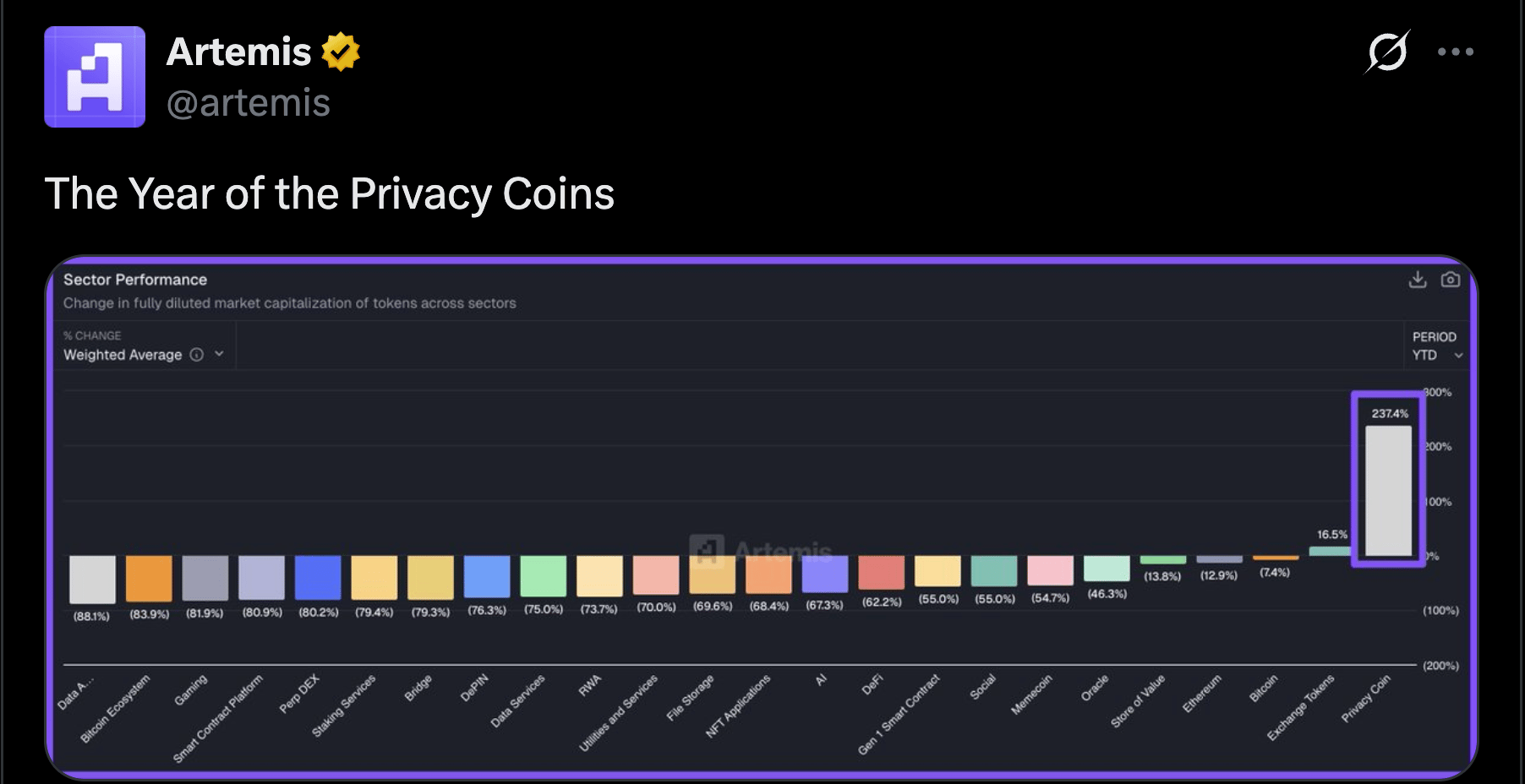

Privacy has been the outlier trade this year. Privacy Coins are up roughly +237% YTD, while nearly every other bucket shows deep double-digit declines—many in the -50% to -80% range. Even the sturdier categories lag: ETH screens modestly positive at about +16%, BTC shows a small YTD dip, and exchange tokens sit slightly negative.

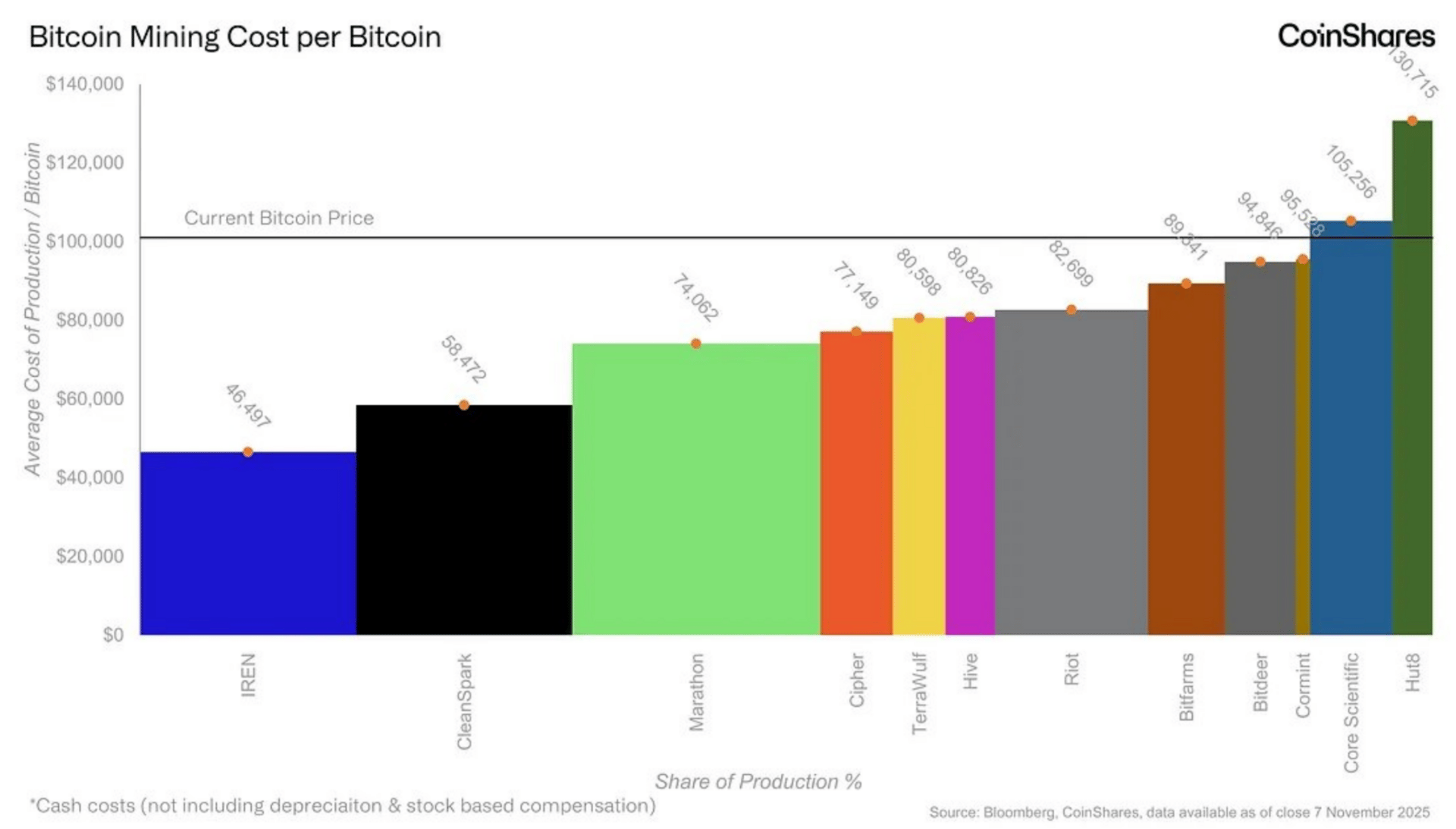

Public miners’ cost curve has shifted higher. CoinShares pegs the average cash cost to mine 1 BTC at ~$74.6K in Q2’25, and the all-in average (incl. depreciation and stock comp) at ~$137.8K. The dispersion is wide—low-cost operators still clear healthy margins, while higher-cost names are effectively at or above breakeven on an all-in basis—implying tighter balance sheets, more treasury selling risk, and a fresh incentive for efficiency gains and consolidation if price softens. In short: the industry is far more price-sensitive than earlier in the cycle, and cost leadership matters.

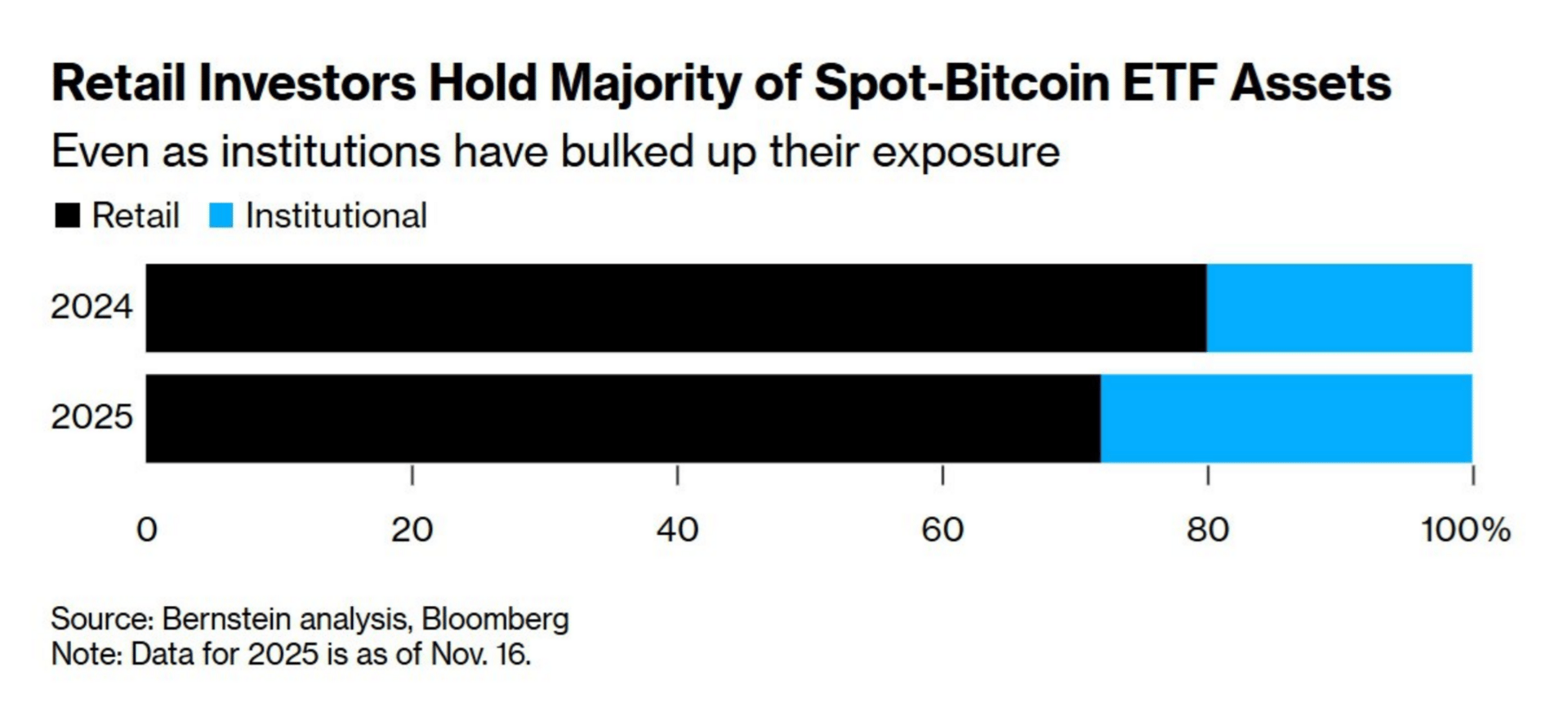

Retail still owns the spot-BTC ETF story. Bernstein estimates retail holds roughly three-quarters of assets, while institutional ownership has climbed from about 20% at end-2024 to 28% as of Nov 16, 2025. The mix says depth is improving without crowding out the original buyer base—institutions are scaling in, but flows remain retail-led, which helps explain the stop-start tape and sensitivity to headlines.

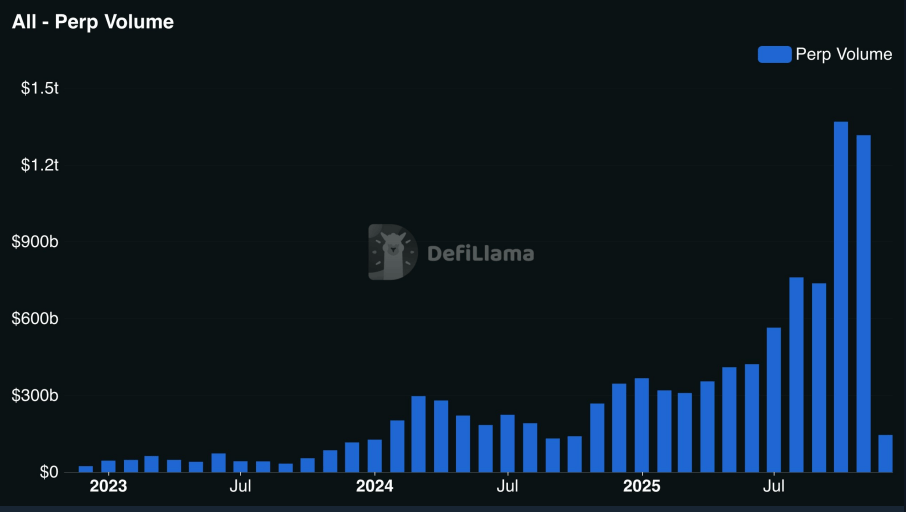

Perp DEXs just cleared $1T in volume for the second straight month in November — roughly 4× year-on-year and 15× over two years. That’s not a niche anymore; it’s a core venue for price discovery and risk transfer. Liquidity is clustering on a few leading protocols, spreads are tighter, and on-chain funding now meaningfully steers positioning alongside CEXs. The upside is resilience and 24/7 composability; the caveat is higher leverage cycling faster through the system, which can amplify moves when funding flips or liquidity thins.

Majors & Memes

Majors were mostly range-bound this week with a slight downside bias. BTC slipped about 1% over seven days as volatility compressed after the mid-week swing, while ETH eked out a 1.2% gain. BNB was essentially flat with a small uptick, and SOL drifted lower by roughly 2.6% after failing to hold brief strength. XRP was the clear laggard in the top tier, down 7.2%, while TRX stood out with a 3.3% rise, again behaving as a defensive outlier in an otherwise choppy tape.

Below the majors, leadership was narrow. HASH, BCH, RAIN, LINK, and WBT featured among the stronger names, posting single- to low double-digit gains as capital rotated into a handful of stories rather than the broader alt complex. Further out on the risk curve, speculative names drove the biggest moves: PIPPIN, LUNC, ALCH, BUILDON, ULTIMA, BEAT, MYX, FARTCOIN, BTSE, TEL, and EGLD all logged outsized weekly advances, reflecting targeted momentum rather than a broad-based altcoin move.

On the downside, weakness was more widely distributed. ZEC and CC led the sell-off with drops north of 25%, while APT, ICP, FLR, KCS, HYPE, AVAX, POL, UNI, ASTER, WLD, ONDO, NEAR, and ATOM all traded heavily lower, mostly in the low- to mid-teens. Smaller caps such as LGCT, MON, FTN, HAJIME, DCR, XPL, STRK, UDS, DASH, APEPE, MORPHO, EIGEN, and DEXE posted similarly sharp retracements. The overall pattern is consistent with a cautious, liquidity-first market: majors are holding in a broad range, while alts remain a high-beta expression where traders are quick to punish weakness and selectively reward only the cleanest momentum setups.

Smart Money Moves

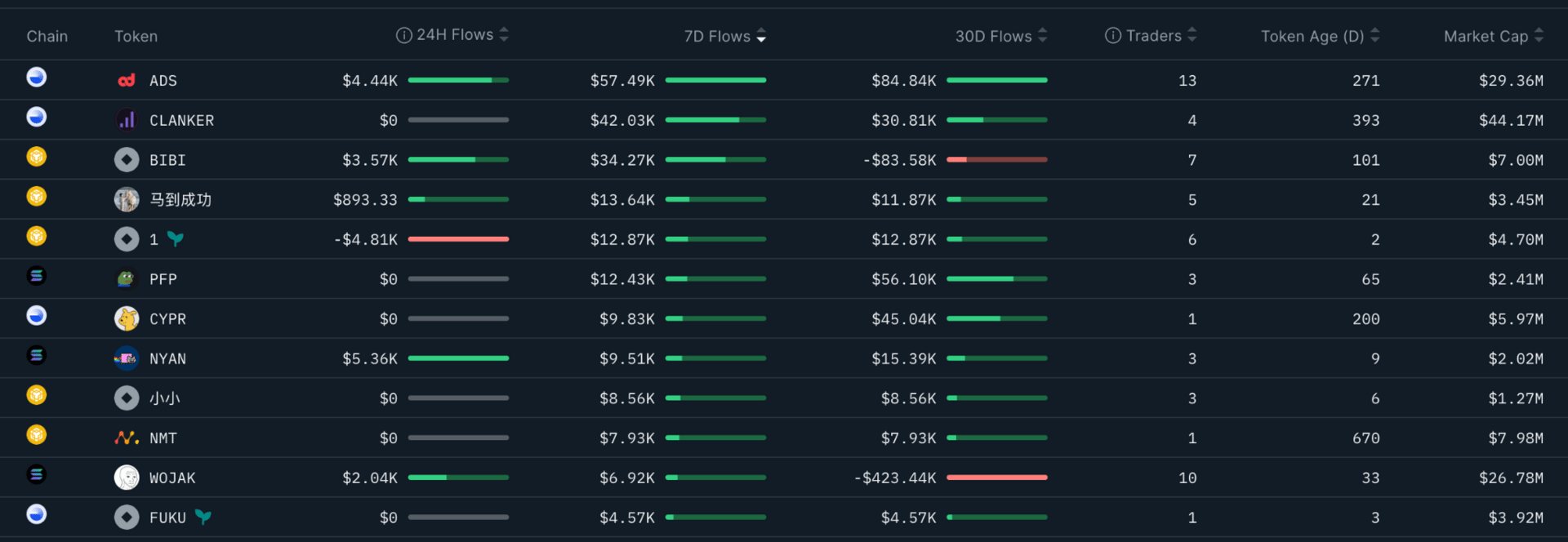

Activity in the trenches has fallen off hard, and the shift is visible everywhere. The usual rotation into microcaps has evaporated, liquidity is thin, and the heat maps that once lit up with constant churn now look flat. The token-popularity charts makes the picture obvious: where attention was once concentrated across a handful of high-velocity names, interest collapsed almost overnight, splintering into smaller pockets with none of the prior momentum.

Most of that flow has migrated into prediction markets, which have become the new outlet for risk-taking. Traders who spent the year grinding through low-float memes and microcaps are now sizing into real-world event markets instead, where outcomes feel cleaner and liquidity is deeper. Volumes across major PM platforms are now several multiples higher than what SOL-based trading bots or meme pools are seeing.

Even so, a few tokens managed to attract smart-money interest over the last seven days, though the scale is modest compared to prior cycles. Names like ADS, CLANKER, BIBI, and NYAN saw small but visible inflows, with ADS and CLANKER leading on 7D accumulation and a handful of traders leaning into them despite the broader slowdown. PFP, CYPR, 马到成功, 1, and WOJAK also picked up lighter bids, though the flows remain shallow and far from conviction size. These aren’t breakout setups — they’re more like selective probes in an otherwise frozen market.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply