- Crypto Pragmatist by M6 Labs

- Posts

- The Start Of A New Phase

GM Anon,

Markets are getting spicy— CPI cooled, gold melted, and futures whipsawed like it’s 2021 déjà vu. BTC flexed back to 60% dominance while ETH stole headlines with a staked ETF filing and big on-chain moves. SOL kept the vibe alive with its own ETF approval, and even Up Only is back from the dead — peak bull nostalgia.

Let’s break it down.

TLDR

Futures swung on trade headlines and soft CPI; gold plunged 5%, its biggest drop in years.

U.S. shutdown entered week four as Trump–Xi talks set for next week.

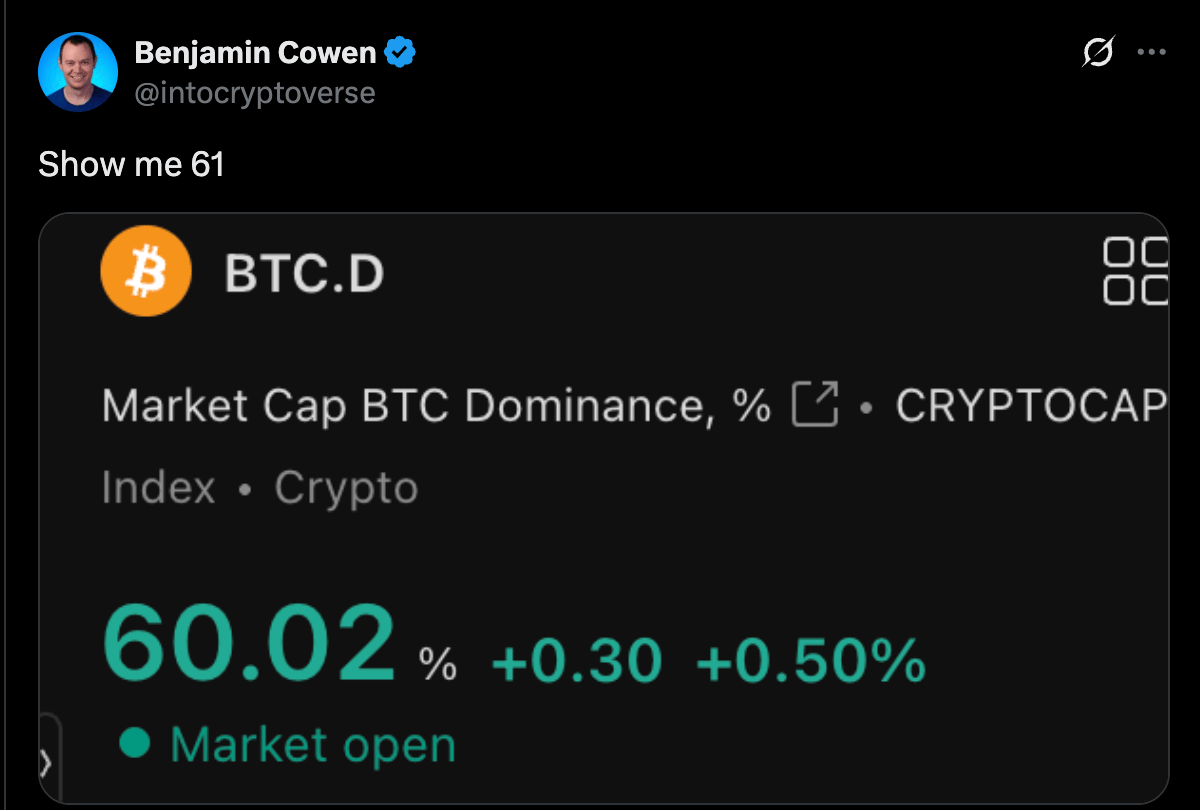

BTC dominance hit 60%; miner wallet with 4K BTC reactivated.

ETH saw $654M moved, VanEck filed staked-ETH ETF, JPMorgan okayed BTC/ETH collateral.

SOL gained traction with HK’s first SOL ETF, Gemini credit card, and new Perps DEX plans.

Institutional flow strong: BlackRock courting BTC whales, T. Rowe Price and 150+ ETF filings pending.

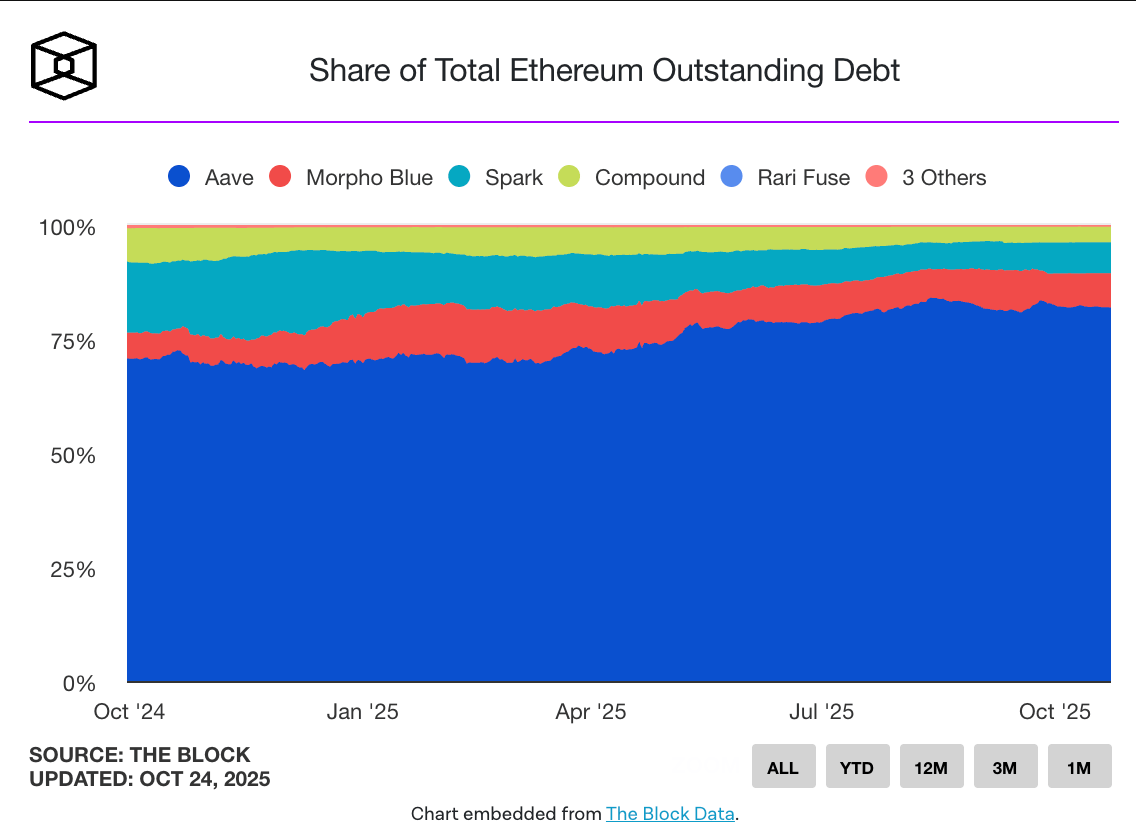

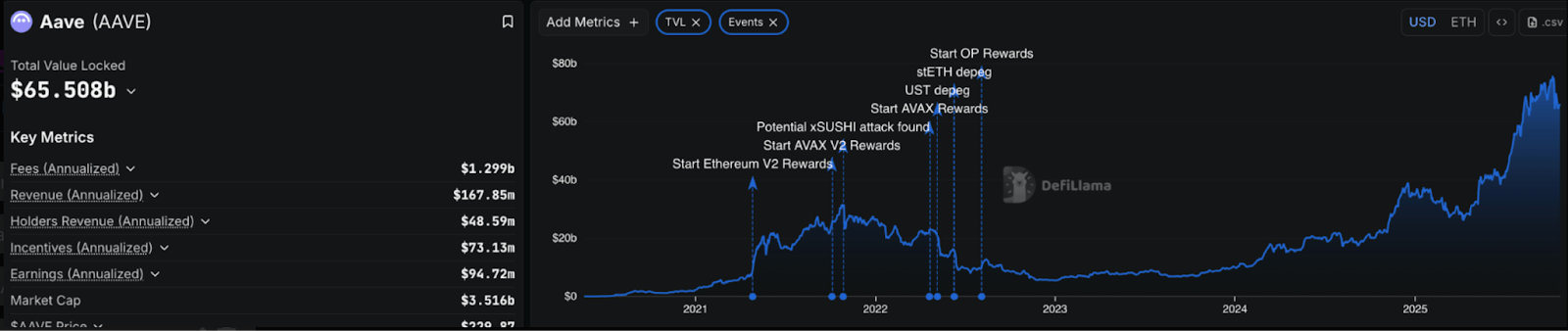

Aave loans hit $25B; DeFi profits led by derivatives and launchpads.

L2s led inflows as capital rotated from ETH and BNB.

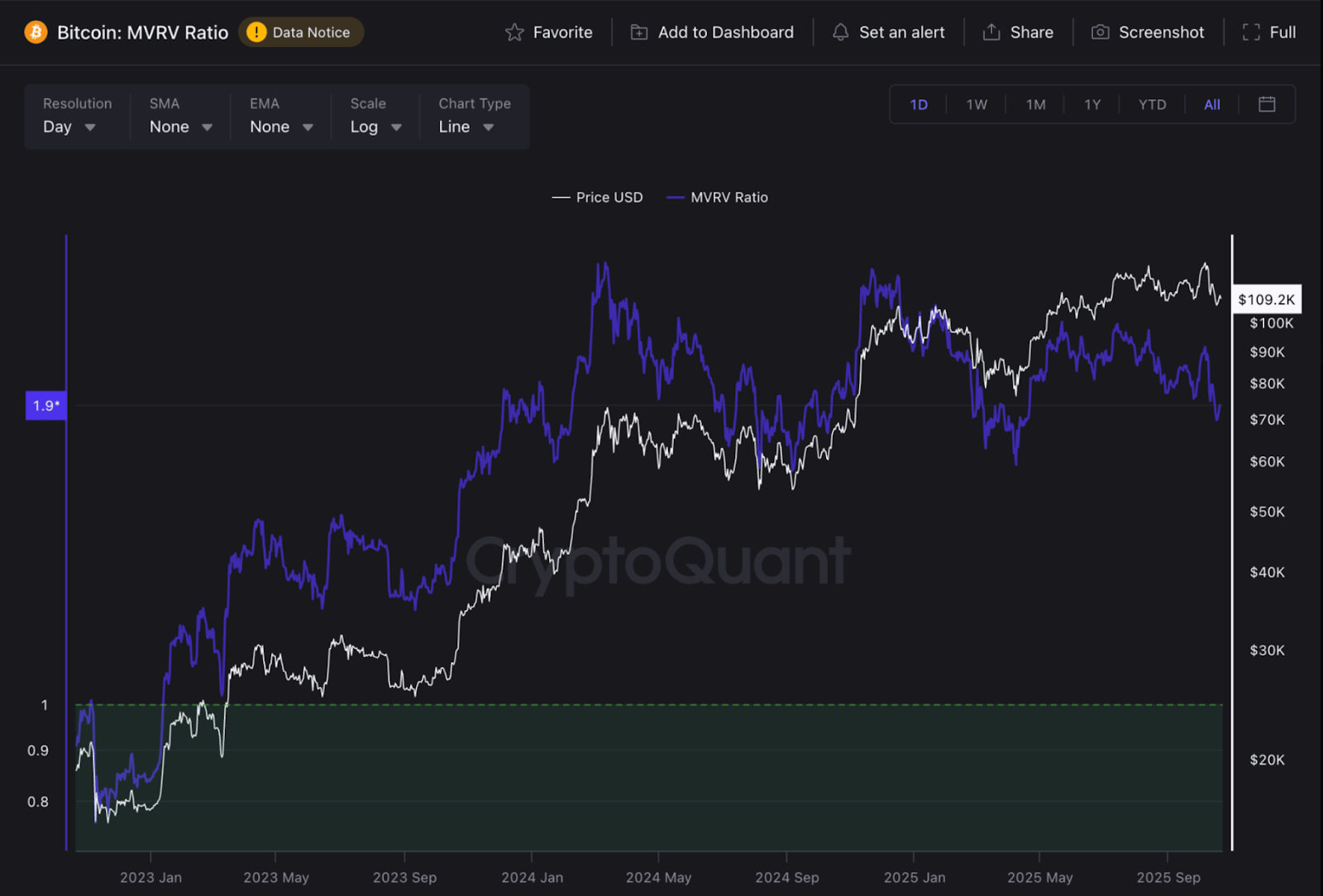

MVRV near 1.9 signals distribution; BTC likely range-bound.

Regulators advance 2025 framework; Revolut gains MiCA license, Kadena shuts down.

Join The Coiners + Get in on the $50K Grid Bot Challenge 🚀

Don’t wait, Anon — it’s free and will level up your trading game. As a member, you’ll unlock:

High-calibre crypto trading alerts

Weekly live streams with expert trader Michael Whitman (Wed Q&A + Fri Market Recap)

Real-time strategies straight from the pros

🔥 Plus, get front-row access to our $50K Grid Bot Challenge — we’re putting $50K into Pionex Grid Bots and you can follow along every step:

✅ Learn the exact ranges + settings we use

✅ Copy the bots into your own account with 1 click

✅ Track live results in real time

✅ Vote on the “Coin of the Week” for a short-term bot

The mission: turn $50K into 6 figures while showing you how to run profitable bots yourself.

Want more? Qualify for VIP access by meeting one of these:

Deposit $100K+ through a partner exchange

Trade $1M+ in monthly volume

Refer 3 friends who sign up

Stay sharp, stay active, and keep stacking edge with The Coiners.

Market Update

Futures whipsawed on the week: initially lower on another round of trade-war headlines, then higher after CPI printed cooler than expected. That eased rate fears but didn’t clear the fog, with the U.S. entering a fourth week of government shutdown even as Trump and Xi were slated to meet in Asia next Thursday.

Safe-haven dynamics flipped as gold sank 5% in its biggest daily drop in years. Meanwhile, tech risk took on a different hue after Google claimed a quantum breakthrough and Washington opened talks to take stakes in quantum-computing firms, a reminder that strategic tech and policy are moving in tandem and can jolt cross-asset positioning.

Crypto traded with a defensive bid under the surface as BTC dominance pushed to 60%, aided by a 4k-BTC miner wallet breaking 14-year dormancy that kept supply narratives front-of-mind. In majors, ETH flow optics were busy: the Ethereum Foundation moved $654M in ETH and VanEck filed for the first staked-ETH ETF, while Fed Governor Waller signaled a shift toward embracing crypto and JPMorgan said it would allow BTC and ETH as collateral—both supportive for institutional onboarding.

SOL headlines skewed structurally constructive even as the ecosystem refocused, with Hong Kong approving the first SOL ETF, the co-founder Toly designing a Perps DEX, Gemini launching a SOL credit card, and Solana ending support for the Saga phone. BNB caught a clean impulse after Trump pardoned CZ, lifting the token 4%, and breadth improved as Robinhood officially listed BNB alongside new alt listings like HYPE.

Institutional and balance-sheet activity accelerated. BlackRock sought to pull BTC whales into its ETFs; T. Rowe Price filed for its first crypto ETF and separately for an actively managed product; JPMorgan’s collateral move and over 150 crypto ETF filings awaiting review added to the queue. Galaxy reported a record quarter with profits up 1500%, FalconX acquired 21Shares, Fireblocks bought authentication startup Dynamic, and Ledger unveiled a next-gen Nano with a new wallet app, all pointing to a deeper infra stack.

On the venture and strategy side, Hayes is raising $250M for a new PE fund, while Hyperliquid Strategies targeted a $1B raise to buy HYPE. Stripe’s Tempo raised $500M at a $5B valuation and hired away Dankrad from the ETH Foundation; Revolut secured a MiCA license and hinted at a stablecoin; Coinbase made moves by buying Cobie’s Echo for $375M and Up Only NFT for $25M.

DeFi sectors were equally active. Aave’s outstanding loans hit $25B with plans to integrate Maple, the DAO proposed a $50M annual token buyback, and the team acquired Stable Finance’s developers. Covalent launched a Strategic Reserve; Solmate announced a validator center with aggressive M&A; Aster DEX rolled out Rocket Launch.

Meanwhile, ZEC spiked through $300 before fading and still led altcoin chatter; HYPE outperformed after a co-founder appearance on TBPN and a prospective bid from Hyperliquid Strategies. Thematic flows were loud: TIBIRR rose to $380M near ATH, LMTS stealth-launched a prediction-market token at $300M, and METEORA debuted at $500M but underwhelmed some—complicated further by claims the top airdrop recipient was the TRUMP team and accusations that its founder led MELANIA and LIBRA. Sports and prediction rails converged as DraftKings acquired Railbird, the NHL struck a deal with Kalshi, Kalshi fielded investment offers at $10B+, and Jupiter launched prediction markets with Kalshi.

Policy and corporate signals rounded out the tape. The SEC and CFTC aimed to finalize a crypto framework by end-2025 as Democrats met with crypto executives on a legislative push; Asian exchanges tightened scrutiny on DATs even as Evernorth’s SPAC planned to be a $1B XRP DAT. Groups pressed Trump to defend the CFPB’s banking rule, while JPMorgan’s collateral greenlight—and Revolut’s MiCA license—showed banks and fintech inching toward standardized engagement. Lastly, Kadena wound down operations with KDA dropping 60% on the news.

Market Data Points

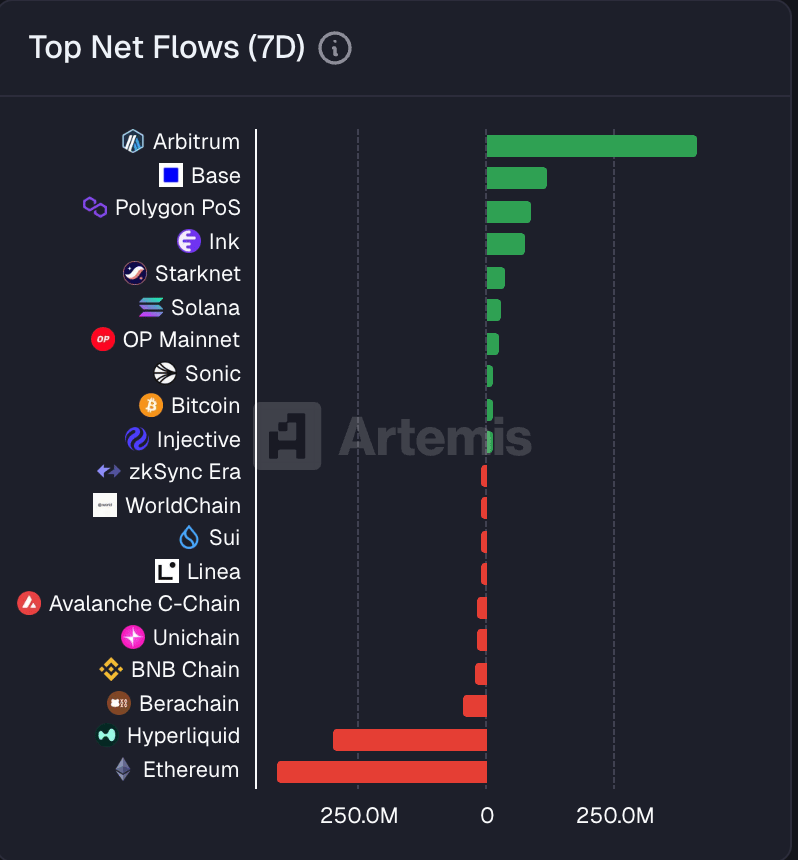

Over the last seven days, Arbitrum dominated with the strongest net inflows across all chains, comfortably leading Base, Polygon, and Ink, which also posted solid positive flows. The top of the chart shows clear rotation toward L2 ecosystems, suggesting that liquidity is chasing cheaper execution and active DeFi environments rather than sitting idle on mainnet. Further down, Solana, Starknet, and OP Mainnet continued to attract moderate inflows, showing steady cross-chain engagement.

On the outflow side, Ethereum saw the largest capital drain, followed by Hyperliquid, Berachain, and BNB Chain — a sign of short-term capital rotation rather than structural weakness. Overall, the trend points to a risk-on shift into L2s and smaller chains, with Ethereum once again serving as the main liquidity source for the rotation.

The MVRV ratio is sitting near 1.9, meaning the average holder’s coins are worth almost twice what they paid. Historically, readings above 2.0 have marked overheated phases where profit-taking intensifies and upside momentum starts to fade. You can see that pattern repeating — each time MVRV spiked above 2.2, price followed with a local peak, then cooled as profits were realized.

The current divergence, with price still near all-time highs while MVRV trends lower, suggests distribution rather than accumulation — holders are in profit, but conviction is thinning. Until this ratio resets closer to the 1.4–1.6 zone (where past bottoms formed), BTC may stay range-bound or face corrective pressure before another strong impulsive leg higher.

October saw Aave’s TVL hit its highest level ever, briefly topping $69B before cooling slightly. The surge through early to mid-October was explosive — a sharp jump that pushed the protocol well past its previous cycle highs from 2021–22.

Unlike those earlier peaks that were mostly incentive-driven, this latest climb reflects a broader return of liquidity and leverage demand across DeFi. Even with the small pullback since the highs, Aave remains at record territory, cementing its spot as the dominant lending protocol in the market right now.

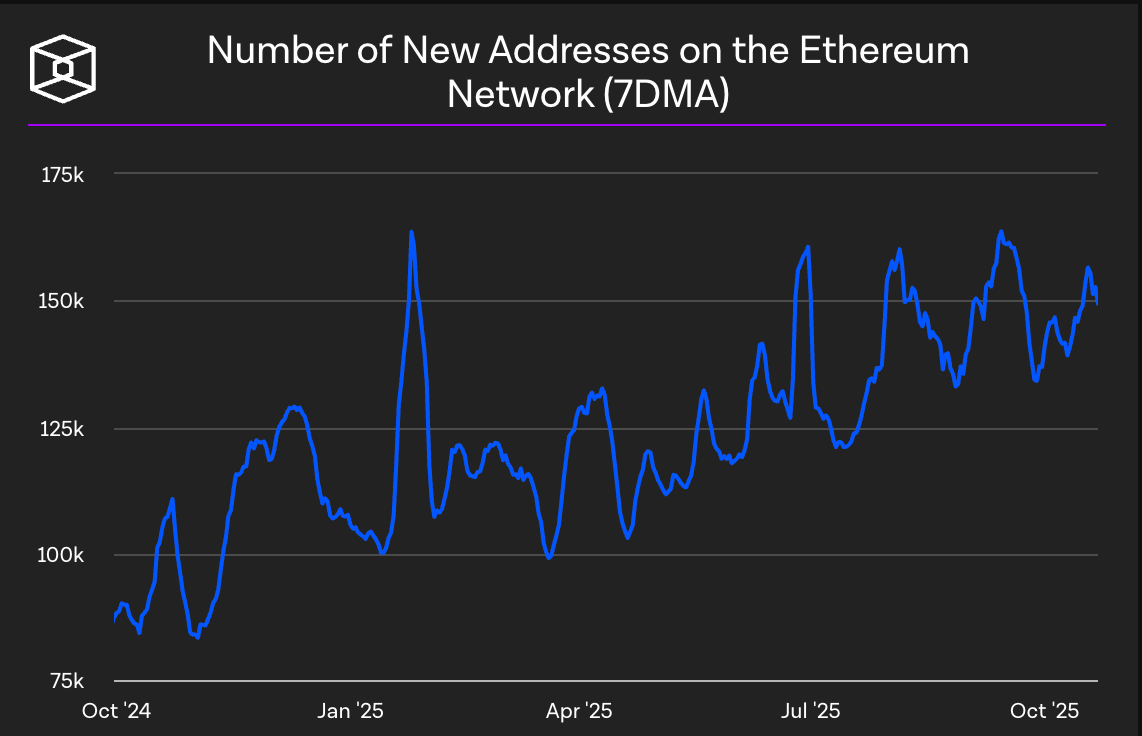

Despite ETH’s price lagging behind BTC and SOL through Q3 and into October, network growth has quietly accelerated. The number of new Ethereum addresses has been trending higher all year, and even with periodic pullbacks, the 7-day moving average remains firmly elevated — consistently holding above 120K new addresses per day and recently brushing up near 150K.

That steady climb suggests organic user growth and developer activity are expanding beneath the surface, even as market narratives rotate elsewhere. This kind of divergence — weak price action but rising on-chain participation — often appears near late-stage consolidation phases, when speculative attention is low but long-term network fundamentals are strengthening.

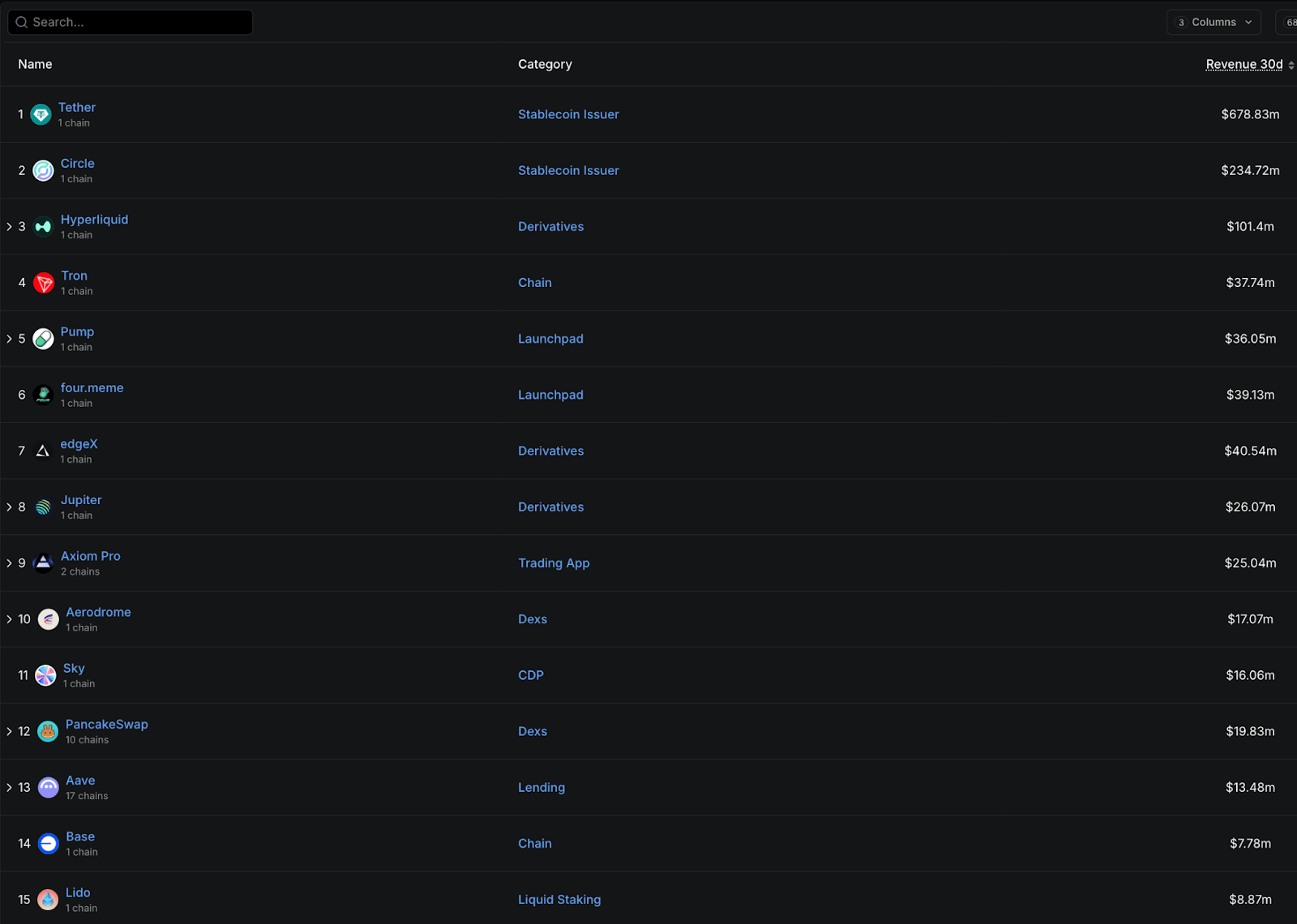

Leaving out the stablecoin giants and Tron, the data makes it clear where the real money has been flowing this month — derivatives and launchpads.

Hyperliquid leads the pack with over $101M in 30-day revenue, followed closely by edgeX ($40.5M) and Jupiter ($26M). Together, these trading protocols highlight the surge in on-chain leverage and perpetual activity as traders rotate capital away from majors into high-beta assets. Derivatives remain the most profitable vertical in DeFi, comfortably outpacing lending, staking, and DEX sectors.

Meanwhile, Pump ($36M) and four.meme ($39M) show that launchpads are still raking in serious fees. Below that tier, Axiom Pro and Aerodrome represent steady performers in trading and DEX activity, while Aave ($13M), Lido ($8.8M), and Base ($7.8M) round out the list — stable but far less explosive.

Overall, the past 30 days confirm that speculative trading products — both perpetuals and launchpads — remain the dominant profit engines of this market cycle thus far.

Majors & Memes

Majors closed the week in better shape as the softer U.S. CPI print reignited some optimism across risk assets. BTC led the recovery, grinding higher through the week as flows stabilized after recent volatility. The move wasn’t explosive but steady — a sign of improving confidence rather than speculation.

ETH followed with moderate gains, maintaining structure and benefiting from renewed inflows into blue-chip DeFi. BNB recovered slightly after last week’s drop, while SOL continued to show leadership among L1s, supported by consistent volume and network traction. XRP stood out as the best-performing large cap, posting a strong rebound that outpaced peers. ADA, DOGE, and TRX were more subdued, trading mixed but holding above recent support levels. Overall, majors reacted constructively to the macro tone, showing the first signs of stabilization after a choppy October stretch.

Beyond the top names, capital rotated selectively into narrative-driven sectors. AI and infrastructure plays were clear winners, with COAI extending its rally as one of the week’s top performers. JUP, ZEC, and PUMP also advanced, while STORY, BCH, and ENA gained steady traction on improved sentiment. Mid-cap strength was broad but measured, pointing to a more balanced market where traders are re-entering but still avoiding overextension.

The laggards were mostly recent high-flyers giving back gains. MNT, CAKE, and HYPE all slipped slightly, joined by smaller pullbacks in BNB and HTX, as profit-taking set in. The broader picture, though, remains constructive — volatility cooled, ETF outflows steadied, and macro relief gave traders room to re-risk modestly. Momentum is rebuilding, but participation is still cautious, suggesting the market is trying to base before any sustained breakout phase.

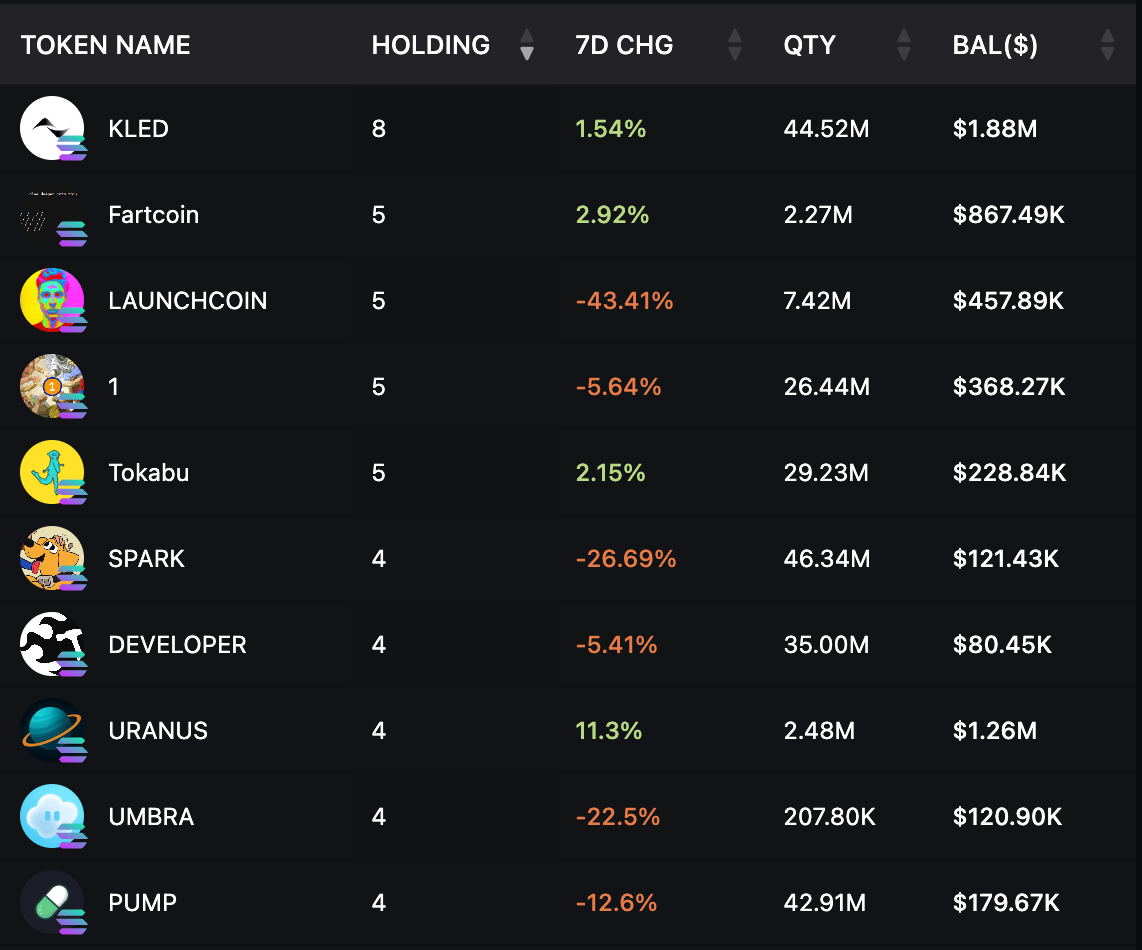

Smart Money Accumulation

Smart money accumulation in the Solana ecosystem this week skewed selective, with adds concentrated at the top and breadth fading. KLED stayed the anchor holding, nudging higher on the week and carrying the largest balance (~$1.88M) across the most wallets on the list, while URANUS printed the clearest build—double-digit 7D growth and a balance above $1.26M—signaling fresh rotation into a smaller set of higher-conviction names. Fartcoin and Tokabu also showed modest net adds, more consistent with topping up than aggressive new entries.

Cuts were broader and heavier in the mid tier. LAUNCHCOIN and SPARK saw sharp weekly reductions, with LAUNCHCOIN posting the steepest drawdown. 1, DEVELOPER, UMBRA, and PUMP were trimmed as well, pointing to a continued narrowing of exposure rather than full exits.

Net-net, capital is concentrating into a few liquid positions while the tail is being reduced—classic risk-aware posture after recent volatility. Wallet counts clustered in the top names, dollar balances reinforced that concentration, and the overall pattern still reads as cautious accumulation rather than a risk-on chase.

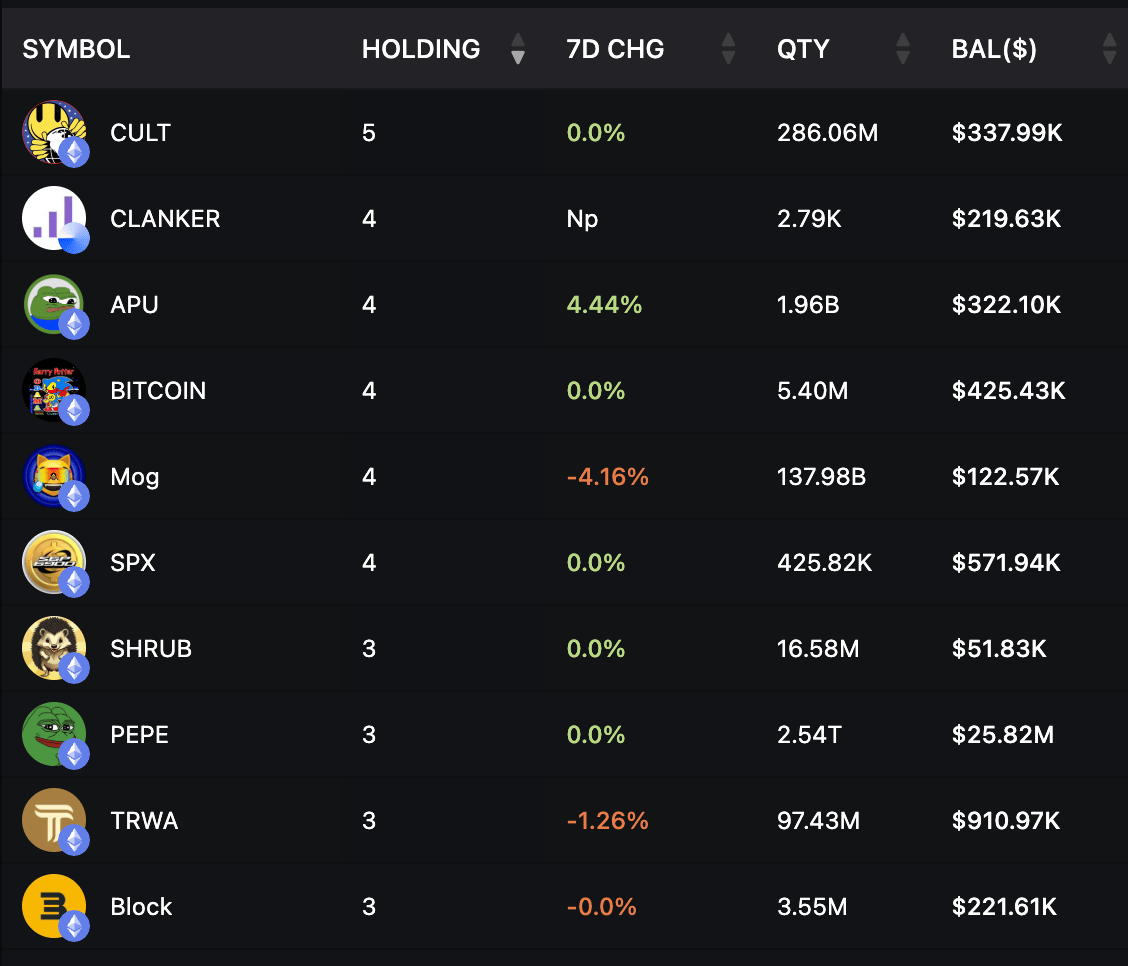

Smart money accumulation across the EVM ecosystem this week was largely steady, showing little net rotation but a few quiet shifts in positioning. Most top-held names like CULT, BITCOIN, and SPX held flat on both wallet count and dollar balance, suggesting a pause in active allocation after recent choppy flows. SPX remains the largest tracked balance at around $570K, with BITCOIN and CULT close behind — a sign that capital is sitting tight rather than rotating out.

The standout move came from APU, which posted a clear rise in wallet allocations and total holdings, showing some renewed speculative accumulation. CLANKER entered the list this week with roughly $220K in balances, indicating a small but fresh inflow of capital. On the other end, MOG and TRWA saw mild trimming, while Block, SHRUB, and PEPE were unchanged.

Overall, the tone is neutral — quiet accumulation at the edges, stable holdings at the core, and a general preference for maintaining existing exposure until stronger directional signals emerge.

That wraps up this post—we hope you found the insights valuable. See you next week, anon! 🚀

Reply